How can with China dumping and Chemicals sector being downturn this company be in peak margins? How?

Posts in category Value Pickr

Websol energy system ltd (08-09-2024)

Websol Annual Report.pdf (5.8 MB)

A very interesting Annual Report was published by Websol. My key takeaways were that the company is looking at a 4x expansion in by FY 27 on its current cell business of 600 MW. Apart from that they might get into commercial wafers and ingots production apart from captive use and this might help them retain good margins. Also, they are entertaining getting into solar rooftop EPC side of the business.

With all these optionalities I see this company as a 25000 cr Mcap business in next 2-3 years if they are able to execute professionally like they have till now.

Disclaimer ~ All disclaimers are useless, we are all responsible for our own decisions. I am currently 92% net wealth invested in this company and I am up almost 90% in one month. This makes me biased but at the same time, I can sell and switch to any company without being liable to inform. My projections of 25000 cr mcap comes from a topline estimation of 2500-3000 cr topline with 10 Mcap to Sales and an assumption that 2-3 years down the line the company will be aspiring to reach 5gw capacity and hence the elevated exit multiples shall be assigned. Also, Premiere Energies with a Quarterly Topline of 1600+cr and almost 50,000 cr Mcap will be a good North Star metric for a company like Websol. There is no reason why Websol cant be 2-3 years down the line where Premiere is right now

Ending my Disclaimer with the theme of the Annual Report

“BOLDNESS IS EVERYTHING”

Onwards and Upwards!

VLS Finance limited (511333) (08-09-2024)

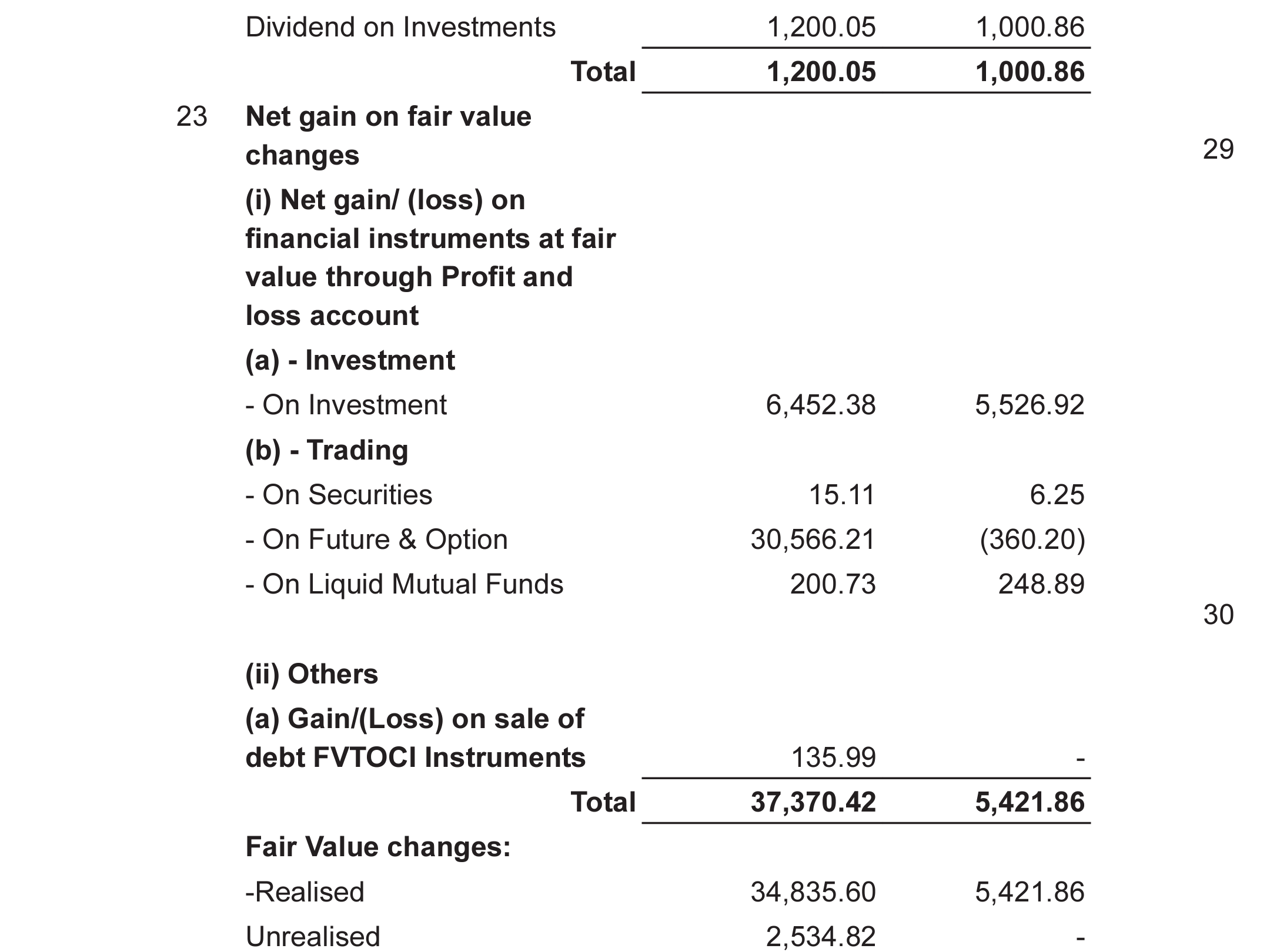

In the Annual report I can see in net gain on fair value change for trading On Future & Option is 30,566.21

So, the company made around 305 crore from f&o?

SWAN ENERGY LIMITED (SEL): The company focussing on sectors with strong tailwinds (08-09-2024)

Just one confusion. Has the 5 MMTPA terminal already been completed? Sources keep say it will be completed. In that case what explains the outperformance of the energy sector? Thanks

EFC – Entrepreneurial Facilitation Centre (08-09-2024)

Following my points on this video –

(1) I could not digest the statement on potato as he was in final year of B Sc. Agriculture and he was not knowing where potato grows underground or aboveground!!. I can believe if he is not graduated in Agriculture science – integrity of the promoter !

(2) One man army can work for small level business but not if he want to grow company to mid/large cap. His approach looks like “Jugad” do it at lowest cost. Most of people are from his association. To grow company, professional talent has values and promoters should give respect to talent in respective area

(3) Promoters mentality / thinking is good to grow company from micro to small cap but such approach can not work for further growth of the company

(4) I shall remain cautious and keep track on equity dilution, related party transactions and quality of growth and quality of clients they get for office occupancy!

Tata Motors – DVR (08-09-2024)

Tata Motors DVR shares will be swapped for ordinary shares on September 1, 2024, and the shares will be credited to accounts on September 18, 2024.

The cash entitlements will be remitted on September 21, 2024

Investment in the ancillaries, or ancillaries of ancillaries-vendors of famous companies (08-09-2024)

I would love to hear thoughts & reasoning on the selling between December to next year April/May. How did you arrive to this specific time period?

Thanks

Skipper Ltd., (Power and Water) a moat in making? (08-09-2024)

Though the revenues are increasing, the story that the management paints and the reality aren’t matching. Management wanted the exports revenue share to go to 50% and reach 75% eventually. But the reality is, the domestic revenue share is 86% and exports is 14%.

Supporting this claim, the management says that they have presence in 100+ countries and that they have been getting inquires from multiple countries across the world, North America, Australia, Middle East, Nepal, etc. This is to create a narrative that they are diversified now and hence the revenues should be more predictable.

Let’s look at their order inflows in the past few quarters starting from Q2’23 till date: 461 → 2863 → 410 → 1215 → 1529 → 402 → 1141 crores

Of these, the biggest order was from BSNL (domestic telecom), second biggest order seems to be from PGCIL. They secured 9 contracts from PGCIL in the last 12-15 months.

From the recent concalls, the management confirms that the revenues from EPC, railways, North America are pretty less and that the railway revenues may decrease this year. However, they seem to have got a good order from Australia, not sure of the size though.

Putting all these into perspective, Skipper is a domestic player, largely dependent on PGCIL and the telecom tailwinds (revival packages to BSNL from Govt).

For Skipper to grow 20%, they should get order inflows of around ~ 1200 crores, every quarter, or pretty huge orders (once or twice every year) from the existing clientele. Unless there are tailwinds in domestic sectors that Skipper operates in, I am not sure how that is possible. If any, due to the economic conditions, the orders from PGCIL may dry up or slow down (as has happened in 2019).

If it helps, FIIs have reduced their stake from 9% in June 2023 to 3.6% in June 2024, promoters have reduced their stake from 71% to 66% in the last couple of quarters.

EFC – Entrepreneurial Facilitation Centre (08-09-2024)

Needed a rejig/shake like that to tread cautiously ![]()

EFC – Entrepreneurial Facilitation Centre (08-09-2024)

Thanks for this bro! Got to learn a lot and still much more to learn… THANKS A LOT ![]()