Hi Aditya,

I shared your post with my peers here at ISB (Indian School of Business). Some wanted to know if you’d be open to considering non CA candidates with a fin background?

Regards

Ravi

Hi Aditya,

I shared your post with my peers here at ISB (Indian School of Business). Some wanted to know if you’d be open to considering non CA candidates with a fin background?

Regards

Ravi

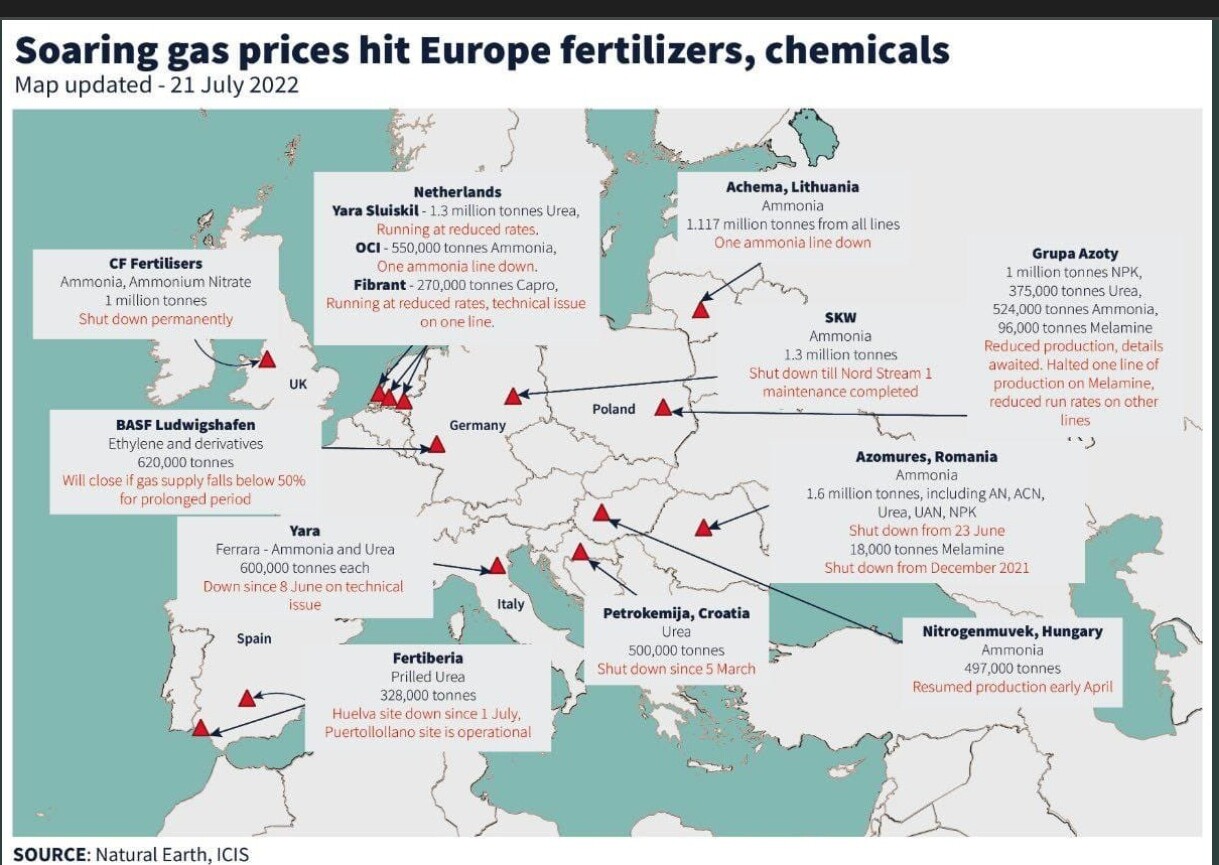

Fantastic opportunity for Indian fertilizer manufacturers.

Just by looking at your Tata Elxsi allocation it makes me nervous. I also hold Tata Elxsi and largest holding but whenever it goes above 10%, I usually get uncomfortable and now it has already hit all time high I am going through the same. Thumbs up to you for holding such a large position in one stock.

On Swiss Military , Do you have any idea how much of revenue can come from Lifestyle Products ?

If I may ask, What is rationale behind increasing allocation in Borosil after demerger. Is it because there might be chances of price going down or something else ?

Portfolio update

| Company name | Allocation |

|---|---|

| Tata Elxsi Ltd. | 31% |

| Central Depository Services (India) Ltd. | 14% |

| RPSG ventures | 13% |

| Borosil Ltd. | 12% |

| Tata Consumer Products Ltd. | 7% |

| Avenue Supermarts Ltd. | 7% |

| Hindware Home Innovation Ltd. | 6% |

| FSN E-Commerce | 4% |

| Swiss Military Consumer Goods* | 4% |

| Studds Accessories Ltd | 2% |

Tata Elxsi

Growth remains strong and demand is intact in spite of inflation. Attrition rate increased but is still lowest amongst the sector. Rupee depreciation decreased the effect of inflation. Valuation remains high at present.

A portion of it has been reallocated to other stocks.

Central Depository Services Ltd.

Growth rate has slightly reduced due to the market downturn.

BSE will have to reduce its holding from 20% to 15% due to directions by SEBI following which it will not remain as the promoter. This company will always operate without promoters under professional management.

They have bought 6% of ONDC.

A portion of it has been reallocated to other stocks.

RPSG Ventures

FSL is having growth reduction and margin contraction due to inflation. This will be mitigated to some extent by revenue growth from IPL rights. Performance of the LSG team was good in this IPL.

Naturali is getting good response in the FMCG division.

Borosil Ltd.

Anti dumping duty on China should help the glassware segment.

The Scientificware division has good growth rate, better margins and higher profitability than the Consumerware division. BOROSIL is the market leader in laboratory glassware in India. I will increase my position when the demerger happens according to cash availability.

Avenue Supermarts Ltd.

Company has nicely recovered from Covid disruption. Growth is back on track and margins have improved. The market size is large enough to accommodate any threat from quick commerce.

The E-commerce division is growing rapidly but is loss making at present.

Tata Consumer Products Ltd.

Recently acquired Tata Coffee has a better margin.

Tata SmartFoodz, NourishCo, Sampann, Tata Soulfull, and Tata Q have high growth.

Tata Starbucks is expanding nicely. Himalayan brand will also sell honey now.

It is an overall nice, defensive, full fledged FMCG company now.

Hindware Home Innovation Ltd

Acquisition of the manufacturing unit of the Building products division from AGI Greenpac Ltd (formerly HSIL) should improve the margin in coming quarters.

Smart appliances and pipes division is growing rapidly.

Margins will remain low due to the higher input and commodity prices.

Swiss Military Consumer Goods Limited

There is no conflict of interest with Swiss Military Lifestyle Products Pvt. Ltd as all business will be integrated with this company. Integration of all Swiss Military product categories like Bags, Luggage and Travel Gear, Travel Accessories, Electronics and other accessories should increase the revenue in coming quarters.

Its book value should turn positive when the rights issue is over.

*Price was halved when rights entitlement was given, so allocation decreased.

Studds Accessories Ltd

Price has fallen in unlisted market. Margins may take a hit this year due to increase in raw material prices. Waiting for annual report to come out.

No quarterly report is given in unlisted shares. Nothing to track at present.

While looking at companies quarterly performance, we have to know that there are certain companies involved in certain sectors where particular quarters are heavy and some are not so heavy. In companies like HBL where an element of defence orders is there and govt projects like railways are there, quarterly results can be often lumpy, so its better to look at them on a yearly basis. There are some sectors like construction, defence, etc where last quarter is often best quarter. Another example is of Kaveri seeds where q1 is the most important quarter.

Even after all precautions, stocks often fall because of unexpected reasons and in these situations, the rough has to be taken with the smooth and it often makes sense to exit at earliest sign of trouble.

A small scuttlebutt.

The mgmt has been beating up their drums regarding rolling out of the app. Installed and tried to use it today.

volume growth will happen because of market share gain. they maintain the ebitda margin. But if steel price softens the topline bottomline will reduce. in q4fy22 concall mgmt told they are sure of 20% volume growth but don’t know about price

Mr. VK Misra, Technical Director, JK Tyres & Industries Ltd. expressed that contrary to the global scenario, we do not have any waste tyre and every kg is consumed in various processes in India. The important aspect is proper use of end-of-life tyres which are environmentally friendly. We need to collectively plan steps to ensure this and find solutions to hurdles to which we are expected considering not an organized process. While it is important generalize disposal of waste tyres, it is even more important to recover raw material from these which would be true circularity. Currently, in India the recovery is very limited and we need to work towards getting support from the government. A lot of work is happening to recover carbon black, a key material for the rubber industry and polymer as well. This is the area which requires large investment with various adequate technology.

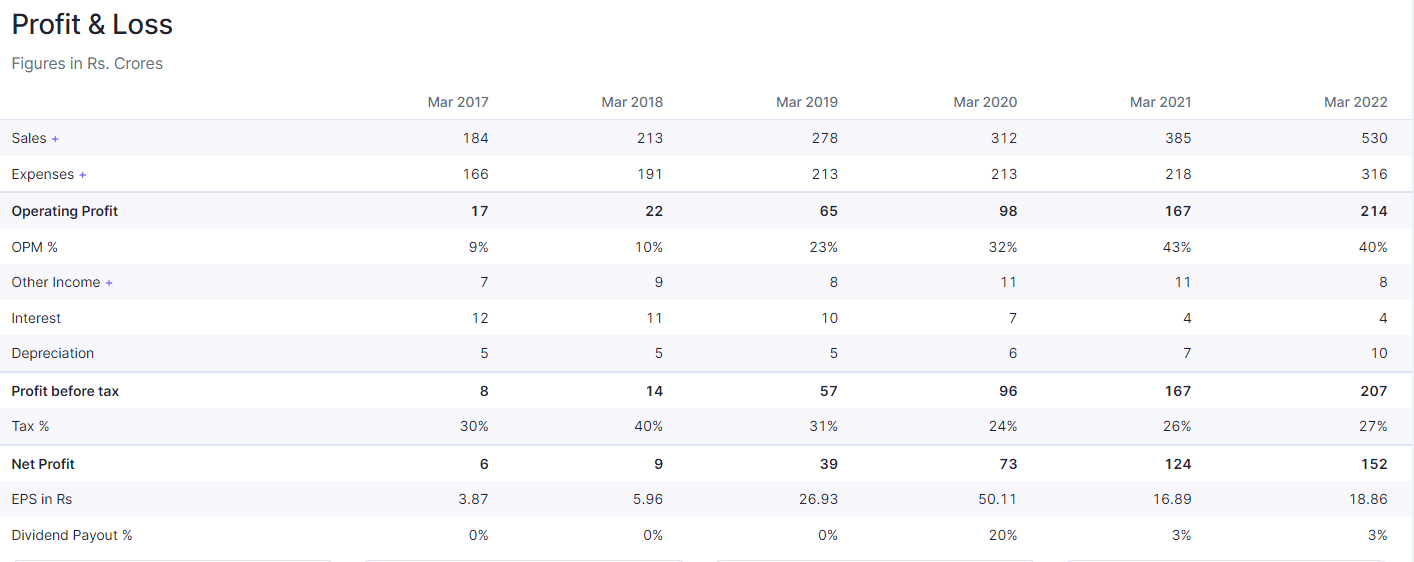

Profit and loss statement

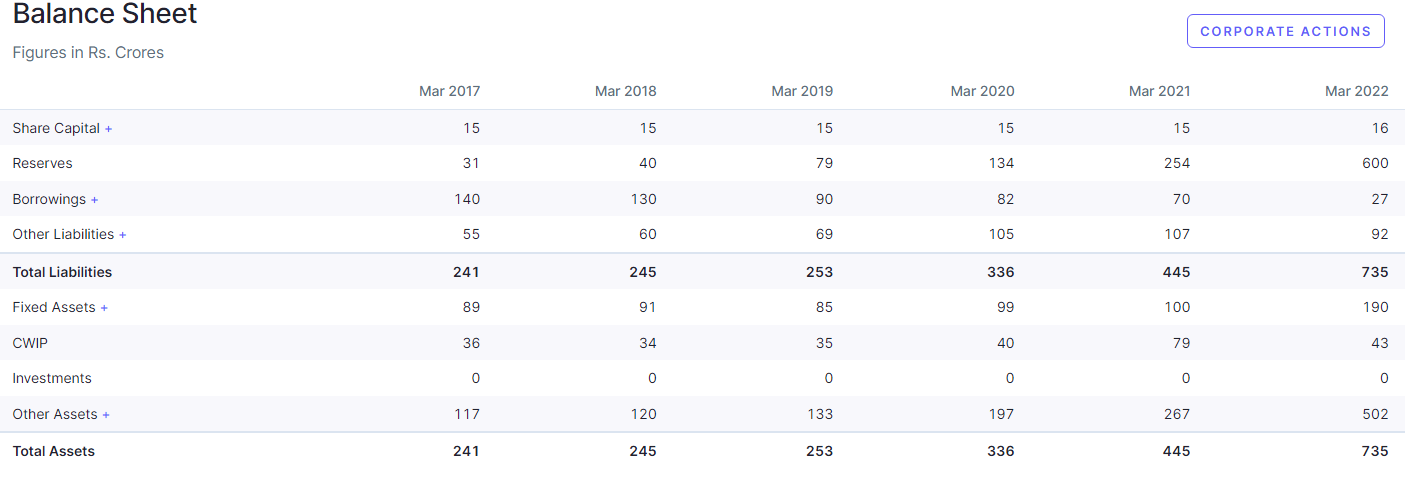

Balance Sheet

Dear investors,

Above profit and loss statement show OPM margin jump from 10% (2018) to 23% (2019 and onwards), if we check balance sheet fixed asset, there is no increment during or one year before (capitalization amount) these periods. so chances of backward integration during this period is less.

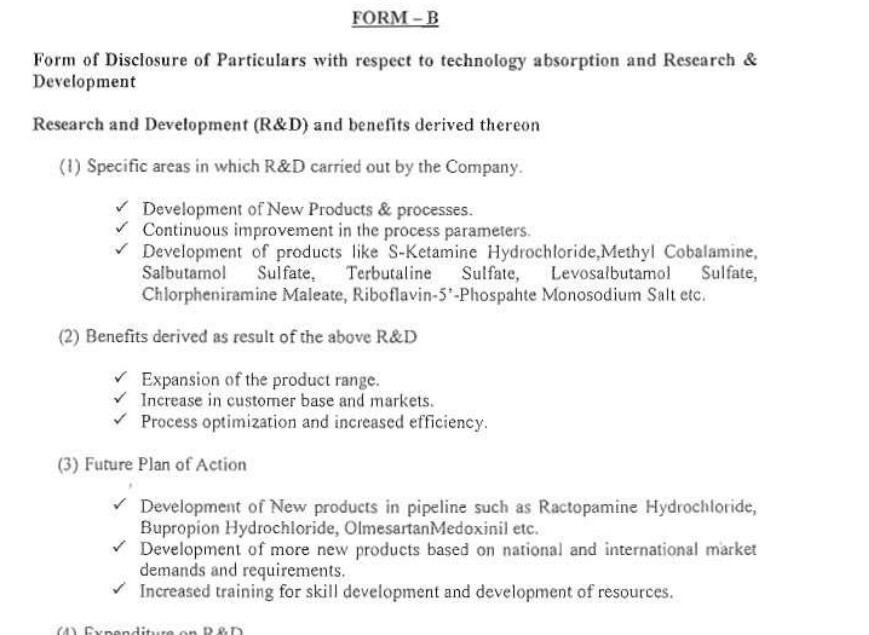

Below is screen image is from annual report of 2018-19, shows same product (as shown in current year) as major export product.

May be this jump in margin is due to price fluctuation (could be temporarily), sustainability of margin is the question

may revert with your views.