I think if at all we need to compare Nykaa with any listed player, Trent would suit the bill better with more inclination towards fashion and better growth…

Posts in category Value Pickr

Krsnaa Diagnostics – what is the diagnosis? (06-08-2022)

Can anyone share concall notes from yesterday?

Thank you.

Gujarat Reclaim Rubber (now GRP Ltd) (06-08-2022)

I am analyzing Tinna Rubber vs GRP to understand the differences, competitive positioning & the reason for a vastly different P&L & balance sheet. Some initial insights I have been able to gather:

-

Tinna Rubber & Infrastructure Ltd. - Valorem CXO Meet - YouTube Please see from 56:10 He tells diff between grp & tinna

Grp is only into non road segment, tinna gets 40% or so from road segment Also, grp only makes rubber reclaim products, does not make micronised rubber powder. Tinna does Not sure what implications this has on Gross Margin & opex but will try to dig deeper. - 1 more key difference which came out in grp concall : grp receives shredded tires so no steel is present in them they don’t process the steel Tinna receives ready made tyres which have steel in it & tinna produces steel abrasives out of the steel wire present in the tyre & sells it as well.

- One more critical difference: 90% of sourcing for grp is biax tyres only 10% is radial tyres. Tinna 100% is radial tyres. According to both concalls, Radial tyres are growing much more rapidly than biax types. Tinna also says in their concalls that radial tyres are higher quality & enable them to make higher quality products.

- Tinna employee costs are around 9-10% compared to 15-17% for GRP. Even tinna used to be around 15-17% mark until fy21, only fy22 onwards, employee cost fell sharply to 9%. We find the reasons in FY22 & Fy21 annual reports: excerpts below:

- On EBITDA margins, GRP freight costs is massive at 50cr, so we have to validate whether export is really high margin for them (ex of the freight costs), Tinna in comparison being largely domestic focussed has negligible freight costs (Tinna gets 5% from exports, GRP gets 40% from exports)

- Material cost: wise both are neck & neck, around 45% material costs in FY22 for both of them.

-

Power costs: Even on power costs Tinna has some details in Concall though not very satisfactory. Let us examine.

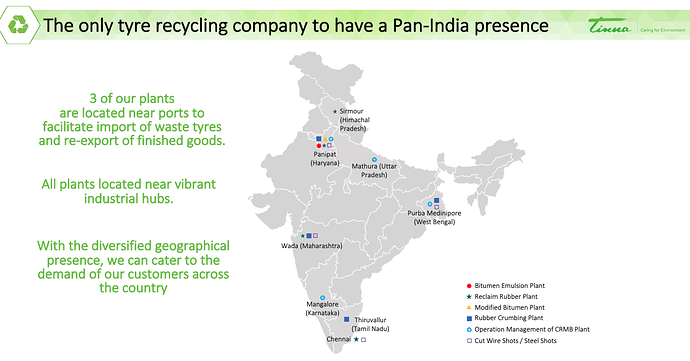

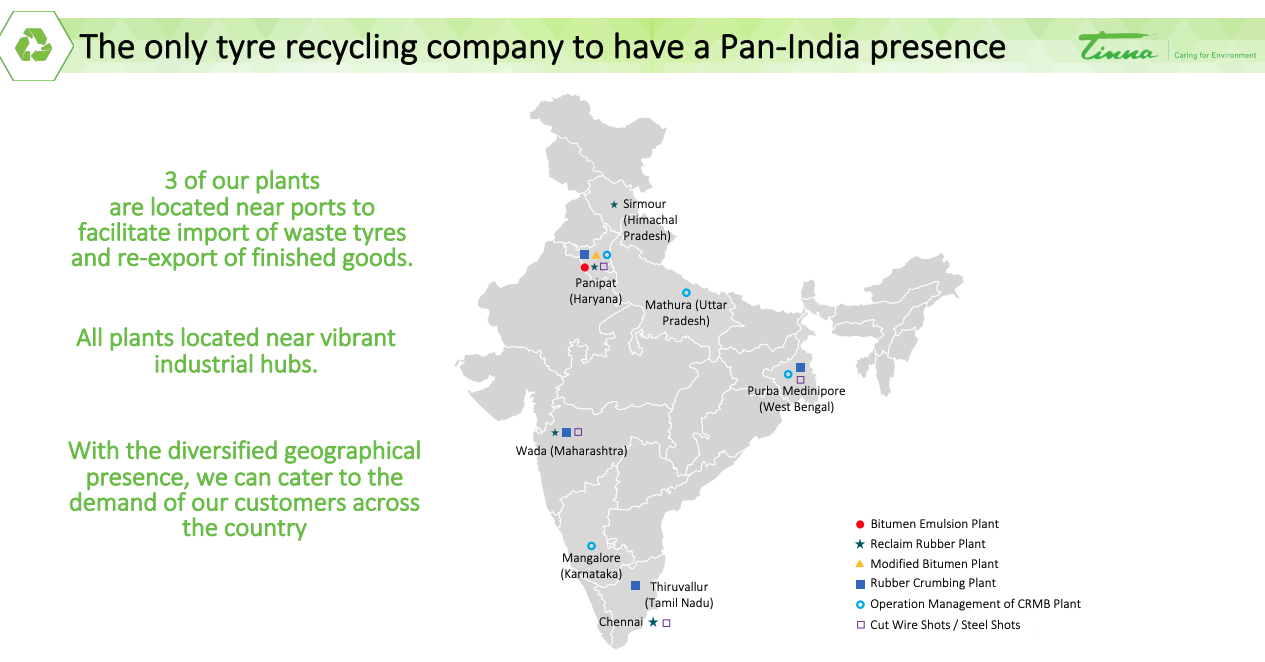

This is a little bit vague & i would love to ask Tinna management what these exact upgrades are which enable higher power efficiencies. One thing to note here is that Tinna has a more diverse manufacturing footprint with plants in Himachal, harayana, Maharashtra, Tamil Nadu & West Bengal

As opposed to GRP which has its manufacturing footprint concentrated in West India (Gujarat, Maharashtra, MP).

The power costs in Gujarat are 6.6 Rs / Unit.

Power costs in Maharashtra are around 8-10 Rupees for commercial users.

Power costs in madhya pradesh are around 7 Rupees per unit. The blending % would depend on the % mix between the manufacturing footprint. A simple average of the 4 plants gives us a blended cost of Rs 7.5 / unit.

As compared to this, for Tinna, the cost of power in Himachal is around 4.2 Rs / unit post subsidies.

Harayana is around Rs 4.3 / unit

Maharashtra has 1 plant which from previous work is around Average of 9 Rs / unit

Tamil nadu is around Rs 6.35 / unit

West bengal is around 4.5 Rs / unit (see during day hours for industries)

Averaging it out for Tinna, we get

(4.2+4.3+9+6.4+4.5)/5 = 5.7 Rs / Unit.

Effectively what this means is that there is a possibility that Tinna might be sourcing its electricity at 30% cheaper rates (we should confirm these assumptions via concalls of both GRP & Tinna). This can partly explain some of the differences in power costs for tinna & GRP. For GRP power costs / revenue is around 12% versus 8% for tinna. Normalizing for the rates of power, The difference is not much. of course these calculations are not exact because Tinna & GRP both could be sourcing some of power in-house as well (solar, wind).

Summary of Findings in tabular format:

| Attribute | GRP | Tinna |

|---|---|---|

| Fy22 Revenue | 388 | 237 |

| Tonnes sold | 60000 | 50000 |

| Realization / Ton | 64666.66667 | 47400 |

| FY22 Material Cost | 47% | 46% |

| FY22 Employee Cost | 15% | 10% |

| FY22 AR on Employee Cost | Statement on ‘continues to invest in upgrading its plant processes towards increased automation’ but cannot see material impact in Employee costs | Implemented automation to save manpower costs. talked in FY21, walked the talk in FY22 AR |

| Fy22 Power & Fuel Cost | 47 | 19 |

| Fy22 Power / Revenue | 0.1211340206 | 0.08016877637 |

| Cost of power unit blended avg in Manufacturing locations | 7.5 Rs / Unit | 5.7 Rs / Unit |

| FY22 Freight & forwarding expenses | 53 | 5.45 |

| Product mix | Only non-road products. Only reclaimed rubber products | Road segment products & non-road segment products & micronized rubber powder. Also sells to building material cement additives |

| Raw material mix | 90% biax tyres & 10% radial tyres | 100% radial tyres |

| Raw material state | Receives shredded tires so no steel is present in them they don’t process the steel | tinna does the shredding & so processes the steel, sells steel abrasives |

this analysis is by no means exhaustive, will continue to add whatever i learn on GRP & Tinna.

Disclaimer: have a position in Tinna, studying both tinna & GRP more deeply.

Gujarat Reclaim Rubber (now GRP Ltd) (06-08-2022)

I am analyzing Tinna Rubber vs GRP to understand the differences, competitive positioning & the reason for a vastly different P&L & balance sheet. Some initial insights I have been able to gather:

-

Tinna Rubber & Infrastructure Ltd. - Valorem CXO Meet - YouTube Please see from 56:10 He tells diff between grp & tinna

Grp is only into non road segment, tinna gets 40% or so from road segment Also, grp only makes rubber reclaim products, does not make micronised rubber powder. Tinna does Not sure what implications this has on Gross Margin & opex but will try to dig deeper. - 1 more key difference which came out in grp concall : grp receives shredded tires so no steel is present in them they don’t process the steel Tinna receives ready made tyres which have steel in it & tinna produces steel abrasives out of the steel wire present in the tyre & sells it as well.

- One more critical difference: 90% of sourcing for grp is biax tyres only 10% is radial tyres. Tinna 100% is radial tyres. According to both concalls, Radial tyres are growing much more rapidly than biax types. Tinna also says in their concalls that radial tyres are higher quality & enable them to make higher quality products.

- Tinna employee costs are around 9-10% compared to 15-17% for GRP. Even tinna used to be around 15-17% mark until fy21, only fy22 onwards, employee cost fell sharply to 9%. We find the reasons in FY22 & Fy21 annual reports: excerpts below:

- On EBITDA margins, GRP freight costs is massive at 50cr, so we have to validate whether export is really high margin for them (ex of the freight costs), Tinna in comparison being largely domestic focussed has negligible freight costs (Tinna gets 5% from exports, GRP gets 40% from exports)

- Material cost: wise both are neck & neck, around 45% material costs in FY22 for both of them.

-

Power costs: Even on power costs Tinna has some details in Concall though not very satisfactory. Let us examine.

This is a little bit vague & i would love to ask Tinna management what these exact upgrades are which enable higher power efficiencies. One thing to note here is that Tinna has a more diverse manufacturing footprint with plants in Himachal, harayana, Maharashtra, Tamil Nadu & West Bengal

As opposed to GRP which has its manufacturing footprint concentrated in West India (Gujarat, Maharashtra, MP).

The power costs in Gujarat are 6.6 Rs / Unit.

Power costs in Maharashtra are around 8-10 Rupees for commercial users.

Power costs in madhya pradesh are around 7 Rupees per unit. The blending % would depend on the % mix between the manufacturing footprint. A simple average of the 4 plants gives us a blended cost of Rs 7.5 / unit.

As compared to this, for Tinna, the cost of power in Himachal is around 4.2 Rs / unit post subsidies.

Harayana is around Rs 4.3 / unit

Maharashtra has 1 plant which from previous work is around Average of 9 Rs / unit

Tamil nadu is around Rs 6.35 / unit

West bengal is around 4.5 Rs / unit (see during day hours for industries)

Averaging it out for Tinna, we get

(4.2+4.3+9+6.4+4.5)/5 = 5.7 Rs / Unit.

Effectively what this means is that there is a possibility that Tinna might be sourcing its electricity at 30% cheaper rates (we should confirm these assumptions via concalls of both GRP & Tinna). This can partly explain some of the differences in power costs for tinna & GRP. For GRP power costs / revenue is around 12% versus 8% for tinna. Normalizing for the rates of power, The difference is not much. of course these calculations are not exact because Tinna & GRP both could be sourcing some of power in-house as well (solar, wind).

Summary of Findings in tabular format:

| Attribute | GRP | Tinna |

|---|---|---|

| Fy22 Revenue | 388 | 237 |

| Tonnes sold | 60000 | 50000 |

| Realization / Ton | 64666.66667 | 47400 |

| FY22 Material Cost | 47% | 46% |

| FY22 Employee Cost | 15% | 10% |

| FY22 AR on Employee Cost | Statement on ‘continues to invest in upgrading its plant processes towards increased automation’ but cannot see material impact in Employee costs | Implemented automation to save manpower costs. talked in FY21, walked the talk in FY22 AR |

| Fy22 Power & Fuel Cost | 47 | 19 |

| Fy22 Power / Revenue | 0.1211340206 | 0.08016877637 |

| Cost of power unit blended avg in Manufacturing locations | 7.5 Rs / Unit | 5.7 Rs / Unit |

| FY22 Freight & forwarding expenses | 53 | 5.45 |

| Product mix | Only non-road products. Only reclaimed rubber products | Road segment products & non-road segment products & micronized rubber powder. Also sells to building material cement additives |

| Raw material mix | 90% biax tyres & 10% radial tyres | 100% radial tyres |

| Raw material state | Receives shredded tires so no steel is present in them they don’t process the steel | tinna does the shredding & so processes the steel, sells steel abrasives |

this analysis is by no means exhaustive, will continue to add whatever i learn on GRP & Tinna.

Disclaimer: have a position in Tinna, studying both tinna & GRP more deeply.

Caplin Point Laboratories (06-08-2022)

The company is executing and planning quite well for it to achieve long term compounding

EXPANSION / NEW MARKETS in established Business

US BUSINESS growth (With larger capacities and product registrations )

BACKWARD AND FORWARD INTEGRATION (API’s KSM manufacturing, Front end presence in the US)

CRO/CMO

All this while generating great cash flows, funding everything with internal accruals, maintaining high and sustainable margins, high returns on capital.

DISCLOSURE: INVESTED

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (06-08-2022)

Ugro capital achieved 4000 cr AUM vs 2900 cr in Jan’22. If they maintains asset quality, Hockey stick growth can be seen going forward.

Caplin Point Laboratories (06-08-2022)

Q1 FY23 RESULTS AND CONCALL NOTES:

-

US Operating revenue grows 61% YoY to Rs. 41 Cr.

-

Geographical breakup of sales: LATAM & Africa – 88 %, US - 12%

-

Caplin Steriles completed the development of 2 complex emulsion injectable products with a target to file them during the current financial year. On track to complete 3 more complex products in the next 3-4 months.

-

Company finalizes plans to start a Warehouse in Chile, with specific focus on Private Market and specialized generics in Tenders . The Company already has 75 products approved in Chile.

-

Company sets up a new marketing team for Vietnam and Cambodia with first order for Cambodia already received.

-

CRO: Company’s CRO wing AMARIS CLINICAL receives approval from ISP Chile, in addition to US FDA EIR. Around 9 products shortlisted for conducting BE studies for Chile, for Caplin. First product approval received (for partner ANDA) through studies completed from AMARIS CLINICAL.

-

API Facility – Company plans for greenfield API facility at Thervoy SIPCOT site acquired in 2020. Project to have 2 dedicated blocks, for Oncology and General Category APIs.

-

First two complex emulsion injectables developed from CSL will be filed within FY23, with Biostudies completed at AMARIS CLINICAL for one of the products.

-

Company has earmarked Mexico and Chile as the next immediate avenues for growth in LatAm . Company has 1 product approved in Mexico, with 6 more approvals expected in the next few quarters. Company currently has 66 product registrations in Chile.

-

Targeting Tier II-III customers in US (Just like the Latin America business model)

-

Launching Own Label products by Year-end in the US (3 products)

-

Caplin Steriles to turn Net breakeven this year.

ValuePickr Pune (06-08-2022)

I am in too Swarang Tanksali 8087958758

Acrysil – Kitchen sinks (06-08-2022)

Acrysil --Few good things happening at domestic front in Q1FY23 which may negate export oriented headwinds

Domestic business has increased by 117% YoY to Rs. 38 crores for Q1 FY23 contributing 22.2% of the revenue. Company has witnessed substantial demand in domestic market and going ahead, expect momentum to continue in domestic market

Company Increased dealer network in domestic market from 1,500 to 1,880 dealers during Q1 FY23 and plans to increase by ~3,000 by end of FY23

Company’s order to IKEA for supply of Quartz kitchen sinks has been doubled.

Production and supplies of additional order started in July 2022