The company has suffered a loss in this quarter and are refusing to show it, negating it with potential future earnings. It is very dishonest accounting to be frank and is disappointing to see. If they can do this then technically they can do the same with other earnings or one time events. 95% of other firms would account the loss in this quarter as a one-off and then when the insurance payout is realised they would show a one time gain.

Posts in category Value Pickr

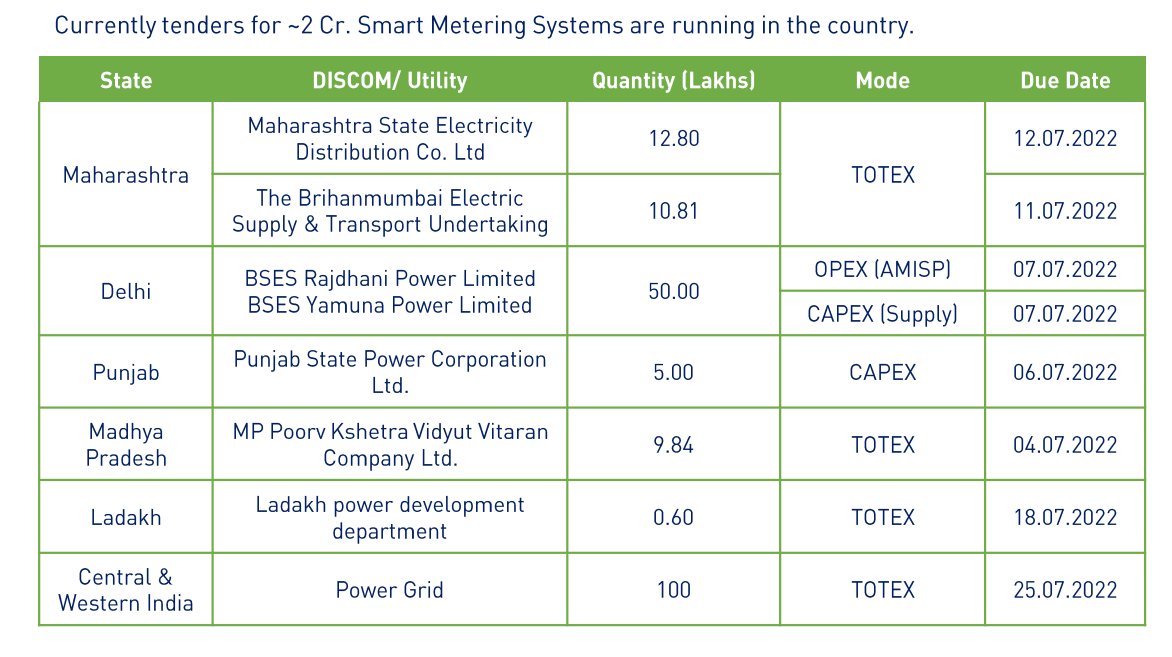

Genus Power – Smart Metering (04-08-2022)

Hi Aniket, Can you share the source of this data? I will try to join the call today and ask some questions if I get a chance.

Redington India : Strong Performance history, re-rating candidate (04-08-2022)

Easing of supply chain constraints. The last two years saw abnormally good WC days because demand was high and supply was constrained. So, the company was able to collect receivables comfortably. The WC is now normalising, 25-30 days is what one should expect. Few quarters will see great FCFs and some will see negative FCFs, it is the nature of the business (mainly because of reporting cut-off date).

Genus Power – Smart Metering (04-08-2022)

Somebody needs to check with the management- which of these tenders they participated in and whether they have got any orders from these.

Metropolis Healthcare Ltd – Another Diagnostic Player (04-08-2022)

But there is difference in MR’s role for medicines and Diagnostics.

In case of medicines, the medicine can be available in any chemist shop, here the important is medicine not the shop.

However, in case of Diagnostic Dr. prescribe the test not the Lab. So the Pan India player, the reliable player will can get patients.

Nazara Technologies (04-08-2022)

Q1FY23 Concall

FY23 revenue guidance growth of 50% organically . eSports, Adtech & Fantasy gaming will drive.

AdTech business has synergies with all other verticals of the Nazara

We have been able to increase Kiddopia price upto 10-13% with new users, without drop in users. Our cost for trial has reduced due to this. Further headroom for price increase available as competitors have increased close to 30%. We have reached pre-apple policy profitability metrics of 1:2 , means spending $1 and make $2 in 24M

Gaming accessory delivered 22cr last FY, This year is growing at 3cr per month

12-13% Ebitda guidance for FY23

Battleground has lesser revenue for Nodwin, which was removed from Googleplay. Nodwin can grow 50% plus .We work with diversified publishers, no impact on battleground getting removed from Googleplay. Nodwin will have an Ebitda of 5-6%

In eSports usually H2 is better than H1 , Q1FY23 was better than Q4FY22 so FY23 looks well poised for growth.

Waiting for regulatory clarity on GST and bans to focus on real money fantasy gaming with growth of user acquisitions

Nazara Technologies (04-08-2022)

Q1FY23 Concall

FY23 revenue guidance growth of 50% organically . eSports, Adtech & Fantasy gaming will drive.

AdTech business has synergies with all other verticals of the Nazara

We have been able to increase Kiddopia price upto 10-13% with new users, without drop in users. Our cost for trial has reduced due to this. Further headroom for price increase available as competitors have increased close to 30%. We have reached pre-apple policy profitability metrics of 1:2 , means spending $1 and make $2 in 24M

Gaming accessory delivered 22cr last FY, This year is growing at 3cr per month

12-13% Ebitda guidance for FY23

Battleground has lesser revenue for Nodwin, which was removed from Googleplay. Nodwin can grow 50% plus .We work with diversified publishers, no impact on battleground getting removed from Googleplay. Nodwin will have an Ebitda of 5-6%

In eSports usually H2 is better than H1 , Q1FY23 was better than Q4FY22 so FY23 looks well poised for growth.

Waiting for regulatory clarity on GST and bans to focus on real money fantasy gaming with growth of user acquisitions

Hindustan Aeronautics (HAL)- India’s Largest Defense Company (04-08-2022)

Hi All,

I have started understanding the business of HAL and have gone through this thread in detail.

Considering the large order book, and possibilities of export, stock price looks close to fair value or marginally overvalued. I am unable to decide P/E range for this PSU as of now.

Also, I have not understood the reason for only 3% Tax in March 2022 (FY22). It would be good to hear from those who have already invested in this stock. Does this happen frequently that, tax fluctuates in this business or was it some one off reason.

Due to this very low 3% tax in FY22, EPS has zoomed from 96.88 to 152.11 in FY22. This is about 57% PAT growth. PBT has not gone up that much. So mainly EPS growth has come from low tax payout. I might have missed the reason for this while reading the thread.

Disc : No investment.

Grindwell Norton-Saint Gobain Merger Arbritrage (04-08-2022)

i think u can use this thread for Grindwell norton alone.

Tips Industries Limited – Ready to RACE ahead! (04-08-2022)

Received long back ( about month ago). Shares are not listed yet.