Hi All,

Recently IRDAI has announced that life insurers can now sell full fledged health insurance plans. I assume this will be big benefit for all life insurance companies.

Hi All,

Recently IRDAI has announced that life insurers can now sell full fledged health insurance plans. I assume this will be big benefit for all life insurance companies.

Hi All,

Recently IRDAI has announced that life insurers can now sell full fledged health insurance plans. Previously most of the health insurance were part of the general insurance division. How this will affect pure play general insurance companies like ICICI Lombard… Now ICICI LOMBARD will have competition from life insurance companies like LIC and their own sister concer life insurance division ( ICICI Pru life)…

Definitely ICICI Pru will launch their own health insurance products

When it comes to Banca partner ICICI BANK. Whom they would refer incase if cross selling health insurance…

Will they have conflict of interest between both life and general insurance arms…

Are there any possibilities of merging both the arm to form one single insurance company?

Hi All,

Recently IRDAI has announced that life insurers can now sell full fledged health insurance plans. Previously most of the health insurance were part of the general insurance division. How this will affect pure play general insurance companies like ICICI Lombard… Now ICICI LOMBARD will have competition from life insurance companies like LIC and their own sister concer life insurance division ( ICICI Pru life)…

Nice post. Have been invested since Jan 2019, first with bank and then switched over in July 2020 to IDFC Ltd. So I’ve gone through the roller coaster, but overall significantly in the positive. Agree totally about asset quality being the key determinant for future….credit costs maintained in the 1% range over several years is what is going to drive meaningful re-rating and BVPS compounding from profits and raising capital at higher multiples.

Having said that, his focused execution of the plan laid out in 2018 is very commendable and gives me confidence to stay invested and watch the story unfold here.

Wow this post has given me a very good understanding how the valuation works for banks, it’s part of past track records, why hdfcbk gets a pb ratio of 3-6.

So I guess market will give it a good PB ratio once it’s convinced about the asset quality of the bank for long term. So inspite it hitting a 15% ROE unless market is convinced of it’s underwriting quality over long term it won’t get premium valuation. But if banks like Bandhan Bank can get a pb ratio of 2 I guess IDFC first bank also deserves a PB ratio of 2 because it’s loans are less risky compared to Bandhan, provided that IDFC hits 15% ROE.

Disclosure: Invested at average price of 36 so has valuation as margin of safety.

Lets see how are the results tomorrow. If they keep a tab on expansion, they might report good profits.

Kedar bhai…

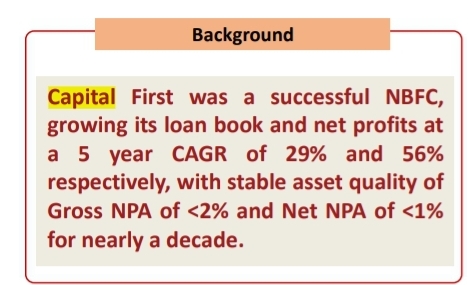

When a conversation comes to credibility, VV refers to his Capital First days. And rightly so. Idfcfirst is nothing but an extention of his career from Capital First.

A chunk of that book is carried under the new banner. That business is a time tested one. Those Customers are well understood.

This also gives us relief to know that VV has been doing this core lending business since FY 10

NPA is one thing he knows how to keep under check. His team has good experience in collection systems etc.

Most importantly, he has passed the litmus test: Covid. If he can survive that, get away without major NPA, then he is good for another decade.

What appears new to his experience is the technology bit, the in-house credit card and loan disbursement tech where they will bypass the need for DSA. Hence, reducing cost. It appears, that couldn’t be a huge threat.

Banking is a balance sheet business for the most part. Lending will always be the core activity and it is not easy to run a lending book in a country like India (~6 Cr odd people filing taxes in a population of 140 Cr) without an adventure every now and then.

Lending is underpenetrated for a reason in India, a good chunk of the population is simply not worth lending to as of now. Given this situation all large and med sized banks end up competing for the same set of credit worthy customers and companies. The lowest risk lending deals are most likely to be won by those with the lowest cost of funds for obvious reasons. The least risky areas of lending like secured assets will be dominated by the larger banks.

More often than not, high NIM is a sign of risk rather than of superior lending capabilities. Capital is a commodity, which is why the rate of lending is the only thing that matters to borrowers. A loan from HDFC Bank is no different from a loan from ICICI Bank, unlike in some other business segments. A handbag from LV and VIP Industries are not the same, even if the utility is the same.

The other aspect of running a bank well is the ability to build scale and to do cross selling well. Each branch is a micro catchment area where the bank has access to customers who can consume financial products in addition to giving deposits and taking loans. Cross selling fee based services like cards, wealth management and transaction banking to companies do not induce additional balance sheet risk. They call for investment into technology, people and processes and regular operating expenditure in the form of salaries, rent and other overheads. To issues even 100 cards, technology, customer service and processing teams need to be in place from day 1. These expenses do not scale with an increase in the customer base. So when VV talks of C/I coming down over time, he obviously is taking of higher scale doing this, not more operational efficiency.

The best way of assessing these aspects is to see the cost to income ratio and the success in cross selling services and products. Ideally new customers (NTB) contribute to liabilities before they contribute to assets. Leading customer acquisition with lending has been a sure shot way to disaster in India for obvious reasons. VV himself was part of this mistake at ICICI Bank, he is unlikely to make the same mistake again.

Most smart and experienced management teams manage to do branch expansion, expense management and cross selling well.

In my book, Q1 results provide good comfort on the expense management and cross selling parts but doesn’t yet do much for the first part - prudent lending. Not to say that the current lending processes are lax but that there are miles to go before the market gets comfortable about the quality of the asset side of the business.

The foray into prime loans and the focus on mortgages is good from a risk management point of view, even if it dilutes the NIM over time. Growth in the newer areas like digital loans, consumer loans, gold loan etc will take time to season and give comfort to investors.

Keenly watching developments here over the next few quarters. There are obvious positives here after the Q1 results but it doesn’t yet address some of the risk investors have about mid sized banks that are under pressure to deliver 20% loan growth while suffering disadvantages on the cost of capital front.

These will only get addressed with scale and time, even if the operating numbers look very good 3-4 Q’s down the line. Even behemoths like ICICI Bank and Axis Bank have grappled with credit issues - due to both the economic cycle and the specific bank’s lending cycle.

The second part (specific bank’s lending cycle) is the more important one to understand for long term investors. Economic cycles are the same for every bank while which segment to focus on/avoid to build assets is a conscious call taken by the management. A good assessment of this is unlikely to come from going through financials or debating about numbers already declared by the bank. It can only emerge from a good understanding of the credit culture and the decision making hierarchy within the bank. It is truly an intangible and is rarely apparent even to internal folks, leave alone investors observing numbers from a distance.

While banking sector has been a wealth creator in India, the bulk of the wealth creation has been done only by a few banks while the rest of them have only burnt investor capital over decades. In mid sized banks and lenders I guess it is important to play the cycle well. I hope this bank turns out to be a successful one over time but not coming to any hasty conclusions yet based on Q1 results and the obvious improvements in operating efficiency & the steady asset quality so far.

Disc: Holding for self and customers

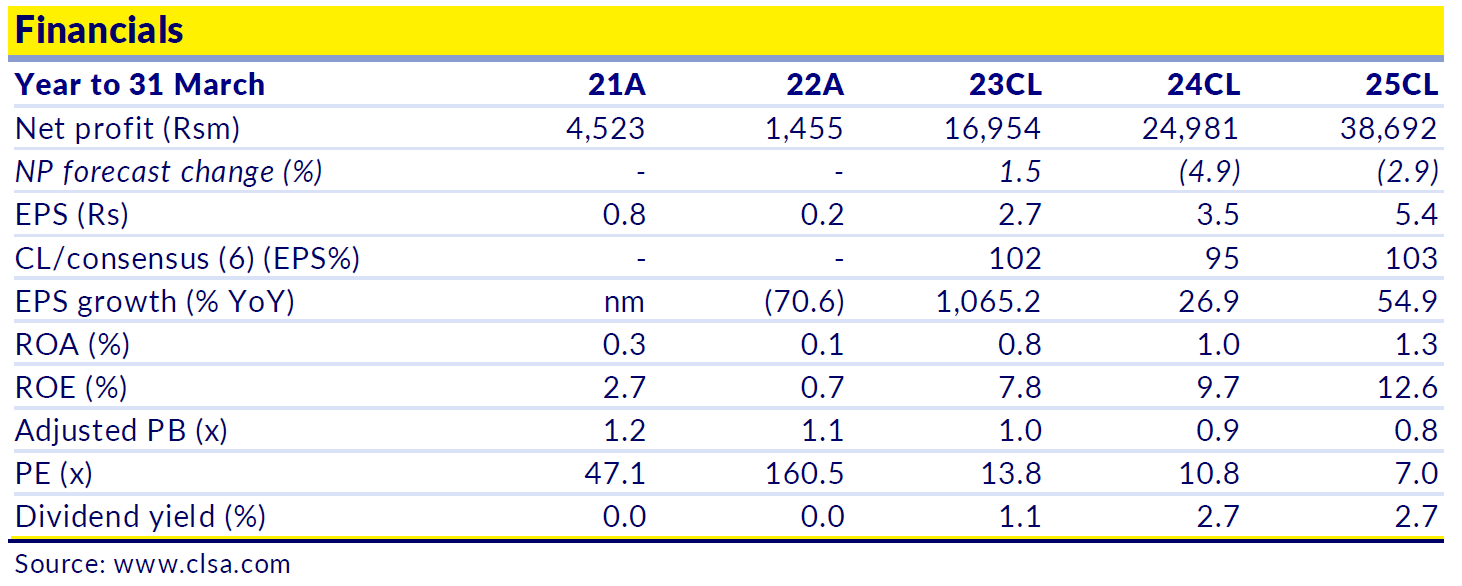

CLSA does not see RoEs hitting 15% even in FY25. Same thing for low estimates it has for RoAs 3 years down the line.

Disc: Invested