Looks like the Flooring division has done extremely poor in Q1 FY23. Sharp decline in OPM to about 1% for this division has dragged the overall bottomline.

Posts in category Value Pickr

Affle India – India Mobile Internet Advertising Leader (29-07-2022)

so no details on how much PhonePe paid Affle eventually?

StageInvesting +Elliot Waves (29-07-2022)

It came in early July…with the FED July meeting completed with no surprises, the next meeting is in September…@StageInvesting Does this mean, a free run in S&P till the Sept meet?

eMudhra – building seamless digital and paperless experiences (29-07-2022)

25% + growth is expected in next 2-3 years. EBITDA margin will remain around 40%.

TARSONS products ltd (29-07-2022)

Tarsons 39th AGM :

We serve multiple industries and a brand in life sciences space.

IPO subscribed 77 times.

FY2022 :

48% EBITDA growth

33% revenue growth

We have been able to surpass industry growth. We are focussed on cost reduction to maintain margins.

We have goodwill with distributors

we will report satisfactory results in months to come.

Manufacturing capacity up due to increased demand. In line with expanding portfolio, 5 acres in panchla, fulfillment centre in Amta.

Achieve long term value to all stakeholders

Q&A :

We are developing 2 new facilities (Panchla 5 acres Q1FY24 commence, Amta (state of art fullfilment centre, getting sterilization in-house). Various new products at these facilities. Will keep us in good growth in next 5-7 years.

Amta : 75% of facility will be fulfillment centre, radiation plant for sterilization to save cost and time.

Develop bio process facilities at Amta in future.

Dividend : Capex using funds, will benefit to co. in long term hence no dividend declared. In coming year, will consider.

Penetration in overseas market :

As of today, 33% exports. We are just a decade old in export market.

Lost manpower due to accident ? Our safety norms are upto the mark, we have not had accidents at any plants.

Company : 3.31 crores in CSR Masks to Tata medical, Narayan hru, Local areas.

R&D allocation : no RD directly. Currently since inception till now, captured in project cost, manufacturing stakeholders joint projects (mould

Last 2 RD : we have 10 people add to 30-35 people.

RD budget < 1% now.

At peak 2-2.5% of revenue.

1700SKUs spread 65 machines, 500 moulds. We cant comment on exact capacity utilisation.

25% of products : we are back ordered. Facilities for this

2nd 25% of products : 75% utilisation.

Last 50% product : 65% utilisation.

Imported RM : 2/3rd material, rest locally.

IT Capex : 70-80 lacs, implemented SAP

Power expense : Today all plants using traditional. We manufacture plastic products we will look at sustainability. New plants will have 25% dependance on salar power.

Next 5 years, 2 facilities massive expansion, focus will be executing and delivering. Capacity is consumed. Post then new capex.

Premco Global — Narrow Fabric (A critical component for inner wear) (29-07-2022)

Was going through the FY22 annual report. Good that they are again looking for expansion. Given the cash flows and surplus perhaps they could be more aggressive.

Perhaps one of the rare small/micro cap company to be paid dividends every quarter.

Disc: Invested in family and client acs. Views may change.

eMudhra – building seamless digital and paperless experiences (29-07-2022)

thanks a lot for posting the results here. However there seems to be unusual interest in the stock of this company 2-3 days post results. Does Mr. Market know anything that we don’t?

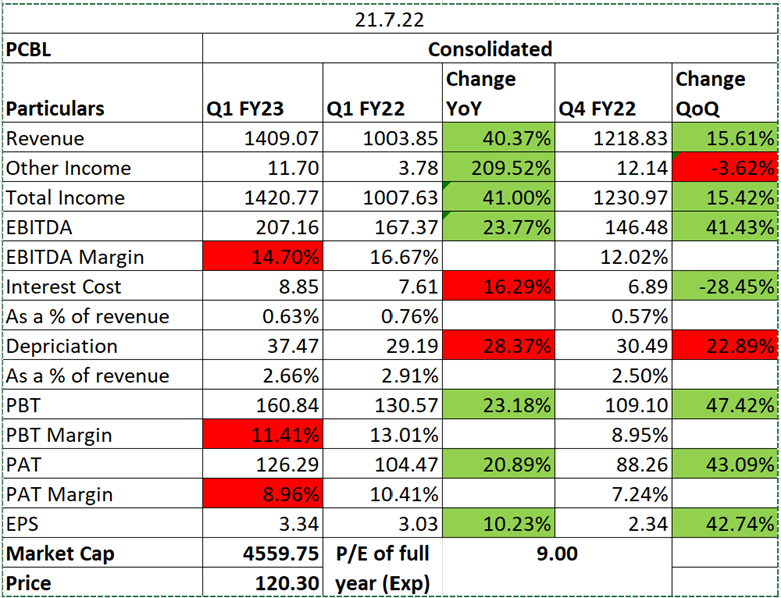

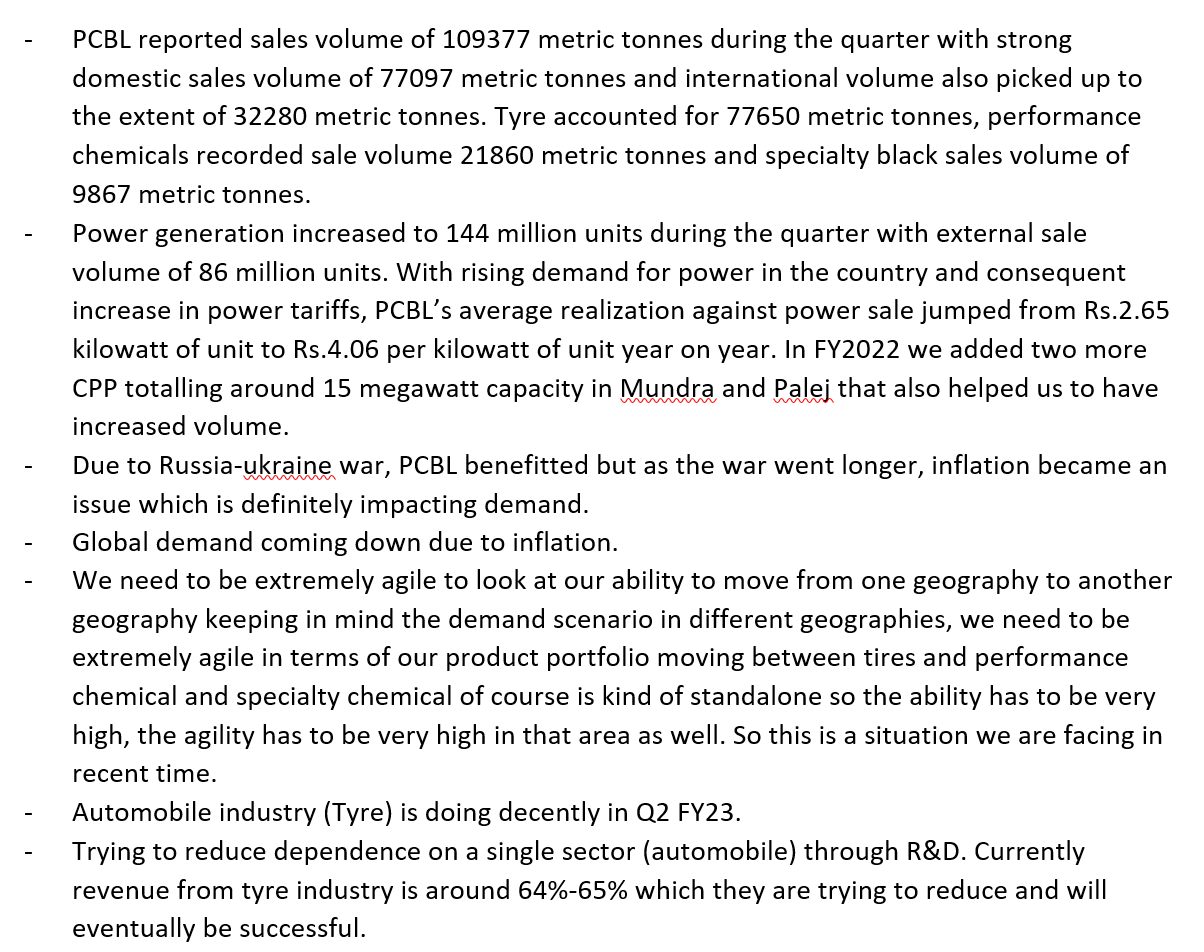

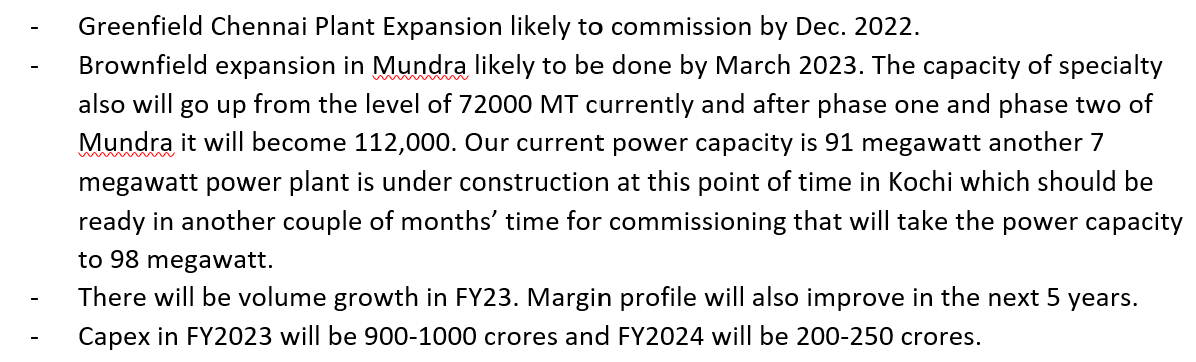

Phillips Carbon Black (29-07-2022)

PCBL Q1 FY23 Result Update!!

Overall, Margin Expansion is expected along the years. They are catious in the short term but very optimistic in the long term. Seems to be an OPPORTUNITY!

Sharda Cropchem – Can it get into indian market in a bigger way? (29-07-2022)

@harsh.beria93 - The key aspect is - Management has tried to clarify - attributing the disastrous Q1 margins to Euro vs Dollar. But the key question is - Is that all true :)…does it make full sense or management is hiding something beyond the currency headwind and freight cost issues.