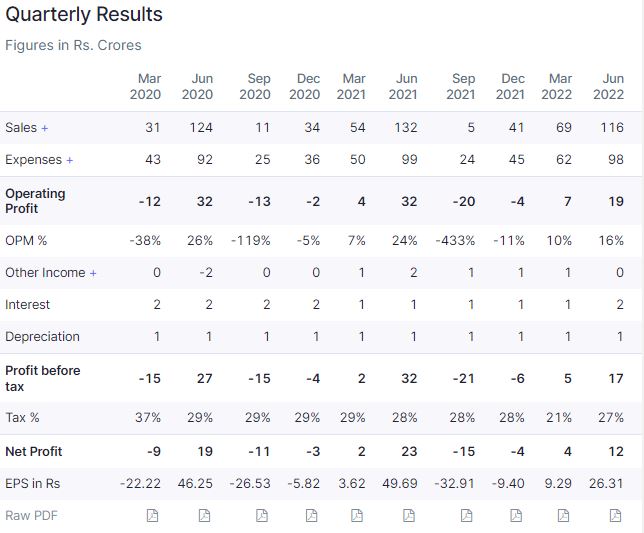

one more bad quarter…sales and margin degrowth… no commetary from management…

one more bad quarter…sales and margin degrowth… no commetary from management…

Insights on second-level thinking and contrarian investment for superior returns. An article by Howard Marks of Oaktree Capital Management.

https://www.oaktreecapital.com/insights/memo/i-beg-to-differ

Excellent article by Anand Sridharan of Nalanda Capital

Notes from AR iro NGL Finechem for FY 21-22 -

Geography wise revenue breakdown -

India - 24 pc

Europe - 28 pc

US - 3 pc

Asia Pacific - 30 pc

RoW - 15 pc

Company has 50 pc plus mkt share in top 3 of its products.

Veterinary APIs grew 26 YoY in FY 21-22

Revenues increased to 318 cr from 258 cr

EBITDA at 69 cr vs 77 cr

PAT at 53 cr vs 55 cr

EBITDA margins at 21 pc vs 30 pc

Aim to launch 3-4 products per year. Currently have 5 molecules in pipeline, each with multi step synthesis. These products are likely to be margin accretive. Their newly launched poultry molecule has shown wide acceptance and is clocking in good sales. Company completed expansion at Macrotech’s plant ( subsidiary ) in the FY 21-22. Also added capacities with brown filed expansion at Tarapur.

Disc : invested, biased.

Notes from AR iro NGL Finechem for FY 21-22 -

A prominent animal healthcare company in India with a global footprint. A leading manufacturer of animal APIs, advanced intermediates and finished dosage forms. Has 3 state of the art manufacturing facilities in Maharashtra - two at Tarapur and one at Navi Mumbai.

Current product portfolio of 21 animal APIs, 02 human APIs, 04 intermediates and 10 formulations. Revenue breakdown -

Veterinary APIs - 82 pc

Human APIs - 7 pc

Intermediates - 9 pc

Formulations - 3 pc

Geography wise revenue breakdown -

India - 24 pc

Europe - 28 pc

US - 3 pc

Asia Pacific - 30 pc

RoW - 15 pc

Company has 50 pc plus mkt share in top 3 of its products.

Veterinary APIs grew 26 YoY in FY 21-22

Revenues increased to 318 cr from 258 cr

EBITDA at 69 cr vs 77 cr

PAT at 53 cr vs 55 cr

EBITDA margins at 21 pc vs 30 pc

Aim to launch 3-4 products per year. Currently have 5 molecules in pipeline, each with multi step synthesis. These products are likely to be margin accretive. Their newly launched poultry molecule has shown wide acceptance and is clocking in good sales. Company completed expansion at Macrotech’s plant ( subsidiary ) in the FY 21-22. Also added capacities with brown filed expansion at Tarapur.

Disc : invested, biased.

I saw some post on twitter that data center work is on

Company started buying shares yesterday as per open market buyback, let us hope it gives a floor and results provide tailwind for stock to go up…

detailed investor presentation

Something on similar lines from South Korea

Any idea why receivable days has jumped in FY22 vs previous years?

In Automobiles SDA usage is in Catalytic Converters .

SDAs are the key building blocks for manufacturing high-precision zeolite which is used in automotive emission control, petrochemicals, continuous flow chemistry,

Dont think its used in gasoline .