You seem to have mastered this skill of finding the companies which are very early in their journey. It’s the time when no one is looking at those companies. But can you please help us understand how do you spot such opportunities. The companies that you mentioned in the example, usually don’t get screened because story hasn’t actually started playing so what is your framework to spot such opportunities?

Posts in category Value Pickr

Suprajit Engineering (26-07-2022)

HDFC Securities initiated coverage

LDC Business is facing issues.

Marksans Pharma- Can it be the next Pharma Biggie? (26-07-2022)

I have mentioned that if share price falls to 40 then I will deploy my additional cash. Its just my planning for future. No body knows how future unfolds. Its my conviction based on concall studies and macroeconomics.

Disclaimer: Part of portfolio for long term.

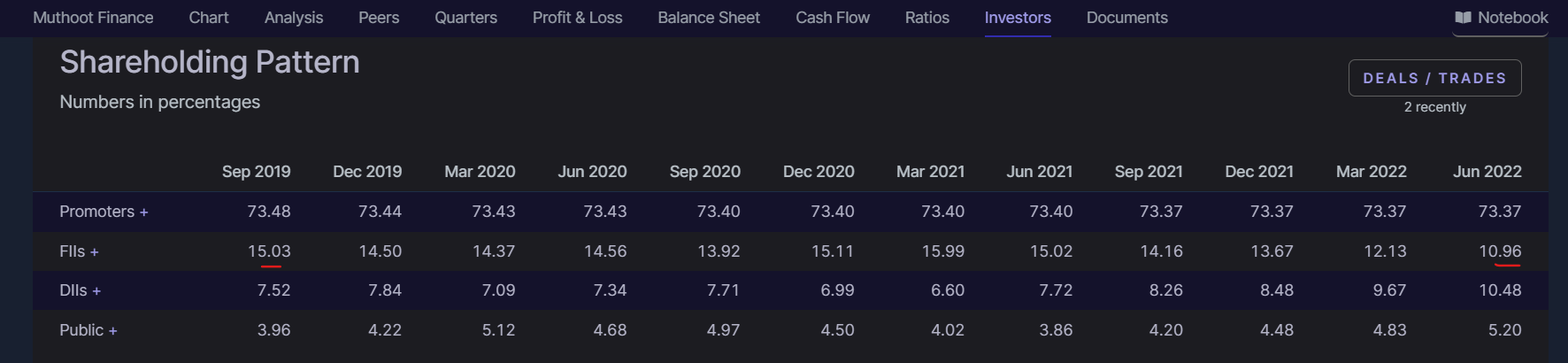

Muthoot Finance (26-07-2022)

FIIs have offloaded 5% of their stake…

Chemcon Speciality Chemicals – Red herring or True Value (26-07-2022)

did anyone attend the agm. If yes will be great if can share the notes

NIIT Ltd (26-07-2022)

I think it will be SNC, under “Talent Pipeline as a Service (TPaaS)”, where they kind of build pool of job ready employees by training them.

Hitesh portfolio (26-07-2022)

Cross-posting my notes from Tatva Chintan Q1 concall in case some folks following this company are keen.

Tatva Chintan – A catalyst for growth (26-07-2022)

Concall: Tatva Chintan Pharma Chem Earnings Call for Q1FY23 - YouTube

Investor PPT: https://www.bseindia.com/xml-data/corpfiling/AttachLive/5605c8a3-6517-4977-b734-c11ac57ad8bd.pdf

My notes on Q1 FY23 concall:

SDA

- Elephant in the room - Drop in SDA demand for Q1 (52% in FY22 vs 7% in Q1FY23) and Q2 was advised in Q4 concall.

- This is a temporary demand problem mainly due to semiconductor shortage and geo-political issues, further increased due to COVID lockdowns in China.

- Despite SDA tanking, achieved 83% of YoY numbers meaning other segments are quite strong. PTC + Salts + PASC showed 60% YoY growth, expect better through to Q4 due to 1 new product in PASC gone into commercial sales now.

- SDA is high margin segment so lower EBITDA margin in Q1 is due to loss of revenues from SDA segment

Guidance for FY23

- Renewed demand seen. Q2 to be marginally better than Q1 with Q3 onwards full scale demand expected.

- Carrying higher inventory now mainly due to expected demand uptick from Q3 onwards.

- So, realistically expect to achieve 90% of FY22 numbers. Mainly due to delay in order for 1 large customer in China which should come in by Dec '22.

- SDA based zeolite catalyst in waste recycling already developed and ready for commercial sales.

PTC

- PTC showed historically highest quarterly revenue of 40Cr, growth of 79% YoY. TCPCL continues to be leader in PTC segment and has increased market share in Q1 (by how much?)

Guidance for FY23

- More PTC can be sold due to lower captive consumption by SDA segment in Q1. Additional capacity of PTC should be online by Q3FY23 so now full potential of PTC can be realised without hampering SDA pipeline when SDA demand returns.

- PTC demand in Q1 higher due to 1 Europe customer whose 80% demand was serviced by TCPCL due to better logistics than other supplier.

Electrolyte Salts

- Showed historically highest quarterly revenue of 6.9Cr, entire FY22 was 5.7Cr.

- Formal approval from new customer on energy storage device application is in and commercial sales have begun. 2 more customers in pipeline for approvals.

Guidance for FY23

- Robust future for this segment in coming years. Previous guidance is 4x-5x over FY22.|

PASC

- PASC 34.5Cr, strong growth of 28% YoY. 1 new product has begun full commercial sales.

- Monoglyme - Pilot stage equipment will be in place in Q2. For another product (Which one??), equipment is in place and trials underway with commercial sales Q2-Q3FY24 onwards.

- New product in metal extraction is approved and commercial sales to begin in Q4FY23 (1 of the 4 ones in R&D in Q4). At full scale, 30-40Cr revenue potential.

Guidance for FY23

- No major callout for PASC. Previous guidance of strong growth of 40-50% expected over FY22.

Flame Retardants

- Pilot trials completed, Full scale plant trial to start now. Current plant of 5000 MT vs global market size of 160,000 MT. No competitor in India, only 3 known MNCs.

Guidance for FY23

- No major callout, revenue potential towards Q4FY23.

General

- Capex for Dahej as per schedule and should be ready by Q3FY23 (Nov '22) despite 3 weeks of construction strike. Increase reactor capacity from 200KL to 400KL with potential to double revenues in coming years.

- Minor capex of 3Cr towards special tanks for storing flame retardants done in Q1FY23.

- Until FY22, 100% tax exemption for Dahej plant. Next 5 years, 50% tax would be applicable. Overall tax rate should be 18-20%.

Guidance for FY23

- No major capex after Dahej expansion until EC clearance for acquired land comes in.

- Sustainable margins - 23-27% EBITDA margins

Estimates for FY23 based on above commentary turn out to be not too bad actually. With non-SDA segments, growing 60%, if they manage to get ~200Cr from SDA (10% degrowth), you are looking at ~20% topline growth and ~30% bottomline since SDA is high margin. Now that Dahej tax holiday has ended, bottomline will come down a bit and needs higher SDA share to alleviate that. With Q2 to be marginally better for SDA, overall numbers might look subdued until Q3 when additional capacity, renewed demand and new product revenues kick in. I see this as temporary pain for 2 quarters which will hopefully bring TCPCL down from stratospheric into reasonable valuation range.

Disc: Not invested. In my watchlist to invest when valuations are reasonable.

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (26-07-2022)

- CC Revenue Growth of 23% Y-o-Y, 6.0% Q-o-Q. $ Revenue Growth of 16.4% Y-o-Y and 3.2% Q-o-Q ( CC Revenue Growth : 18% to 21% )

- Q1FY23 EBITDA at 19.4% against 18.6% last qtr. Y-o-Y EBITDA growth of 35.7%, 9.7% Q-o-Q ( EBITDA Margin : 18% to 19%)

- Net Profit at ₹ 854 million. Net Profit growth of 41%+ Y-o-Y, 8.3% Q-o-Q

- New wins continue to be stronge.r TCV of $ 155 million won during the quarter

- Sequential CC growth of 6% led by Electric Powertrain and architecture and middleware domains. Growth steered by passenger car vertical. Higher cross currency impact due to Euro, GBP and Yen depreciation against the INR.

- EBITDA expansion of 80 bps despite supply side constraints, fresher additions and cross-currency headwinds. Operating efficiency, net realization improvement and revenue growth leading to consistent improvement in margins

- Healthy growth in net profit aided by improvement in operating margins and higher other income. ETR for the quarter higher as compared to last quarter, as a result of one-time benefit last quarter.

- High cash conversion continued post acquisition payout, with DSO at 46 days. Net Cash at quarter end ₹ 10.6 billion. 14th consecutive quarter of increase in net cash and healthy cash conversion

- Net Cash Available (INR Million) 10,627

New Engagements ( TCV of new engagements won during the Quarter : $ 155 million)

- A leading European Car Manufacturer selected KPIT for a multiyear engagement in the electric powertrain domain

- A leading Asian Car Manufacturer awarded KPIT multiple programs in the connected and middleware domains

- A leading American Commercial Vehicle Manufacturer selected KPIT for a A leading European Car Manufacturer selected KPIT for a strategic program in the middleware domain multiyear engagement in the Vehicle Engineering and Design domain

- A leading American Tier I awarded KPIT multiple programs in the powertrain domain

KPIT expands its team and global infra-structure footprint

- KPIT expands its team and global infra-structure footprint

- KPIT unveiled its brand-new office in Novi, Michigan, USA

- KPIT expands its local tech center in China - KPIT has taken the initiative to add 20 AUTOSAR engineers in Phase 1 to build a Local Tech Center in China. This workforce will consist of 10 senior engineers and ten fresh graduates / Interns. The team has already onboarded seven senior

engineers and five interns. - KPIT to create opportunities in cutting edge automotive software in Kochi

The vehicle manufacturers are aiming to earn revenues over the life of the vehicle for sustainable growth. This change will be enabled by CASE and centralized architecture programs, essentially Software Driven Vehicles. KPIT is uniquely positioned as a software integrator, helping global OEMs accelerate this journey. We have started the year on a positive note with an all-round performance, with growth in-line with our plan and healthy margin expansion, despite cross-currency headwinds. We remain optimistic on the overall growth environment

StageInvesting +Elliot Waves (26-07-2022)

This message is for those who think that technical -analysis is for lesser souls.

Ujjivan Finance chart was telling in advance that something is happening and was giving signals for upmove.

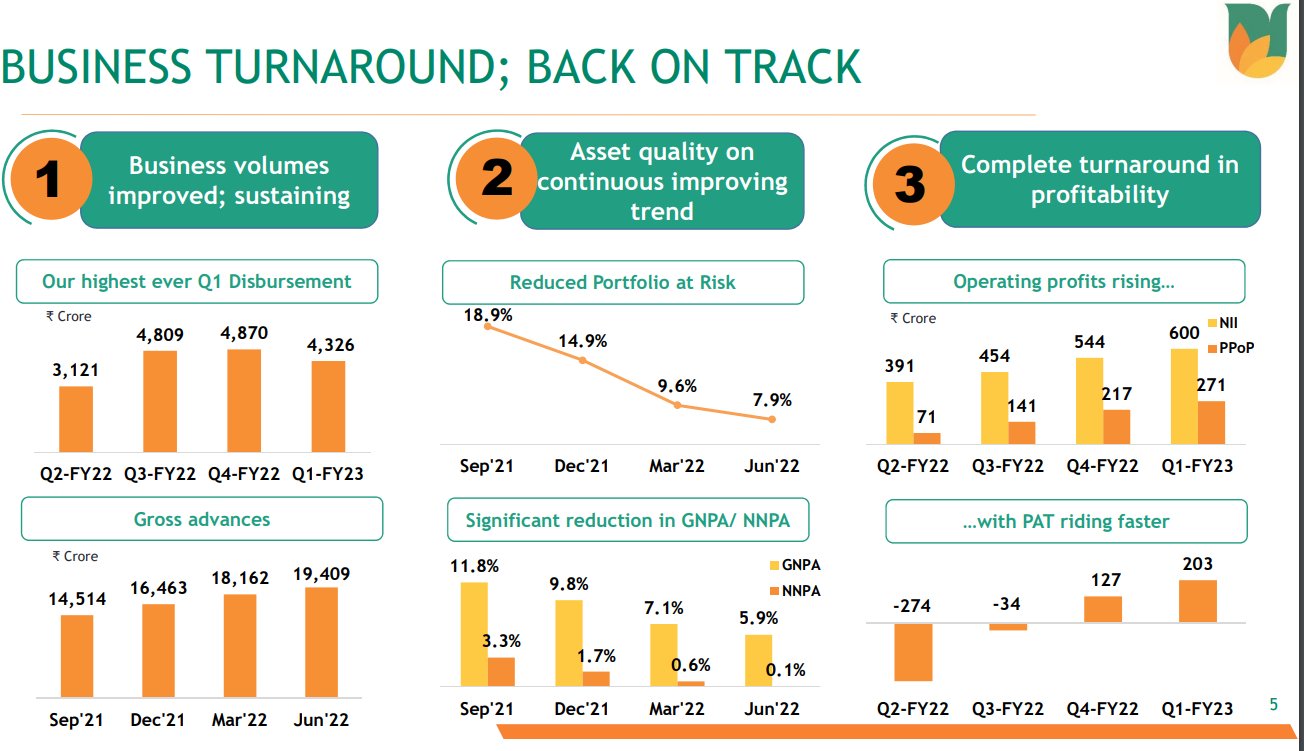

Look at the results declared today.

PPOP at 271cr vs 161cr,

Q4 at 217cr PBT 271cr vs -312cr

Q4 at 173cr GNPA n NNPA sharply lower QoQ n YoY

In short - any work that is done passionately (and if one tries to go into depth ) has value.