Was going through their earnings call. Thought I would summarise it here, which touches on some of the topics including marketing.

Concerns:

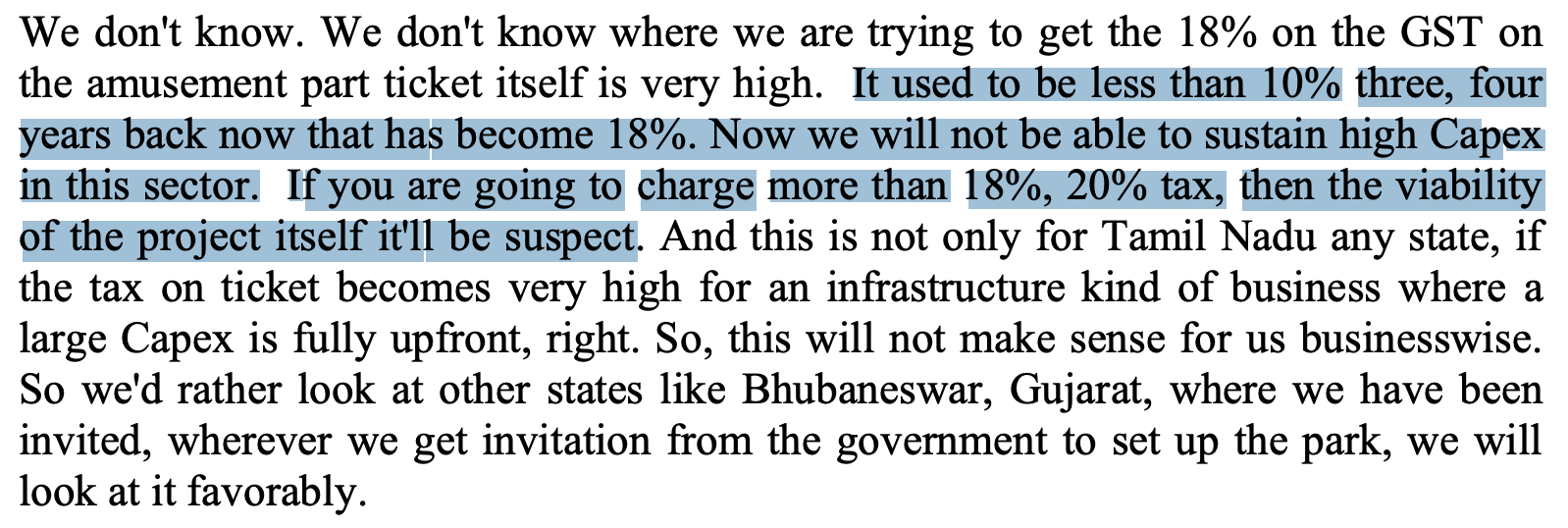

Implementation of GST seems to have material impact, especially in Chennai. This would result in high ticket price that would test customer’s willingness to pay.

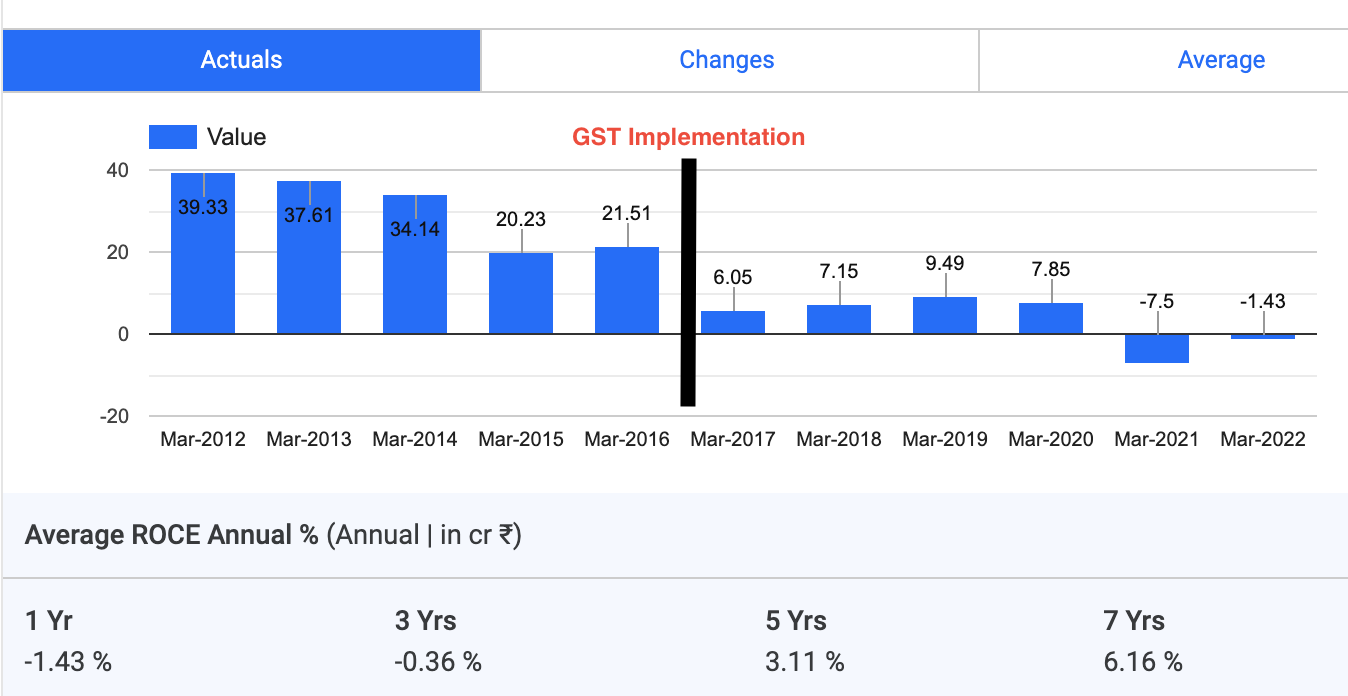

I dont know if GST is the prime reason to have resulted in low ROCE.

On the willingness to pay, when they expand the capacity, the price should come down as they need to attract a lower income people. This is a significant constraint on scaling out vertically. If I am right, the current strategy is to scale to multiple locations and target the higher income group that pays more for tickets. Rest is dependent on economy growth.

Tailwinds

It is interesting to note that the company is entering into digital advertising only now! But, at least they are in right path and not beating around the bush on that.

If things augur well, then there can be some good volume realisation through targeted marketing and improving customer relations.

However, there is a limit to success here. Each park can only grow to a certain peak volume. The key is to improve non-peak volumes and improve ARPUs.

But each park can be expanded to handle 3 million, provided the footfall picks up.

There is a good scope for expansion across regions. If ROCE is stabilised, this is a very good long term play.

What I like the most is the capital preservation, provided if management is good and ethical (which they are IMHO).

Views

Overall, I think the next 2-3 years are going to be a good year for them as long as there are no macro economic issues. The management is good and is quite conservative in their strategy, which is important for an capital intensive company.

Disclosure: Have a tracking position. Might scale up over next qtr