There is already a similar Topic - Checklist I go through before I buy any stock - can you just post this there and avoid duplication?

Posts in category Value Pickr

My Check List for Buying a Company (25-07-2022)

- Must not be a loss making company.

- Must not be a PSU.

- Must be able to remain profitable for next 15-20 years to come.

- Must have zero or very low debt.

- Must not be a capital intensive business.

- Its Product and services must have competitive advantages i.e. 10x better than its competitors.

- It must be very difficult to copy its business by any other company.

- Value migration must not be happening or to going be happened in its business in next 10-15 years.

- Technological or habitual disruption factor should not be there.

- Customer loyalty must be there in the products/services offered by the firm (by force or choice )

- Entry Barrier must be there in the business so that other companies can’t take over its business or take its future business opportunities.

- Pricing power must be there with the company for its products or services i.e. the company must have dominance over its customer,distributor,retailer

- There must be sufficient head room to grow its business.

- The company must have the ability to throw cash to the share holders (may be in a longer period of time)

- Must be professionally run company.If it is 1st or 2nd generation company,then 1 or 2 family members of the promoter in the board is okay.

- All the key positions in the company should not be held by family members.

- The company should be such that ,any idiot can run it.

- Management should be good at capital allocation.

- Stock must be available at good valuation.

- If FIIs/DIIs have less holding,then it is better.

Its a learning process …and will be refined over time.https://themangoinvestor.blogspot.com/2022/07/my-check-list-for-buying-company.html

IDFC First Bank Limited (25-07-2022)

It’s the smart thing to do.

Most saving account deposits are in sub 10L category. So, it’s easy money for the bank; reduced cost of capital, increase NIM.

leading banks give even lower, 3% cuz depositors aren’t keeping the money there for the interest.

The banks CASA won’t see attrition at 4%

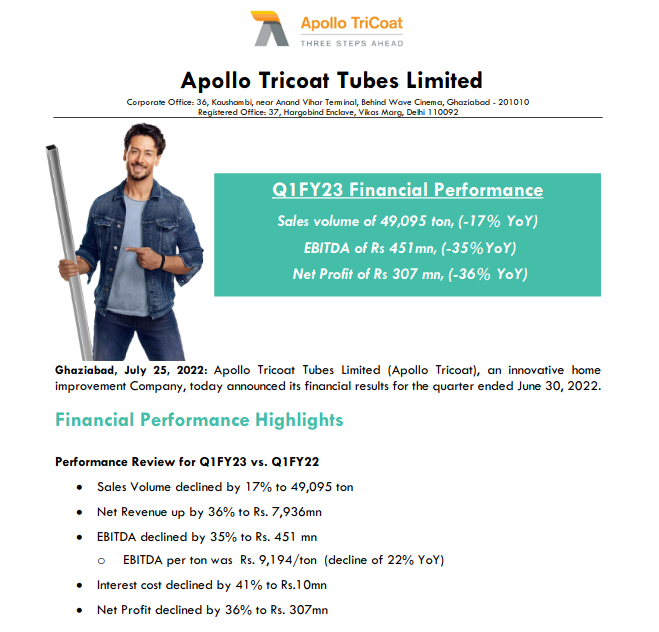

Apollo Tricoat Ltd(ATL) (25-07-2022)

Bad show by Tricoat ![]()

StageInvesting +Elliot Waves (25-07-2022)

POLYPLEX

Thanks for explaining in details. Can you please provide your view on POLYPLEX?

Is it good for 6 months to 1 year hold?

Thanks

Disclaimer : Have invested at lower levels

Vimta Labs Ltd (VLL) (25-07-2022)

Vimta Labs results out today. Very good growth y-on-y and marginal growth q-on-q. results attached.

vimta q1 fy 23.PDF (5.9 MB)

Investing Basics – Feel free to ask the most basic questions (25-07-2022)

Long term loss cannot be set off against short term gain. However, long term gain can be set off against short term loss.

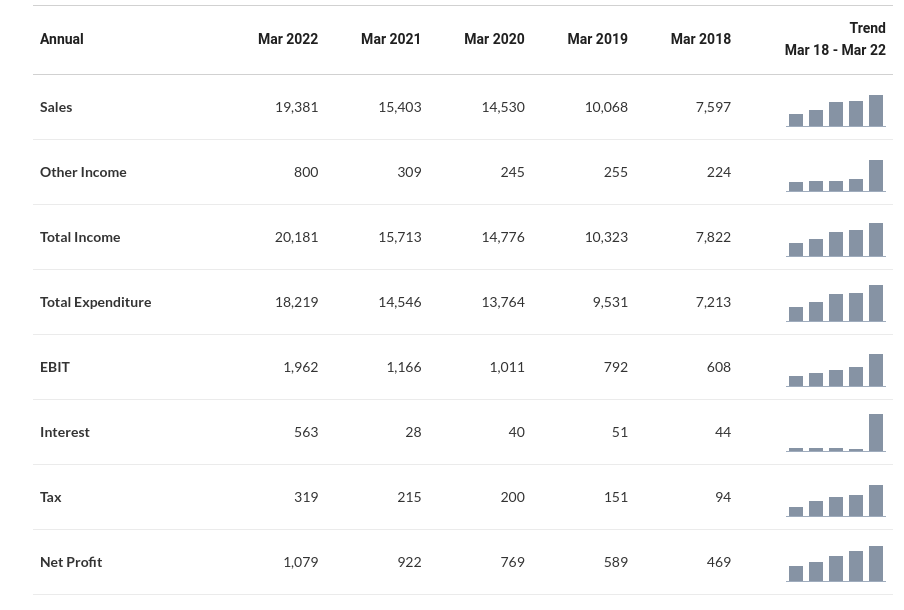

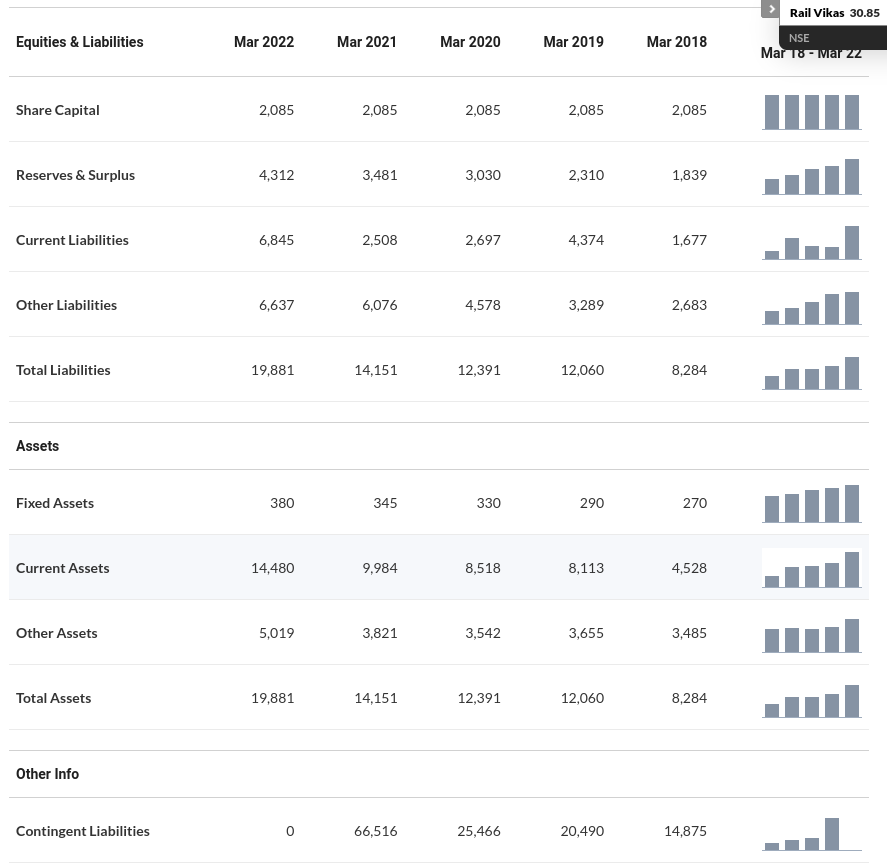

Rail Vikas Nigam – profitable PSU (25-07-2022)

Couldn’t find a thread about it so starting one here.

About Company

Rail Vikas Nigam Limited (RVNL), a CPSE under Ministry of Railways, was created with the twin objectives of raising extra-budgetary resources and implementation of projects relating to creation & augmentation of capacity of rail infrastructure on fast track basis. The Company, incorporated on 24.01.2003, became fully functional with the appointment of all Directors of Board by March 2005. The Company has been granted Mini-Ratna status on 19.09.2013.

RVNL is implementing projects by awarding composite contracts on turnkey basis as per the international practices and standards. As on 31.03.2017, RVNL has completed 213.82 km of New Lines, 1590 km of Gauge Conversion, 2353.32 km of Doubling and 2837.07 km of Railway Electrification i.e. 6994.21 km of project length. In addition, five Workshop Projects and one cable stayed bridge have also been completed. These projects are being executed through 36 PIUs spread across the country.

Besides Doubling and Gauge Conversion, RVNL has also diversified to:

- Railway Electrification

- Railway Workshops

- Metro Railways

- Technically challenging new Hill Railway lines, etc.

The Company generally works on a turnkey basis and undertake the full cycle of project development from conceptualization to commissioning including stages of design, preparation of estimates, calling and award of contracts, project and contract management, etc.

The projects undertaken by the company are spread all over the country and for efficient implementation of projects, 37 project implementation units (PIUs) have been established at different locations to execute projects in their geographical hinterland. They are located at Delhi, Mumbai, Kolkata (4 units), Chennai, Secunderabad (2 units), Bhubaneshwar (3 units), Bhopal (3 units), Jhansi, Kota, Jodhpur, Waltair (2 units), Bengaluru, Pune, Raipur (3 units), Lucknow (2 units), Rishikesh, Ahmedabad (2 units), Kanpur, Varanasi (2 units), Chandigarh, Mughalsarai, Ambala and Guwahati.

The company’s major client is the Indian Railways. Its other clients include various central and state government ministries, departments, and public sector undertakings. Rail Vikas Nigam Limited came out with an Initial Public Offering (IPO) of 253,457,280 equity shares of Face Value of Rs 10 each of the company through an offer for sale by the President of India, acting through the Ministry of Raliways, Govt. of India (the selling shareholder) for a cash price of Rs 19 per equity share aggregating to Rs 477.11 Crores. The face value of equity shares is Rs 10 each.

sources: https://in.linkedin.com/company/rvnl and Markets

Financials

Profit and loss

Balance Sheet

RVNL has a good order book. It has guided for order inflow of ₹15000 cr in FY23E. It has bid for orders of ₹21000 cr. Of the of opened tenders of ₹6000 cr, it has won orders of ₹2000 cr.

It is also trying to diversify from railways. Rail Vikas Nigam announced that its consortium with P Singla Constructions has been awarded the Letter of Award (LoA) by National Highways Authority of India (NHAI) on 11 July 2022 for Construction of 4 laning of NH-S from Kaithlighat to Shakral Village in Himachal Pradesh. The estimated cost of project is Rs 1844.77 crore.

Key risk is that it is almost entirely dependent on government.

Disclaimer: Invested since ipo.

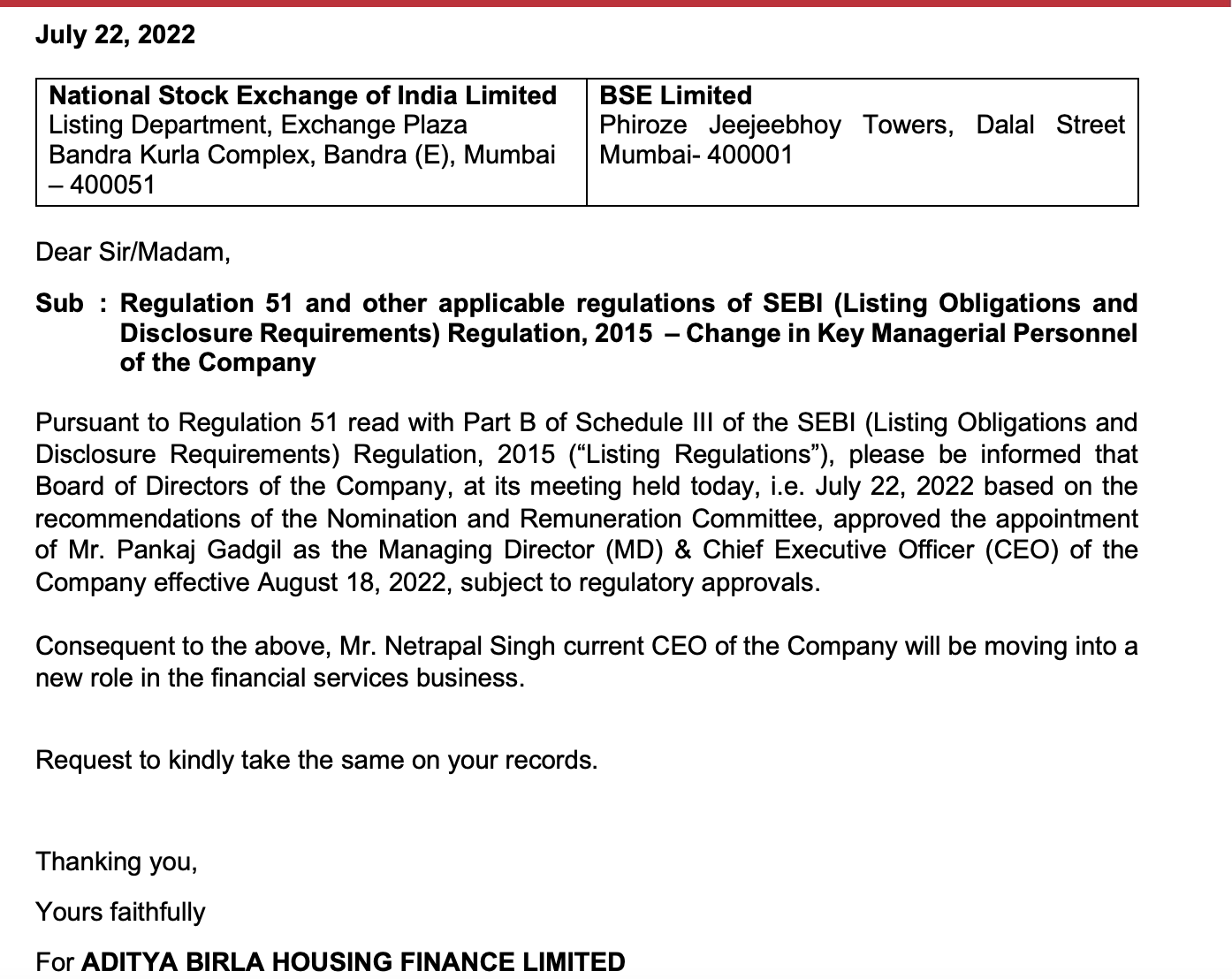

Aditya Birla Capital – A complete Financial Inclusion (25-07-2022)

As speculated here, more top level changes happening at AB Cap. Important disclosure from subsidiary - now the Housing Finance vertical has a new CEO, 19 year ICICI veteran Pankaj Gadgil.

He is also ICICI Bank’s nominee on the board of NPCI. Profile here -

https://www.npci.org.in/who-we-are/board-of-directors/mr-pankaj-gadgil

Hitesh portfolio (25-07-2022)

To be fair, management has guided back in Q4 itself that Q1 and Q2 is going to be subdued for SDA segment which was approx 40% of their FY22 topline. They did advise this is a temporary pain due to semiconductor shortage as auto emission control is a major application for SDAs. And this segment should be back firing in Q3 and Q4 so much that it should cover for the subdued Q1 and Q2. So, I think we should hear the management out. If the commentary changes, this can be taken as heading in the wrong direction.

But if by Q3 growth is expected to be back, the long term business would still be intact. In fact, backlash in the short term due to these and potentially similar Q2 numbers may provide entry points.

Disc: Not invested but on watchlist to invest at reasonable valuations.