Fellow Value Pickers,

Does anyone have any idea about the recent run-up in the stock? Any news that I have missed or some big investor has entered into the stock or it is pure speculation?

Any views are invited.

Thanks,

Mukul

Fellow Value Pickers,

Does anyone have any idea about the recent run-up in the stock? Any news that I have missed or some big investor has entered into the stock or it is pure speculation?

Any views are invited.

Thanks,

Mukul

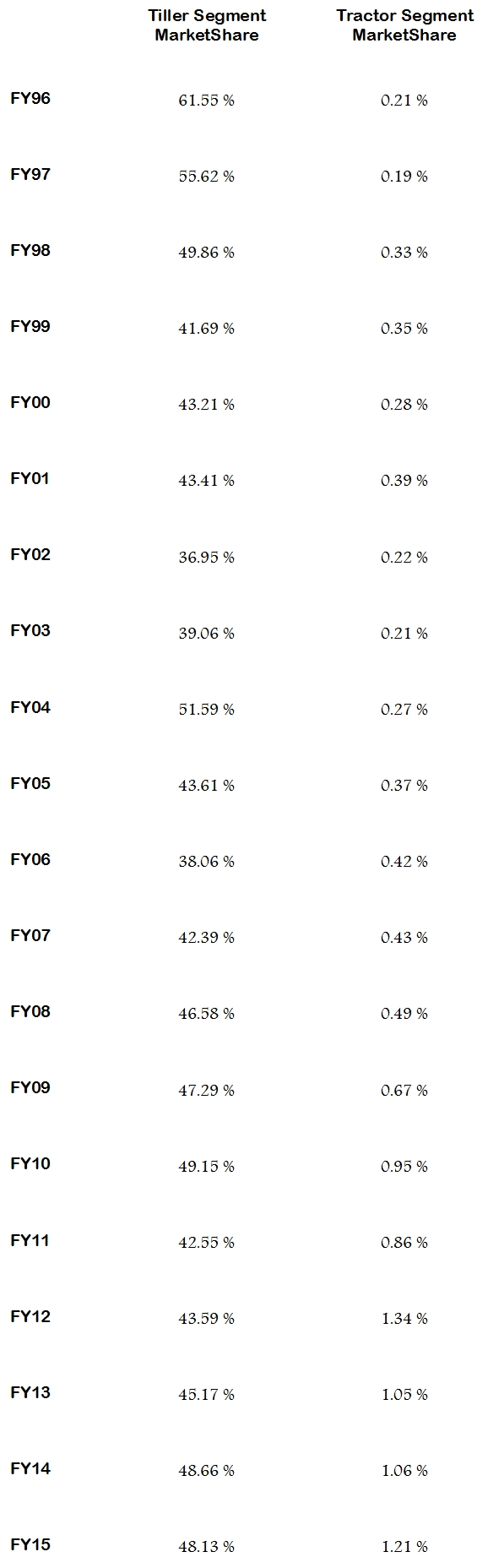

Some statistics on the company :

VST Tillers Overall MarketShare for 20 Years in Indian Tillers & Tractor Market

Notes :

(1) While counting marketshare for Tractors, entire domestic tractor sales are considered rather than below 30 hp tractors.

(2) Since 1998, despite many odds, company has more or less maintained 40 % + marketshare in Tillers market.

(3) Since FY04, company has steadily improved its marketshare in tractor segment.

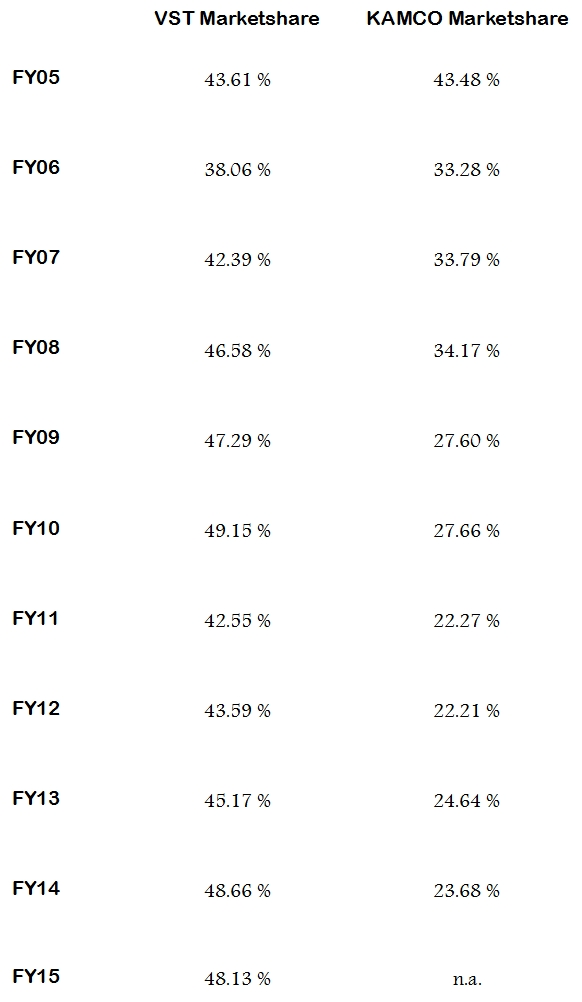

VST Tiller Marketshare v/s KAMCO marketshare for last 10 Years

Note :

(1) From almost similar marketshares enjoyed by VST & KAMCO in FY05, whereas VST has maintained & infact improved its marketshare over last 10 years, KAMCO has seen its marketshare halve.

(2) It seems aggressiveness of other players in the market as well as import threat has more affected KAMCO than VST.

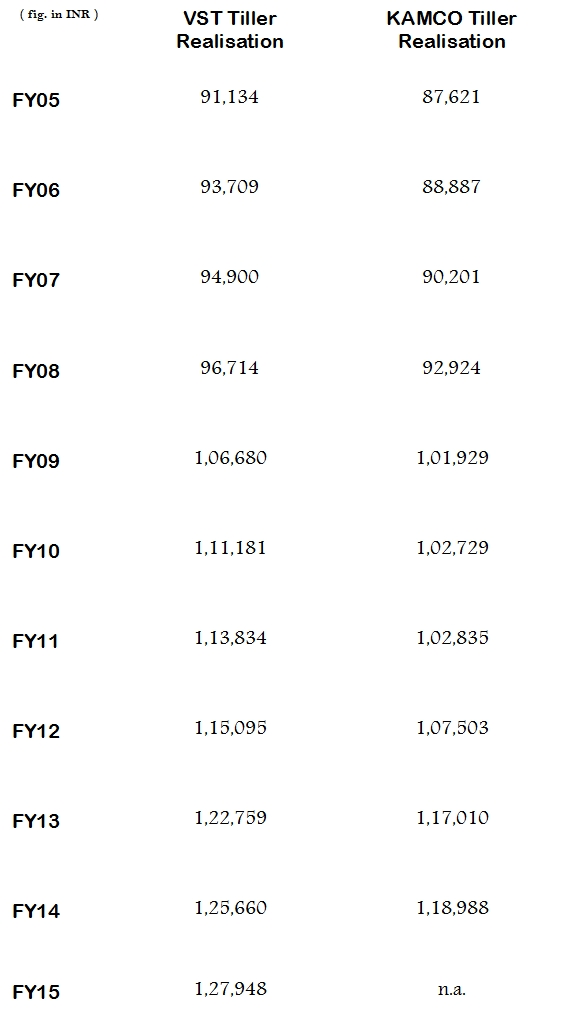

VST Tiller Realisation v/s KAMCO Tiller Realisation over last 10 Years

Note :

(1) VST has always enjoyed superior realisation for its products vis-a-vis KAMCO.

(2) Both the companies have registered gradual increase in realisation over last 10 years.

Rgds.

Discl. - Buying in VST Tillers initiated over last two weeks.Forms ~2 % of family portfolio atpresent.

Note - This is not a Buy/Sell/Hold recommendation of any kind and is just representation of statistical facts and figures. Here, Indian Tractor & Tiller industry statistics is provided alongwith marketshare of some of the major India players and should only be used as a tool for further research and not otherwise.

Recently this company came on my screener as well as mind palace ( watching TV commercial). Good numbers, attractive valuations but nobody seems interested in this stock. Any other problem than Liquidity ????

here are some links

https://www.kalink.co.kr

for the Korean maker

Here is the old news item about alloy wheel tie up with Kalink and the investment at 640

http://www.vccircle.com/news/engineering/2015/09/21/south-koreas-kalink-invest-steel-strips-wheels

PS - got a tracking position today at 384. Debt to Equity certainly scared me and I was fearful of another Ahmednagar forging type story (now, Metalyst )...what made me change my mind is the tie up and improving margin..if u take out the outerlayer of march'14 out, the rest of the net profit looks bearable, if not making you fall out of the chair. looking for no miracles here and hence expectations are low

We can get it after listing at good price I suppose,provided all investing parameters r ok.I will wait n watch.We must not depend on Devi Setti image...

yes, i am .... although booked part profits between 400-420 (lucky that's all) but i am still holding a major chunk. I am very bullish on the stock and if it were to touch 30 day moving average i would be buying back my quantity (and ofcourse if i do not get anything more interesting). there is a good chance that today or tomorrow it could stop its LC journey and if not then 30 day moving average could be a great bargain buy for new guys.

One of the concerns seems to be the shift in the advertising spend pie from print to digital. This certainly impacts the long term prospects for newspaper companies. While advertising spend on print is growing at ~5% the proportion of total advertising spend it represents is shrinking.

The following link provides some useful statistics.

Kind of following Byke from last 2 years but gave it a pass due to high PE in high capex industry. Over the years price has been stable and P/E corrected. In my opinion,

1. Liked the business model of selecting heritage sites for hotel business where customers are kind of not impacted by recession etc.

2. Presence in metros in less which is advantage of having less lease costs.

3. Asset light model through room chartering and leasing.

4. Seems like they can replicate the so far success story to other cities ( read the similar kind of hotel business from One Up)

Threats/questions

Discl: Entered at Rs: 152 - 3% of PF.

No, it's not separate. The 10 boats mentioned in the release to the exchange (and also the tender) are for the IFR. Minimum period of hire is 15 days, which is specified in the tender.

Look like all are making pass just got subscribed 30% as of now