Well, not a single multibagger, not a single defensive to create long term wealth, not a single known name to play safe, all speculative.

BKT

SBI

NMDC

are below avg. but compounders

Well, not a single multibagger, not a single defensive to create long term wealth, not a single known name to play safe, all speculative.

BKT

SBI

NMDC

are below avg. but compounders

I hate to talk like a boss, but got info that big heads of Telugu land and film industry biggies are buying heavily into Neuland Labs. They were the same ones who took Auro Pharma up and then sold to FII's their families are all connected and hence they ask them to buy at market as a favour, so I dont want to discuss the names but I give you a hint that they are a pack and they all have it in their own names. Their families are in telugu film industry and politics.

Disc: Not invested, but looking to get in at a dip. Momentum too strong

the classy way you put it, I liked it. I think with Venkats hardwork and their team they will do something by 2017. Suven can be a multibagger

Dear All,

With all due respect.

I use to track this scrip when it was around Rs. 30 (2.5 years back) and bought decent quantity as well but exited at Rs 55.

Few Red flags which I noticed at that time were:

1) At that time there was no separate website. They have one group website.

http://www.chiripalgroup.com/index.php?page=manufacture_home&id=7

2) Other unlisted entities which are also into textile division. Not able to understand why they got listed only one entity and not others.

3) CFO (Mr. sanjay Agarwal) said pledge share was due to loan taken for other group companies but not for NDL.

4) Criminal case against its promoter and other group companies.

http://www.chiripalgroup.com/Right%20Issue-Final%20Lof-14-12-07.pdf

5) Lavish lifestyle of promoter. (This may not be the concern of many but I personally look for it).

Almost after 6 months of my tracking Crisil came out with Buy report and at that time only, long stuck Orange Mauritius Investments Ltd exited from the stock and Globe Capital Market Ltd & New Leaina Investments Ltd entered. Thereafter, promoter started buying and Dolly Khanna (Globe Capital Market Ltd exited) entered in the range of Rs 60-65 from where stock sky rocketed and touched Rs 170.

Contradictory event,

Promoter is buying shares through open market but not releasing its pledge shares rather diluting it through issue of warrants at higher price.

Is below situation possible?

Raise money by pledging shares ------ start buying (at lower price) in open market to attract investors-------roped in well known punters and take the price to higher levels------dump the stock either by issue of warrants or QIP at higher price-----Enjoy holiday in Las Vegas….

[Just a view]

Regards,

Dics: I am a long term holder of Pix

Now what happened in the stock markets is not our business, but its still doing well, its paying dividends, its creating wealth and most of all Somi Belts is not a real competition as its the only listed Indian company as Pix has foreign promoter and great experience in doing the job, as soon as india picks up, we need machinery and they needs Material Handling that can only happen using belts provided by these guys, they supply many belts for various industries and have a great reputation. I think there will come a day when every Indian company making some thing needs MH and convener belts are going to be used, then you wont get Pix at Market Capt to Cash Flow: 2.18. I am positive the days inventory outstanding will reduce.

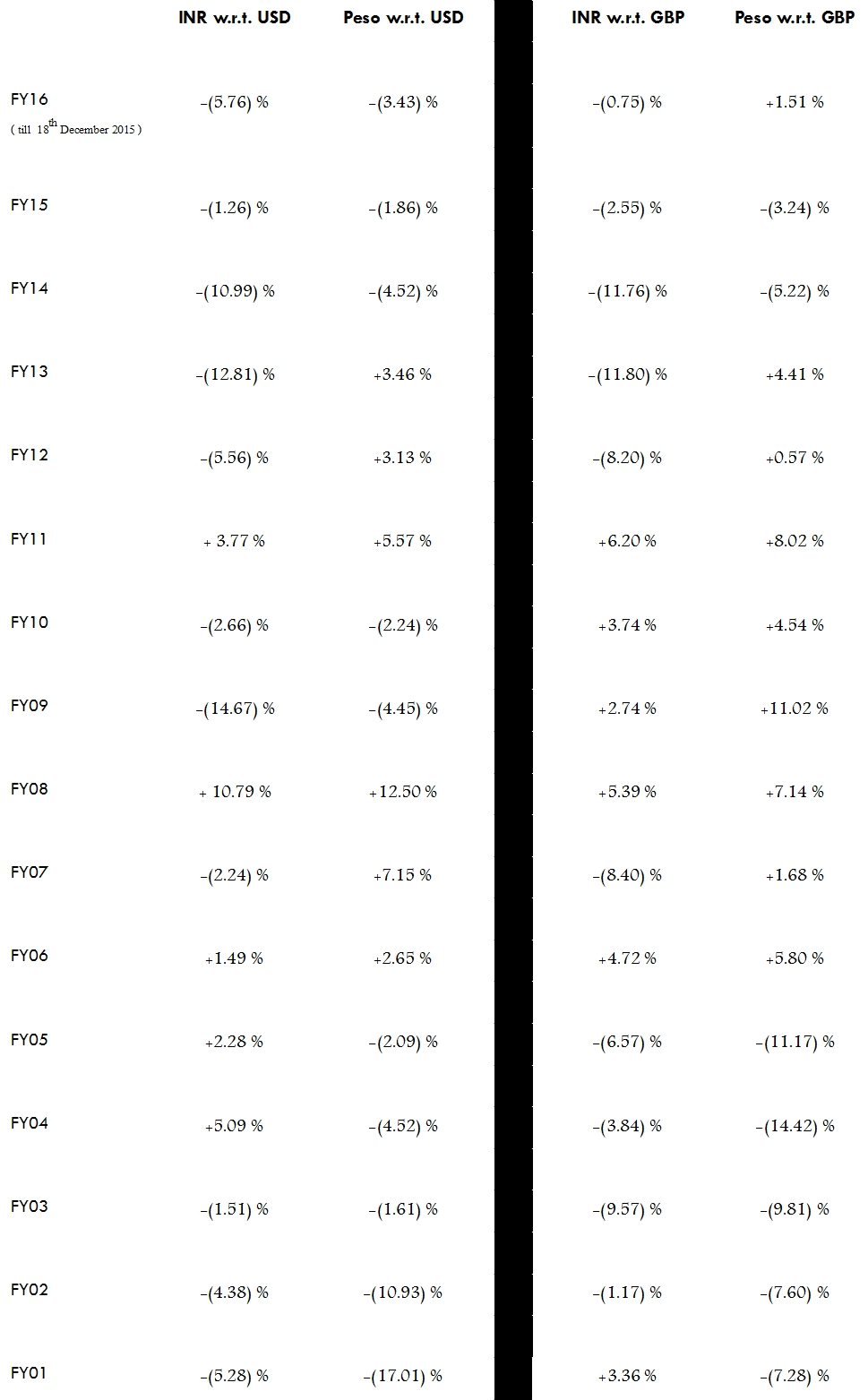

Some Macro Observations :

Currency Benefit

India & Philippines account for bulk of the publishing outsourcing industry. It will be interesting to note respective countries' currency appreciation/depreciation trend w.r.t. USD and GBP (since these two are the major billing currencies for MPS) :

Key things to note :

-- Philippines currency Peso provided the country major advantage till FY09 vis-a-vis INR post which relatively strong INR depreciation v/s both, USD & GBP made India much more competitive than Philippines (only w.r.t. currency we are talking about).

-- Peso overall depreciated by average ~15 % v/s USD & GBP in this 15 years of our study whereas INR depreciated by average ~40 % v/s USD & GBP over the same period.

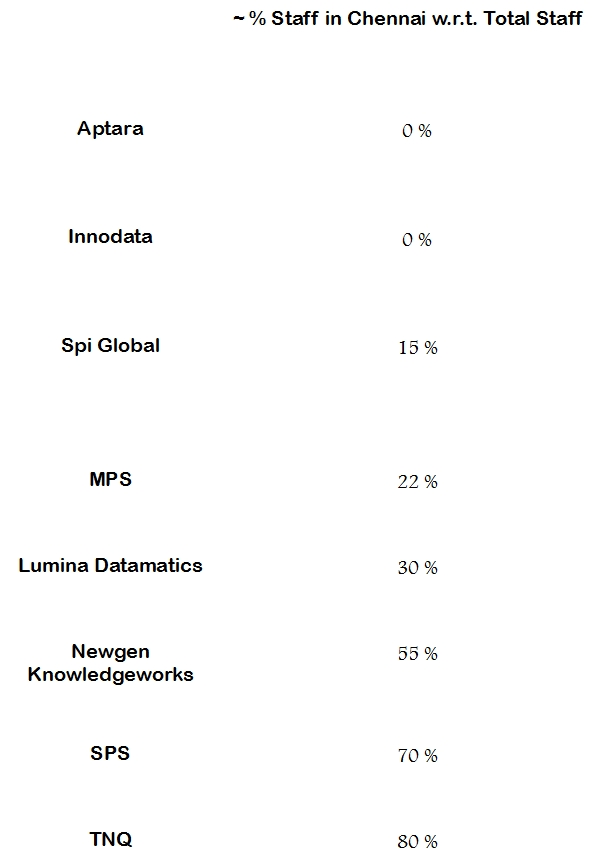

Chennai Floods & H1B Visa controversy Impact on MPS

H1B visa issue might not have material impact on MPS as majority of its overseas staff seems to be local.

Chennai Floods could have an impact on Q3 performance of MPS as ~22 % of its total staff strength is placed in chennai . Also, chennai seems to exclusively cater to LNMS division of MPS as also forms major part of 'Digital Services' division which together account for ~14 % of yearly revenue. In addition, it also caters to 'Books & Journals'.

In absence of any warning from the company, we can't say for sure whether there will be any impact or not and it could be that major portion of the work might have been temporarily shifted to other locations to avoid any impact. Also, 'Guindy' area where MPS facilities are located seems to have been somewhat impacted by floods but to what extent the area was affected that we can't say unless any VP localite member has any info.

Just to compare, MPS seems to be well placed as compared to many of its peers except Aptara, Innodata and SPi as far as chennai situation goes. Providing below approximate operation size of major publishing outsourcing players from chennai :

Rgds.

Genomal Bros' story. Most of it is very well known but a few sentences are reassuring for investors.

'This is just the beginning of our growth story. The best days of Jockey in India are ahead of it.'

Disc.: Trimmed some % but one of the large holdings.

This is a good portfolio with concentration of few good businesses.

About Financial stocks, I also feel that, 2 stocks would be sufficient for such concentrated portfolio. HDFC Bank and Repco look solid businesses with low NPA, high ROE and consistent PAT growth.

Addition of any engineering company may add some value to portfolio, and exposure to this sector may give relatively higher returns if economic turn around and infrastructure growth picks up.

Also, addition of auto stock which is reasonably valued can add value to portfolio.

As long as they remain as "NBFC-MFI", there could be political interference. But with active RBI these days and with passage of MFI bill, these risks would come down. Also, MFI industry does a lot of good for its customers who otherwise have to fall prey to loan sharks. RBI as well as government knows this very well after the AP fiasco. Recent call money scam in AP must also do a lot of good to MFI industry as people would get to know about MFIs who lend with proper regulations in place.

Once these NBFC-MFIs get converted to small bank finance companies and later into universal banks, the political risks will die down. But, for me personally, the moolah is in MFI lending as long as you can keep the NPAs in check and follow proper risk management principles.

Any investment is fraught with inherent risks, we need to take a call weighing the risks vs. reward, according to one's own risk taking ability and knowledge of that particular sector.