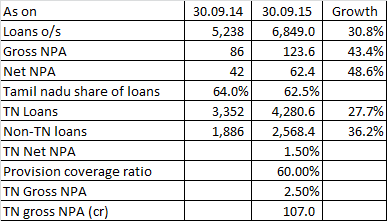

To try and guage the impact of Tamil Nadu (TN) floods, lets look at a few numbers:

Assume TN loans don’t grow (this is debatable, as there may be opportunities to lend for home redevelopment)

Assume TN gross NPA doubles to 5% of the loans outstanding (I think this is possible and maybe conservative assumption, given that loan repayment would be the last thing on the mind in current situation)

While this will not have to be provided immediately on default, it will attract 25% provision after 90 days.

![]()

The additional provision of Rs 53.5 cr (25% of gross NPA) appears significant considering FY15 PAT of 123cr and H1-FY16 PAT of 69 cr

One argument is that the loan would have to be classified as NPA only upon default extending over 90 days. In the next 3 months, it is possible that some of the borrowers are able to stabilise and resume their repayment. Upon full stabilisation, which could be 6-9 months away, and clearing off all the overdues, these loans can be re-classified as normal, leading to write-back of earlier provisions. Therefore, any adverse impact on financials might be a temporary situation.

Another is that the company can try and focus to compensate the situation by growing the non-TN book so that the overall impact is minimised.

A black-swan (sorry for use of the term) event could be that RBI gives a temporary concession/reprieve to banks and financial institutions to defer recognition of NPAs due to the floods situation.

Disclosure: I anticipate a spike in NPA over the next 2 quarters, impact on loan growth rates that the company has been posting till now, and impact on income and profits of the company (how much impact I am not able to gauge - and the above exercise is only an inexact attempt to quantify the discussions surrounding the topic).

Hence I reduced by holding by 20% at 690-700 levels recently. It still remains one of my top holdings and I remain convinced about the long term story. I will buy back my position if the price corrects significantly from here.