@nagpal, yes that is true. Also it has has started incurring higher depreciation from new factories where as full top and bottomline benefits are yet to accrue. Better valuation metrics would be to consider Price to Sales which makes it look cheap .

Posts in category Value Pickr

Agro Tech Foods – A small cap MNC foods FMCG (09-12-2015)

My take if Advertisement expenses are increased this should increase earning , Even If co stops advertising then also earning will increase being major expense . In theory if co stops advertisement for one year this stock will be 20 p/e stock.In future as brand becomes established the ratio of advertisement exp to sales will keep coming down which will be eps assertive.Dis :Small Exposure

Torrent Pharma Ltd (08-12-2015)

Just to add to Hitesh Bhai's point: Currently the pharma sector (large caps) are going through some kind of re-rating. People have seen what USFDA issues have done to IPCA, Dr. Reddy's and Sun Pharma. Most of the time market tends to overplay the negative/positive news. In case of Torrent multiple factors such as the sectoral derating, perceived absence of long term pipeline combined with the overall decline in equities is playing out. FDIs have pulled out massive money from the markets and Pharma was their sector. At the same time torrent with a market cap of nearly 25000 crores is actually a large mid-cap and it will not move into a different orbit without institutional interest (a 25% movement requires 1B $) unlike the sub 2000 crore market cap companies.

I have found a strange kind of herd mentality in how funds behave, they are fine being collectively wrong instead of taking a risk of standing out and being right. As far as numbers are concerned, for torrent it is relatively easy to work out (rough idea of marketshare of various formulation their prices the taxes paid etc.) As Hitesh Bhai said a rise in earnings will be followed by a rise in money paid out to investors and sustained performance and other superior business parameters will force the market to notice it. The same funds which shun companies come around again with a different set of reasons. I would advise you to go through their conf calls where they talk of their dividend payout ratio and upcoming surprises. Finally quoting Buffet "In the short run the markets are a voting machine but in the longer run they are a weighing machine". Go through the story, build your own conviction, assess the risks anxd take a call.

DIsclosure: Invested. Forms more than 10% of my portfolio.

GoodLuck Steel Tubes (08-12-2015)

Having tracked the company:

Positives:

Technocrat Promoters( IIT ians)

Company adamant on improving margins..the same is reflected in recent results with flat sales but booming margins.

Company expanding into a new plant in Gujarat to be close to port and improve export benefit.

Good Promoter Stake

Low PE of 6

Company has been consistently generating good cash flows out doing PAT figures consistently

Company has gotten licensed to be a supplier for Indian Railways.

Orderbook for Solar structures good for 1 year.

Negatives:

Substantial capex of 300 crores in next couple of years

Dependence on capex by government

Overall though can see a vast opportunity ahead for the copany specially considering the sectors the company is in .

Disclosure: Invested

Arman Financial Services Ltd (08-12-2015)

Having listened to multiple confrence calls from the management, absolutely delighted with the great information disbursal by them despite being such a small player limited to only Gujarat and MP

Somi Coveyor Belts (08-12-2015)

A link describing cartelisation among conveyor belt cos.,

Does presence of cartelisation imply belting is a commoditised industry?

Somi Coveyor Belts (08-12-2015)

Hi All,

Please have a look at Somi's competitor,Continental Belting,a private co. The following article and video provide some vital info on the industry.

I'm trying to understand what is a belting player's edge over its competition and where does Somi stand on these parameters? Is it the belting fabric? Is it consultation on optimum installation of belts,because its not a plain vanilla application for all and seems lot of customisation is involved? Or is it providing every efficient solution on lowest energy cost/tonne of material handling?

Also,why has Somi given such aggressive targets,we know industry is not so robust both in India and globally? The new product steel cord belts is already being provided by a few players,Continental Beltings being one.

Views invited.

If you CAN’T BOTHER to research/present a BALANCED view with decent RISK assessment, you have NO RIGHTS to start a thread on that business (08-12-2015)

This thread has served its purpose and is now being unpinned/closed.

Today VP audience and readership consists of different kinds of folks with possibly different ideas of how to use a platform like VP to the best advantage.

It again bears re-iteration that for those whose primary purpose at VP is to generate/receive workable ideas, BUT

a) cannot write a balanced post - adhering to VP Guidelines

b) cannot respond/examine counter-arguments to one's invested ideas, and/or

c) do not have the TIME to work further on his/her proposed idea

please DO NOT use the Stocks Opportunity section.

Should you want to just POINT to a new idea with growth momentum or turnaround in fortunes, or change in Management, etc and find that there is no existing thread on that, please use the Company Q&A section instead, that is free-format and does not impose any limitations.

We expect everyone to respect/adhere to VP Guidelines - it is for our own good. If you are a responsible member, you will not expect other members/moderators/admin to clean up after you.

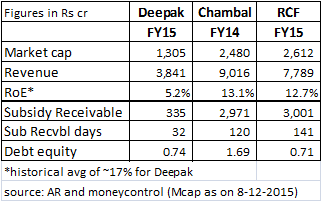

Deepak Fertilizers and Petrochemicals (08-12-2015)

Deepak Fertilizers had Rs 334.98 crore of subsidy receivables due as on March 2015 (Page 127 of 2015 AR). Compared to this, revenue for the year stood at Rs 3841 crore (Page 111). The company therefore seems to be relatively better placed in terms of subsidy dues.

This is the link where moneycontrol says that "news are doing rounds" about delay in payment of arrears from the government this year:

http://www.moneycontrol.com/news/business/subsidy-arrears-low-urea-prices-may-dampen-growth-zuari-_4505801.html?utm_source=IW_DATA_stockpage