Thanks admin for re-opening the thread.

I hope all members on the forum will take due diligence to post balanced views.

Thanks admin for re-opening the thread.

I hope all members on the forum will take due diligence to post balanced views.

“Suven Initiates Phase 2A trial of SUVN-502 in USA in Alzheimer’s Disease”

SuvenLifeSciencesLimited (2).pdf (103.5 KB)

Great Share Malik, very helpful. Indeed, the conviction is increasing day after day.

ok... after multiple attempts, was able to get through to the company folks.

They were forthcoming and here are some of the observations.

-their foray into steel conveyor belts is indeed a big event. The pricing of this @ 3000/m is almost 4times the normal belt. The life is these belts is much better at 4 years as compared to 12-18 months for normal belts makes this more attractive for clients. Also, this requires less maintenance.

there was a delay in getting this product in place and so they had subdued q1 and q2. But they indicated that q3 and q4 should be substantially better and they should easily cross 100 cr for the year.

Also send next year should be much better. Close to their guidance. So perhaps 200 cr at a pat of 12% would mean an eps of close to 20. I think at a minimum u should give at 10 p/e for the growth rates they can sustain, but make ur call.

The industry is still dominated by small players and clients are largely psu's where price is the most important determinant without major emphasis on quality.

So in pvt sector bids, they easily win, but is not so the case with psu's like NLC. But the market size is huge (I don't remember exactly, but I think NLC alone is 200 cr/year). So with their competencies they should be able to scale up.

I checked with some local folks and they had good things to say about Somi and the Bhansali's. But I don't know the source all that well and since he is from the local pollution control board, I don't know what this means.

p.s I hold a position - a medium one.

@neil991 any updates on this one. Did anyone attend the AGM of this company this year. If yes can you please share the notes

Disclosure: Invested

everyone seems to have a view and at times everyone sounds right. Let me add my 0.5 cents here (I know that it VP maturity index, that is all I am worth !!). I think, @subashnayak_19 has been given a prompt rejoinder and that is a fair ask since he is veteran, who has made significant contribution. That said, converting this tag line to what it is now is probably stretching the point. My simple addition - if one says that he or she is not qualified to right about the risks since they are not veterans of this industry, then the opinion must be respected. afterall, this forum is for discussing it further. (Agreed that it has to be in the right section but it is a simple move by the admin)...keep it coming Subash .....

Business

Renaissance Jewellery is involved in designing, manufacture & sales of jewellery of silver, gold, platinum. Jewellery studded with diamonds and other precious & semi precious stones.

Jewellery products include rings, pendants, earrings, bracelets, necklaces & bangles.

Company sells jewellery to large retailers, speciality jewellery chains and online portal.

Company is also into readymade furniture - "Housefull Store" across 38 stores.

Industry Outlook

According to Research & Markets the sector in India is expected to grow at CAGR of 16% over 2014-1019.

Domestic gems & jewellery industry has a market size of $40b in 2013, has a potential to grow to $80b by 2018

Financials

Q2FY16

Long Term Debt = 0

Short Term Debt = 344cr

Non-current Investment = 0

Cash = 34cr

Current Investment = 29cr

Current Assets = 989 cr

Current Liability = 672 cr

Key Concerns

Positives

Disclosure

Invested with tracking positions

"Board of directors of the company today has accorded in-principle approval for exploring consolidation options with Tree House," says Umesh Pradhan, CFO of Zee Learn.

Read more at: http://www.moneycontrol.com/news/business/zee-learn-vs-tree-house-who-isbig-fish_4462961.html?utm_source=ref_article

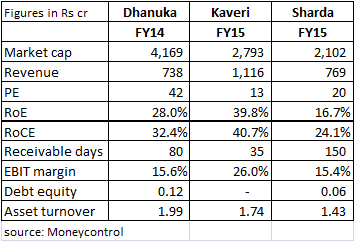

Kaveri might be attractively valued right now compared to peers:

@mukesh_gt

Dear Mukesh, nice to meet you.

Myself a Transformer Design Engineer.

You are correct that Transformer Industry is at cut-throat competition.

Especially distribution transformers are became like a commodity product. There is no rocket science involved in making distribution transformer. Hence there is no moat, There are hundreds of distribution transformer companies in India. Recently ABB shutdown its plant because of high supply and less demand.

Only power transformers business above 220kV can offer entry barriers in terms of Product approval from state board and Product technology. Power transformer business also suffering with surplus capacity and lower utilization levels. But there is hope in the industry that demand will pickup in near future. Recently announced reform UDAY is a boon to the industry if it could implemented by states.

Look at less stressed power transformer companies like TRIL. They will be the major beneficiaries of this reform. Read this article http://wap.business-standard.com/article/companies/power-equipment-manufacturers-expect-uday-to-boost-order-flow-115120300835_1.html

Disclosure :

Not invested in Voltamp

Little position in TRIL