Decent set of numbers in this environment. Even the dividend is consistently being increased. I too am in a dilemma. There are so many companies reporting massive degrowth in sales and/or profit. at least this one is showing some growth. The TTM PE is now 67. ( looks good compared to 90 plus PE it had a few months ago). that gives some comfort

discl: invested since 2010. no buy/sell in last one year.

Posts in category Value Pickr

Page industries (09-11-2015)

Indian terrain—play on consumption (09-11-2015)

True.

Read in AB nuvo annual report that Madura is delivering 70% roce. Please let me know where can I get detailed balance sheet, profit and loss and cash flow of Madura garments. This would help to compare as to whats main difference and why is Indian terrain not able to get that ROCE or why is Madura garments getting that ROCE.

thanks for your valuable inputs.

Tasty Bites: A proxy play to India’s QSR industry (09-11-2015)

Hi Bhaumik - Please write to Kagome Japan and try your luck. Being a publicly listed company, they might be obligated to send if enough of us write in.

Anyway, stellar results from Tasty Bites - http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/E50EA6CF_42E2_40C1_BE43_86E6D535822D_152901.pdf

16% sales growth, 67% profit growth. On track to cross 50 rupees EPS for FY16.

Disc: Invested. No transactions for last 30 days.

Avanti Feeds (09-11-2015)

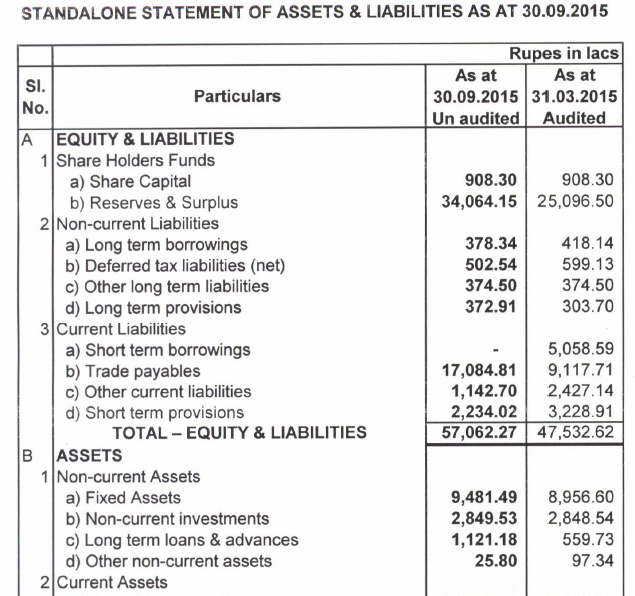

Excellent Accounting stuff explanation Ashwini. I never thought there would be a difference in classifcation of trade payables vs current liabilities and between RM and logistics cost. Thanks much.

Thanks Varadha. Looks like unless you are a private equity fund, you can't pass a inventory writedown just via the balance sheet - ( https://foragerfunds.com/bristlemouth/dick-smith-is-the-greatest-private-equity-heist-of-all-time/ )

Thanks Ayush. Given the nature of Avanti's business, it would be unfair to compare Q4 to Q2 balance sheet. I was trying to understand the flow of business YOY. But your re-classification point is well taken.

My confusion stemmed from the fact that given Avanti wanted to ramp up shrimp processing (as feed business can only take it so far - or so, it seems from the surface), it was only logical that they might have procured shrimp from farmers (apart from in-house production) in exchange for selling them feed. This might have bloated trade payables. But then again, shrimp processing revenues (volume not given unfortunately) has steeply fallen. So, there was a dichotomy.

But if it's just re-classification, then we should be ok. Balance sheet is anyway quite strong.

Kiran

Avanti Feeds (09-11-2015)

I just re-went through the post of @dkirand. I think the confusion will go away if we compare the balance sheet posted by the company:

The major variation between trade payable and current liability seems to be due to reclassification of heads.

Regarding the point raised by @varadharajanr, the provisions have reduced from 32 Cr as on March 2015 to 22 Cr as on Sept 2015 and these could be general in nature.

Regards,

Ayush

Ujaas Energy – Value Migration to Solar Power (09-11-2015)

Some critical points from Concall :-

Management refrained from giving any guidance but said that now they are back on track like the year 2013-14.

They are currently managing 130MW solar plants.

They have bid book of 100MW out of which they are L1 in 60MW (might be that NHPC order).

They've bagged 9MW -West Bengal order plus 10MW - Oil India Order.From long term perspective, Government has target of 100GW by 2022. They said that they would grow 6-7x times of Solar Industry in India. Anurag Mundra did mention that they would be

managing around 5,000 - 7,000 MW in next 5-7 years. i.e. around 50x Company has not yet entered the Household rooftop market.

For Rooftop business, there are two critical points - a. Enforcement of Net Metering Policy & b. A product which will suit the households with less installation time.

They are developing a solution for this market. In coming 2-3 qtrs, they will try to come up with that.During the financial restructuring of various Discoms, there's a condition for them to be RPO compliant. Anurag feels that it will be a good kicker for them. He sees situation improving in coming qtrs.

Apart from these points, other points were redundant though chances are there that I may miss some points

Discl: Invested small amount to track the company.

Styrolution ABS – MNC due for rerating (09-11-2015)

Call was addr by Myung Suk Chi MD & CEO.Highlights by Capital Mkt

The company has capacity of about 110000 MT of ABS and is operating around 75% of installed capacity.Of the total sales, about 87% is ABS sales and rests are SAN products.In terms of market share, overall, the company has market share of about 44% in ABS in India and about 50% in SAN. Almost 75% of SAN produced by the company is consumed in house.

The company had an inventory gain in June'15 quarter and inventory loss in Sep'15 quarter. Net to net things mostly even out in H1 FY'16. At steady state of inventory, the gross margin of the company is around 28%.Management expects the merger with Styrolution Pvt ltd to be completed by end of Mar'16.As per the management, they are not focused on exports and their entire focus remains on India.After Styrolution ABS, Bhansali Engineering is the 2nd largest player with about 20% market share and about 25% of total demand is met through imports.

Automobiles and Consumer durable account for significant demand for company's final product, ABS. within automobiles,2 Wheelers particularly bikes account for major demand followed by passenger car vehicles. All consumer durables be it refrigerator, washing machine, mixer etc require ABS.The slower rural economy has affected the demand of bikes and consumer durables. As per the management, there is a demand and demand will increase if the prices of raw material remains steady.

Going forward, new products and mixtures have been aimed and will be tested in H2 FY 2015-16. These products have higher realizations and increase the overall productivity of consumers as well.Overall, for FY'16, it's difficult to say the revenue growth as it depends upon crude oil prices, but management expects strong performance to continue.

Need for KYC to be enforced when Forum Abuse is detected (09-11-2015)

One thing for all members to remember to help maintain VP as the best-in-class forum is to be vigilant and flag posts which they think violates the ethos of the forum. Collectively we can make a difference in keeping out those who do not share the values of the forum.

Chembond Chemicals- A Perfect Misvalued Bet (09-11-2015)

Hi aditya,

Where did you get this figure from - 57% market share? Who are the other competitors in this niche?

Disc: Not invested.

Indian terrain—play on consumption (09-11-2015)

all of what you are saying is true - inspite of this being a big position for me, I shall say this again - this is the kind of business where cash has to be continuosly ploughed in for growth as they hold inventory. if they can work around that and palm this off to frnachisees/reduce WC days, it will generate FCF's - FCFs are what count for a shareholder., The issue is that this businesss linearly needs capital in consonance with topline growth (may be even more). IMHO, a more enduring moat comes from BS related efficiencies like asset turns, WC days and reducing capital deployed than from margins. Increasing amounts of capital locked in WC increase probability of black swans - obsolescence, write-offs, bad debts etc. -

Look at madura garments ROCE - its 70% and their WC is much better. ITFL is somewhere inbeween an arvind and a madura garments (part of ab nuvo). It's a good business but we just have to be cognizant of the cash flow issue here.