Hey Sumit,

Hope you’re doing well!

Its really inspiring about your journey into full-time investing. You mentioned starting an e-commerce business back in 2014 that sold print merchandise to the U.S. market. I’d love to hear more about that business. if possible, can u explain the business model, customers, marketing methods you used etc. basically I’m asking an entrepreneurship crash course from ur decadal business experience.

Thanks.

Posts in category Value Pickr

Sumit’s Portfolio (02-09-2024)

IDFC First Bank Limited (02-09-2024)

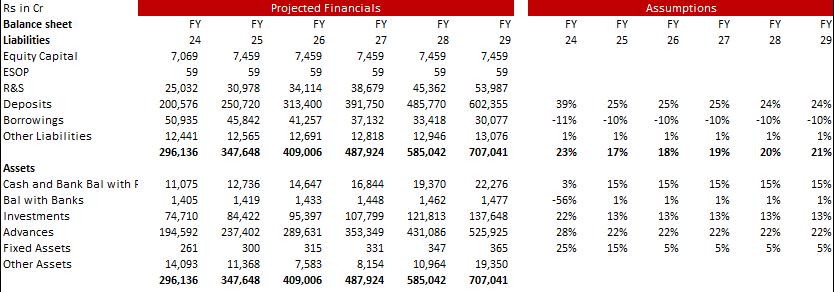

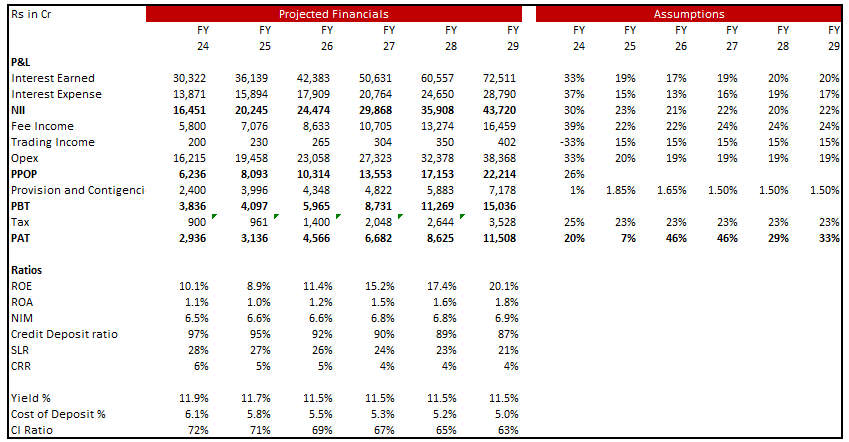

Here is my Projected Financials of IDFC First till FY 29 based on management guidance of few metrics in their Guidance 2.0 metrics and few of my own hypothesis

- Loans to grow annually at ~ 22% till FY 29

- Deposit to grow by 25% till FY 27 and 24% thereafter

- Borrowings to be keep reducing by 10% YOY

- NII to grow at CAGR of ~ 24% annually till FY 27 and then slow to ~ 20% ( have assumed drop in yield to be 40 bps in 5 years due to estimated repo rate drop ( almost 40% the book is not repo rate rate driven ) and assumed Cost of deposit to drop by almost 100 bps over next 5 years due to pay off of legacy bonds , reduction in repo rate )

- Fee Income to grow by 22-24% annually till FY 29 ( Assumed growth here to tapper from 35% -40% historically as many fees are waived off )

- Opex increase assumed to be 20% in FY 25 and 19% thereafter ; Cost to Income ratio to come down by 67% till FY 27 and 63% by FY 29

- Credit Cost to be 1.85% in FY 25 , 1.65% in FY 26 and 1.50% from FY 27 onwards

- ROA is coming to be 1.5% in FY 27 and 1.8% in FY 29

- PAT for FY 29 is coming at ~ 11500 Cr ;

- Have assumed no further equity dilution

Kindly critically examine these numbers and assumptions as to far these looks reasonable

Management has guided for 12-13k Cr of PAT in FY 29 with 1.8-2.0 ROA and 17-18% ROE and 7 lacs cr of Balance sheet size

Disc : Invested

Microcap momentum portfolio (02-09-2024)

Hi All,

Just FYI – @SOMASHEKAR_A_C and I worked on automating this flow and I would like to share this view only Google sheet with you all MomentumPortfolio_V3 – Google Sheets

I am very well aware that the results that I get from this sheet are a “little” different from the ones @visuarchie posts. But since I had offered to see if this flow can be automated I am posting my work here. If you wish to copy this sheet and automate your workflow you could do so. I have only given view access to this sheet, so you will need to copy it if you want to use it.

I don’t intend to keep this sheet updated every week ( at least don’t want to promise that ) and neither do I intend to post my stock picks here. I can’t be as punctual and methodical as @visuarchie so I will let him drive the forum. My intention of sharing the sheet is to contribute back and hopefully help others.

If you spend sometime with the sheet you will be able to understand how it works. Anyways a brief explanation follows

What are the different sheets

- Database: Contains data for all 750 stocks

- Microcap: Ranks the 250 microcap stocks by using the data in the Database sheet

- Smallcap: Ranks the 250 smallcap stocks by using the data in the Database sheet

- Midcap: Ranks the 150 midcap stocks by using the data in the Database sheet.

Where my approach differs

- I intentionally don’t select stocks that don’t have a 1 year history. Basically want to give equal treatment to all stocks. So if we intend to look at a 12 month and a 6 month lag performance all stocks need to pass that criteria. For example JYOTICNC was suggested on this forum but my sheet does not recommend that

- GOOGLEFINANCE() has a weird behavior that it sometimes omits the data for the last 2 days in a given date range. I have modified the sheet to live with this oddity.

- For microcap we were selecting 25 stocks out of the 250 stocks i.e. 10% of the universe. I decided to select the same number of stocks for smallcap as well i.e. select top 25 stocks from a universe of 250 smallcap stocks. If you decide to invest in only the top 20 stocks you could choose to do so

- The sheet automatically calculates which stocks should exit and which new ones you should invest in. For example, if you look into the Microcap sheet, cells D14 to K39 indicate which stocks to exit and which to enter. For example, my sheet told me to exit UFLEX and OPTIEMUS and invest in NETWEB and DHANUKA

Even if you dont intend to use the sheet, you could use some of the ideas from the sheet. For instance,

- @SOMASHEKAR_A_C gave a brilliant suggestion on how to use the GOOGLEFINANCE() function to fetch the stock data. Essentially a single call to the GOOGLEFINANCE() function can fetch data for a range of dates. This speeds up the data updation process significantly. How to use this function can be found as a comment on cell Database!B2. I have copy pasted the values from the GOOGLEFINANCE() call so you wont see the function call being made.

- The sheet uses some formulas to calculate which stocks to exit and which to enter. This can easily be done manually, but I wanted to automate this part and I learnt some interesting things on how to use Google sheets along the way.

Medplus Health Service second largest pharmacy retailer (02-09-2024)

I was reading about this company recently and just went about a background check on the promoter and the company through publicly available information. There is not too much out there but from what little I could gather we can see some points on how the company and the promoter has evolved from 2006 when the first stores came up

Promoter

The promoter has invested in other verticals in the past as well. In 2008 he had a failed start in apparel retail. In 2011 he launched something similar to Nykaa in online beauty retail. In 2014 he launched a venture in online furnishing space after raising funds from multiple investors. He comes off as a serial entrepreneur who wants to build businesses and then sell at a higher valuation considering one person cannot manage so many entities.

The business model has not grown with one model. Earlier in 2016 they were open to giving franchisees. In fact in one interview the promoter mentions that the franchise route will help them scale up to 10000 stores by 2019. This was in 2016. However by 2021 they had decided that they will open their own stores and were closing down the remaining franchisee as well post the IPO. The reason given was low margins in the business which will not allow them to make money.

The company has also recently gone full throttle on its own private label as well while partnering with two other listed entities namely Akums and Windlass for manufacturing MedPlus branded medicine which will be sold in its own store under the “MedPlus” brand so there seems to be a pivot from opening as many stores as possible to now serving own label products in the existing 4500 odd stores

There have been talks of sale of the whole business as well two times before the IPO where the promoter and other investors have offered shares for sale but the reason given has been valuation mismatches which is why the sale has fallen through. This along with the promoter starting other ventures though small, gives an impression that promoter might not be involved in the business for a long time

There were thoughts on raising more capital recently as well with the company passing an enabling resolution for a QIP but those seem to be on a hold for now going by the recent communication. Noticeably store openings have taken a back seat while diagnostics too seem to be a Hyderabad only play for now

E-pack durables – ODM worth a serious look (02-09-2024)

There are many companies in this industry doing very similar stuff. Almost everone makes similar products with similar margins. Any opinion on why epack is better? Purely looking at the numbers it seems like PG Electro makes better margins. Any understanding around why is that so?

The interesting thing I recently learnt about this whole space is that the size of the industry is growing and the size itself becomes a barrier to entry. So anyone entering today with big capacities and the established players are all going to be big beneficiaries.

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (02-09-2024)

The expanded capacity was to be utilised from 16th August. Anyone having an idea if the same has commenced since the capacity expansion had got delayed due to rains.

There hasn’t been any release post commencement of production from the same.

Sumit’s Portfolio (02-09-2024)

Portfolio Update –

Decided to exit Transteel after much deliberation. Despite good growth and rerating prospects, I wasn’t able to build conviction in this company. Here are my rationale for the decision –

-

Negative cashflow : Despite reporting profits, the compay has consistently shown negative free cash flow in recent years. This means the company is spending more cash than it’s generating, which could indicate potential liquidity issues. For example, in the fiscal year ending in March 2024, the company reported a net profit of ₹111.1 million but had a negative free cash flow of ₹422 million (Simply Wall St).

-

High Accrual Ratio: The company’s accrual ratio is quite high (0.66 for the year ending March 2024), which is generally considered a negative sign for future profitability. A high accrual ratio can suggest that the profits reported might not be sustainable(Simply Wall St).

-

Legal Proceedings and Regulatory Delays: Transteel Seating and its promoters are currently involved in ongoing legal proceedings. Additionally, there have been certain delays in submitting returns to various government authorities. These issues could lead to financial penalties or other regulatory actions, which might impact the company’s operations and reputation(FinoWings).

-

Lack of sufficient differentiation : I couldn’t find any significant differentiation in its business model indicating there could be margin pressure as it tries to scale its operations.

-

Poor customer reviews : As pointed earlier in the thread, the customers seem to be dissatisfied with its products and service.

-

Poor employee reviews : A cursory look at sites says that employees are unhappy in the company as well. (Ambitionbox).

Hero Motor – Leader in two wheeler (02-09-2024)

One of the bigger issues to come up with EVs, in my opinion, is when the battery will need to be replaced.

Just imagine, you have an 8 year old 2W, would you be willing to spend ₹30k-50k on new battery?

Instead, I would buy a new EV for ₹100k than spending ₹30-40k on an old scooter.

Which practically means the life of an EV gets reduced drastically to only 8 years compared to 15-20 years for ICE vehicles. That proposition is a big dampener and value-destructive from customer point of view.

I still feel people buying EVs don’t understand the above maths.

Only solution to the above issue would be drastic fall in prices of batteries, say, within 5 years.

Triton Valves Ltd – A Sleeping giant in tire and industrial valves (02-09-2024)

Hii,

I was going through the AR-2024 and came across this point.

During the year Company has filed Amalgamation

application before National Company Law Tribuna (NCLT),

Bangalore, seeking amalgamation of its fully owned

subsidiary Tritonvalves Climatech Private Limited with

the Company. Your Company expects to improve its cost

and customer focus due to the proposed amalgamation.

Why it is doing so?

Disc:- No Buy/sell recommendation. Not invested.

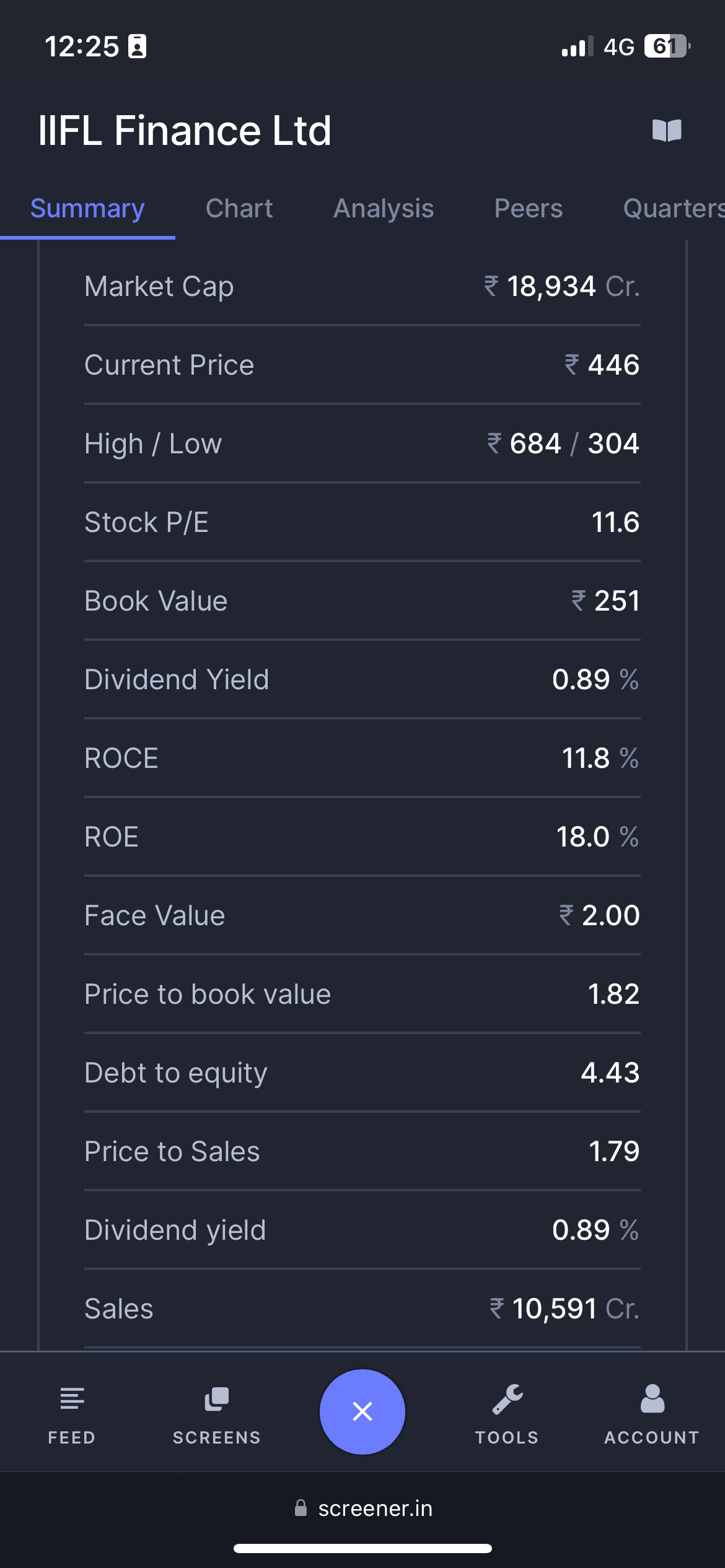

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (02-09-2024)

How are the stats different?