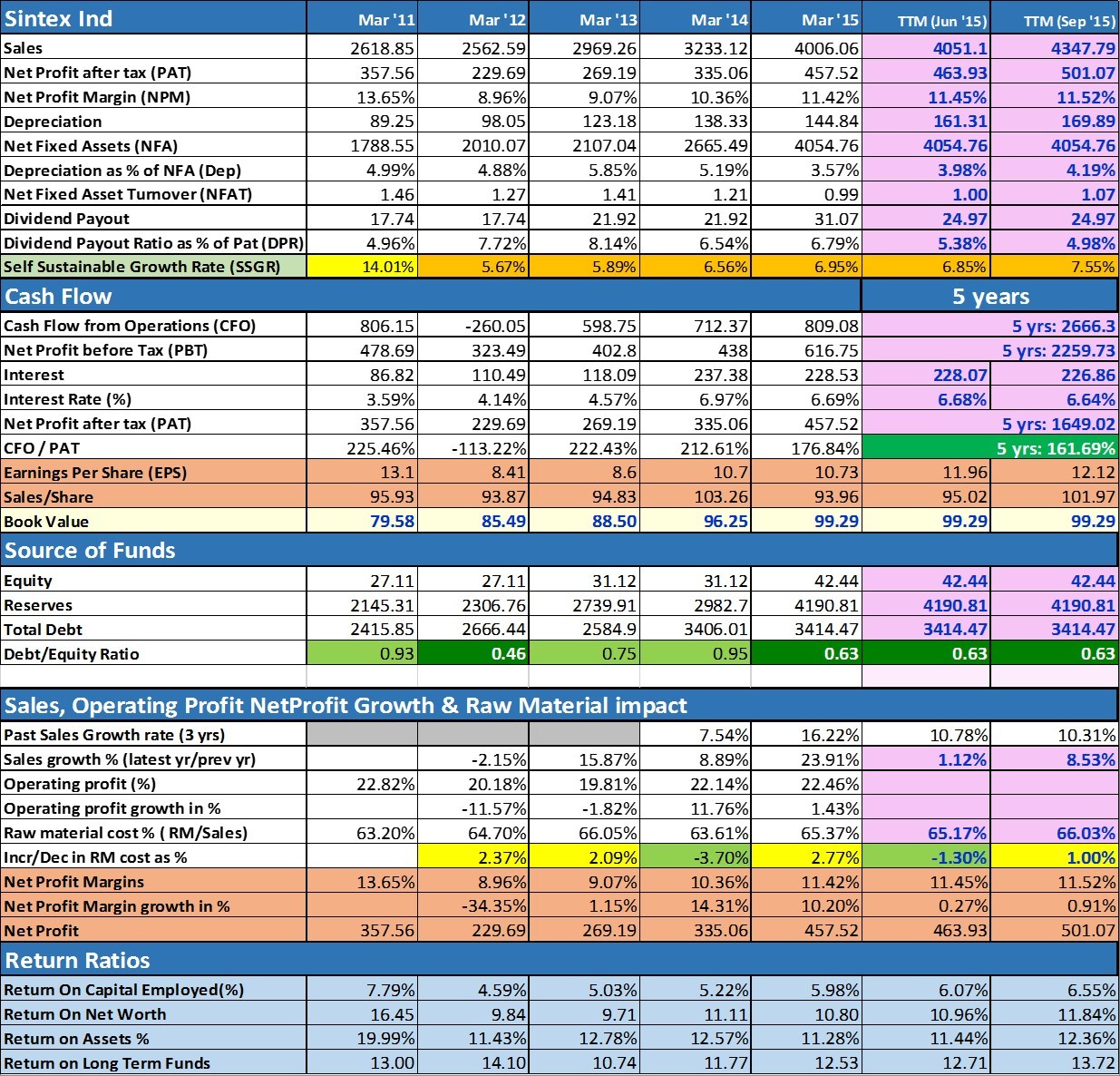

The company could do much better than this as discussed on this thread...

So so performance

I glanced at their Financial Statements for FY14 (FY15 has not yet been uploaded anywhere). Following amused me:

PBT according to the Cash Flow Stmt: Rs 4.20 cr

PBT according to the P&L Stmt: Rs 4.79 cr

Inventory Change according to the Cash Flow Stmt: Rs 4.61 cr

Inventory Change according to the Balance Sheet: Rs 1.55 cr

Total Working Capital Change according to the Cash Flow Stmt: Rs 4.01 cr

Total Working Capital Change according to the Balance Sheet: Rs 1.49 cr

I have no idea what to make of these Financial Statements.

Those having access to FY15 Financial Statements might want to comment on whether such inconsistencies exist in FY15 Stmts as well. If yes, all the reported figures lose their sanctity, unless someone is able to explain these inconsistencies.

this type of order base companies shouldn't be compared on QoQ, as revenue is spread across quarters. Skipper has excellent working capital strategy with cash conversion of 65 days. one should hold min 2-3 years to reap management effort

q2 results out. Its a mixed bag.

Topline grows from 75 crores in q2 fy 15 to 91 cr in q2 fy 16. which is quite encouraging.

Net profit flat at 6.61 crores. Main culprit here is increased employee expenses which increases from 4.3 to 7.3 crores.

Half yearly eps at 8 per share. Last year co did eps of 9 per share for full year.

If co can continue growth momentum in last two quarters this could become interesting.

disc: invested from lower levels. It was a techno funda bet for me.

Q2FY16 seems to be very good, company looks undiscovered by broader market at his point

Long term borrowing = 0

Short term borrowing = 2.9

therefore, Debt = 0

Non- Current Investment = 4.2 cr

Cash = 14.4 cr

Current Investment = 125cr

therefore Cash & Investment = 144cr

Net Profit q2fy16 = 16.6 cr growth = 27%

Market Cap = 512cr

To me it look like at deep discount at 30/-.

Some updates straight from the horse's mouth (Virat's management) post Q2 results as updated by a friend who spoke with management:

The reason behind sales de-growth is due to 2 months inauspicious period between July mid to September mid which comes once in 12-19 years and with no festivals/marriages etc Ghee off take was low... So sales were lower by 30-35% in Q2. This is both in AP and Orissa which was a double whammy.

Pent up demand will be seen in Q3/Q4.

Orissa production plant is in progress to start production by Q1 2017. The land is already procured and there is little CAPEX needed. So the incremental RoCE will be very high.

Karnataka foray is on track through the already established Crane Betal network and the response is good.

Management has started concentrating on Durga brand to make it a well established regional player. All the efforts will pay huge pay offs if story goes as per thesis.

The return ratios are improving and are best in the diary sector.

In my opinion, due to better financial metrics and pristine balance sheet, sticky nature of the FMCG product, brand power, high dividend payment the company deserves better valuations.

Disclosure: I hold Virat as indicated earlier. The details are already available publicly in internet.

@hssodhi198 Thank you.

Skipper Ltd Q2 net declines 14% to Rs 30 croreThe Kolkata-based firm had clocked a net profit of Rs 35.29 crore in the year ago period, it said in a BSE filing.

Read Full Story http://t.in.com/3XXL

Thanks.

@ Arun, I'm not too sure I totally agree with prof Bakshi on this. (Goes without saying, I'm an absolute nobody compared to him) but on his argument of functional equivalents.

Berkshire Hathaway, is Ben Graham's ultimate "frozen corporation" It never has, and has a stated policy of never paying dividends. It is a going concern and does not plan to liquidate either. So was Berkshire a bad investment candidate? (I am NOT even remotely saying that VLS is the same as Berkshire, or it's promoters are Warren Buffet) but since we were on the subject of functional equivalents, I can't see a better equivalent to VLS, than Berkshire.

I am not personally invested in the company because here's my logic. Let's assume I were the promoter (or you were for that matter in his shoes) what would I / you do? At cmp, I would sell about 1 / 1.5% of my relaxo holding and take VLS private. Therefore all the investments VLS has, in Ceat and in all the other companies now become my private investments. I am really surprised as to why the promoters haven't taken VLS private yet. If they can control the board of directors, I'm trying ti understand what is stopping them? They will win the vote on this issue, if ever one were to happen.