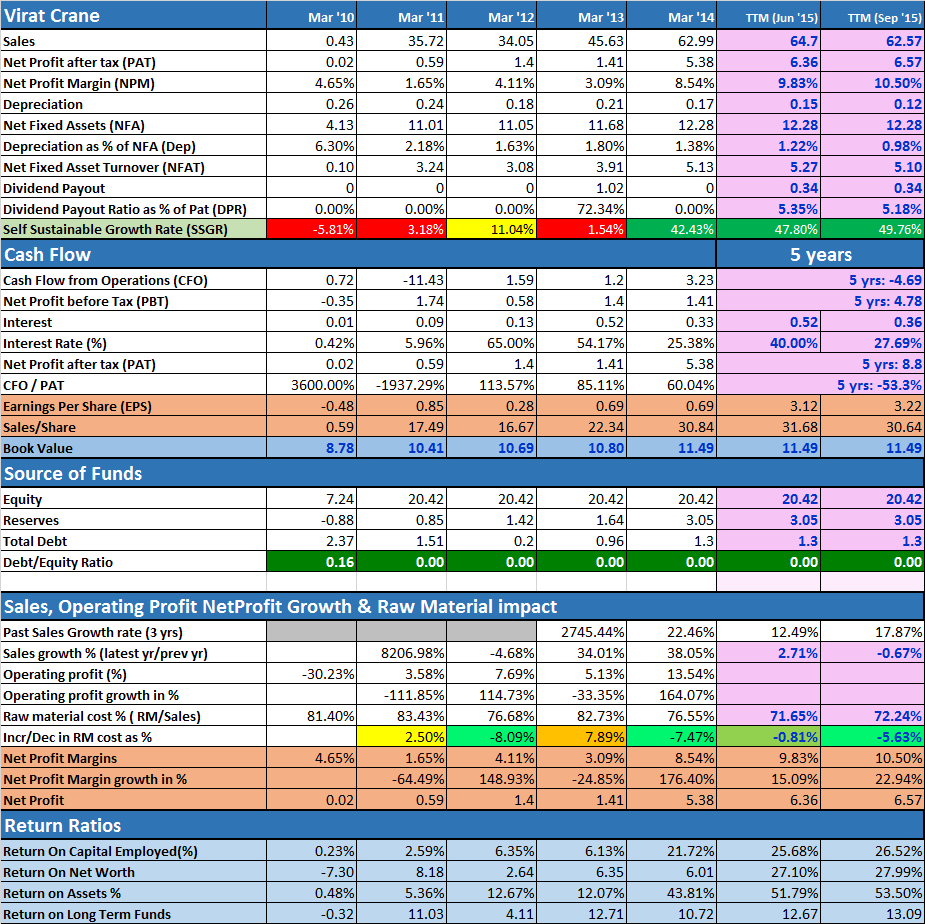

RM cost has improved in Sept-15 qtr.

Returns seems to be good.

The only problem is valuation.

Mold-Tek Packaging 2QFY16 results:

Net Sales: Rs. 638 mm, -19% yoy, -14% qoq Operating Expense: Rs. 538 mn, -21% yoy, -14% qoq. The fall in net sales is due to fall in crude prices which has impacted Poly Propylene, a key raw material.

EBITDA: Rs. 99.5 mn, -10% yoy & qoq. EBITDA margin at 16% in 2QFY16 vs 14% in 1QFY15. Margin expansion was due to higher share of IML products.

IML products share was 40% in this qtr vs 28% in 2QFY15. PAT was at Rs. 51 mn, up 13% yoy and -10% qoq.

1HFY16 results: Net sales: Rs 1375 mn, -13%, EBITDA: Rs. 210 mn, up 2%. EBITDA margin at 15% vs 14% last year, Interest cost at Rs. 6 mn, down 86%. PAT at Rs. 108 mn, up 29%

Accumulate Granules India; target of Rs 174:Emkay

Styrolution ABS - Margin contraction seen as negative surprise

Q2 Sales were higher +5% yoy to Rs 287cr driven mostly by high volume indicating market share gain.

Ebitda, however, declined -4% yoy to Rs 18cr while margin saw 50bps yoy contraction to 6.2% even after inventory gain of 16cr vs gain of 10cr yoy/qoq

Interest cost were lower by -62% yoy to Rs 1cr while tax expense were also lower by 3%

Consequently, PAT grew +13% yoy to Rs 9.3cr

Q2 EPS at Rs 5.28/sh and ttm EPS at Rs 20.53/sh

Gross debt at Rs 118cr (vs Rs 133cr in Mar'15) and NW at Rs 530cr. D/E at 0.22x.

Balrampur Concall – Guided for firm sugar prices, accommodative SAP policy, 5% lower industry-wide output. At Balrampur, Some volumes at Cogen and distillery will get spilled over to next year on a/c of ongoing capex

· Policy measures taken so far:

o Govt provided soft loan of Rs 6000cr to industry to clear cane arrears

o New Ethanol tender for 266cr ltrs is for 10% blending of which 110cr ltrs has been contracted so far (Company has contracted 7cr lts to be supplied between Dec’15-Dec’16 period)

o Govt exempted excise on ethanol produced from new molasses which will add Rs 5/ltr to ethanol realization

o Govt mandates 4mt of sugar exports proportionately across all sugar units (Balrampur’s share would be around 115 lakh quintals)

o As per media, Central Govt to pay cane farmers Rs 5/quintal directly which will reduce cane cost by the same amount for the millers

· Sugar production lower than last year: For next season, management expects 26.5mt vs 28mt output in SS14. Early estimates suggests UP to produce 7.3-7.5mt, Maharashta production will come down from 10.5mt to 8.5mt and Karnataka output will be 4.6mt vs 4.9-5mt last season.

· Cane Prices: For UP SAP, mgmt. indicated that it will get notified over next fortnight (key for next season). Mgmt expects that there will be similar linkages which was there in the last season but it will be more accommodative than what it has provided last year.

· Sugar Prices: On sugar prices, due to global climatic conditions and expected lower sugar output, global sugar prices inched up from 10 cents to 15 cents in recent month. Following the global cues, indian sugar prices also inched up from low of Rs 22.5/kg to Rs 27.5/kg currently. Management is positive on sugar price trend and expects prices to remain firm. However, at current prices, industry making loss of over Rs 3.5-4/kg. On export front also, industry making loss of Rs 4-4.5/kg on raw sugar.

· Key policy announcement made this qtr: One is Rs 6000cr soft loan to industry with 1yr interest subvention, two on export incentive on raw sugar export, three on duty waiver on ethanol – will lead to 12.5% improvement in realization for the company and four on consent to increase ethanol blending, however, these needs huge investment to cater to the OMC demand at 10% blending

· Capex: Company plans to shift its distillery to 100% ethanol focus units. For this, Company plans to spend Rs 200cr over next 2 years towards its distilleries to become zero discharge and complaint to pollution norms. Expansion will be phased out from current 7cr ltrs to 9cr lts by next year and further 10.5cr ltr capacity in FY17 will be available.

· Current Debt at Rs 1050cr (LT Debt Rs 651cr and ST debt of Rs 400cr) vs Rs 1233cr in Q1, D/E at 1x vs 1.18x in Jun’15. Of the LT debt, only Rs 150cr is interest bearing to the tune of 10%, Rs 50cr of 2% and balance is interest free. Against this, Company holds sugar inventory of Rs 736cr. Current cane dues at only Rs 119cr vs Rs 600cr as of last qtr.

· Lowers guidance for distillery and cogen due to ongoing capex: Due to distillery expansion, some volumes of this year will get spilled over to next year during the construction phase at the respective units. So for full year FY16, mgmt. guided power sales will be around 55cr units vs 62cr units they reported in FY15. While distillery sales will be around 70000kl vs 74202kl last year.

Ujaas buys the land, but it is later transferred to the investor. If someone owns 2 MW from the 30 MW park, their land, panels and substation are separately fenced. However, Ujaas still has access to the whole park for O&M. Land forms 2-3% of the total cost of setting up a solar park. Ujaas is not a trader. Any selling (one time) of RECs it undertakes is on behalf of it customers as part of the service package. Ujaas owns some unsold RECs on its own but that is from a 15MW solar park they set up for tax benifit, else all RECs are in names of the investors in the solar parks.

Till recently, for each MW setup, Ujaas would charge ~ 6.5 - 7 cr.(incl. all services mentioned above) of which 1 cr. would be PAT, and further 0.1 cr. annually for O&M with 5% annual increase for 20 years. This is the sole source of revenue.

Thanks Ayush for the comprehensive Q&A. This puts to rest a number of questions that were being raised on the forum.

The MQ sheet combined with the BQ sheet focuses the mind like nothing else that I have seen in my investing life. It is hard work but worth it in the end. A super template created by Valuepikr.

The story of MPS looks compelling with every passing day.

Looking forward to the BQ sheet too  -). You can call me greedy.

-). You can call me greedy.

Best Regards

Disc- Invested

From your reply, is it safe to consider

Nanoinvestor,

Installing Solar Power Plants is the business of Ujaas. However, it differs from Moser Baer:

1.) Moser Baer manufactures solar panels and has some wind farms, whereas so far Ujaas is following an asset light model incurring just opex as opposed to capex.

2.) Ujaas does more than just EPC - procures land, licenses and later helps sell RECs/fulfill PPA, carries O&M. They do this like a MF by buying plot of land and installing say 30 MW - then investors/SMEs can own a small share of this.

You are right in observing that Solar REC is the Indian version of Carbon Credit and that most of the solar modules are procured from China.

Range of Equipment manufactured by Cranex include

1.EOT Cranes (Electric Overhead Travelling Cranes)

2.HOT Cranes (Hydraulic Overhead Travelling Cranes)

3.Goliath Cranes,(A heavy but portable crane, usually about 50-ton capacity, used for jobs requiring heavy lifting and for shop fabrication involving heavy steel)

4.JIB Cranes (A crane having a swinging jib, as opposed to an overhead traveling crane, which does not.A cantilevered boom or horizontal beam with hoist and trolley capable of picking up loads in all or part of a radius around the column to which it is attached )

5.Winches

6.Electric hoists

The products are tailor made suiting specific project needs.The company has a technical collaboration with Kuhezug Fordertechnik GmbH of Germany.