(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Posts in category Value Pickr

Virat Crane Industries Limited (VCIL) – sure shot multibagger (02-11-2015)

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Virat Crane Industries Limited (VCIL) – sure shot multibagger (02-11-2015)

Virat Crane results were declared and they are a bit subdued on the revenue growth front. This could be due to lesser MRP per packet compared to last year. The reduction in milk prices could have been passed to the customer. This also means there could have been not much volume growth.

However, as expected the raw material costs have come down and though the revenue was lower by about 10% YoY the Net Profit grew by 22% YoY.

HALFYEARLY ANALYSIS:

For such a small company, the quarterly earning may not be a right approach as the growth would be lumpy.

If we look at Half Year metrics, the Revenue growth is flat (29 crore vs 28.6 crore) so indeed there is a bit of volume growth (7-10%?) and the net profit (EPS) growth is 61%.

Other expenses are a bit higher which I think could be due to expansion activities in Karnataka (?).

Balance sheet is strong though and finance costs have dropped by a lot when compared to the balance sheet size and the company is practically a zero debt company except for working capital requirements.

Virat Crane Industries Limited (VCIL) – sure shot multibagger (02-11-2015)

Virat Crane results were declared and they are a bit subdued on the revenue growth front. This could be due to lesser MRP per packet compared to last year. The reduction in milk prices could have been passed to the customer. This also means there could have been not much volume growth.

However, as expected the raw material costs have come down and though the revenue was lower by about 10% YoY the Net Profit grew by 22% YoY.

HALFYEARLY ANALYSIS:

For such a small company, the quarterly earning may not be a right approach as the growth would be lumpy.

If we look at Half Year metrics, the Revenue growth is flat (29 crore vs 28.6 crore) so indeed there is a bit of volume growth (7-10%?) and the net profit (EPS) growth is 61%.

Other expenses are a bit higher which I think could be due to expansion activities in Karnataka (?).

Balance sheet is strong though and finance costs have dropped by a lot when compared to the balance sheet size and the company is practically a zero debt company except for working capital requirements.

Shalibhadra Finance – Steady Growth NBFC (02-11-2015)

Do you buy the statement that results have been sent to BSE but not uploaded? BSE is not so lax, it uploads results at best by early next working day if they have been sent at the end of the day.

Cupid Ltd – Helping the world play safe! (02-11-2015)

Thanks @nityanandparab. I agree with you. I do not see 10x returns from this stock especially because of the consumers they cater to. As far as my understanding goes, their main clients are NGOs and other Government organizations which is risky and difficult to verify. How prevalent are they in the retail market? I saw they sell on Amazon and Flipkart but they do not focus much on the domestic market which they claim is the largest market. Why have they not been advertising their brand? I think they can position this product very well in the domestic market by advertising. For eg. Emami positioned fair and handsome perfectly and took away the market. I am sure there is not much difference between Fair and Lovely and Fair and Handsome. They just advertised brilliantly. I dont see any advertisements for female condoms and I believe the company that starts advertising first will occupy the consumers mindshare.

Honestly, 3-4x over a period of 4 years is good enough return for me. But I believe, that there can be a lot more potential for growth. I will arrange a meeting with the management and would like to understand his thoughts.

Sarla Performance Fibres – Another Interesting Textile Story in Making? (02-11-2015)

Concall details not yet uploaded.

Tanla Solutions – a niche player in m-commerce space and a turn around story? (02-11-2015)

Introduction:

Tanla Solutions founded in the year 1999, a Hyderabad based Indian company is a leading provider of telecom solutions to Mobile Operators, Hand set Manufacturers, Content aggregators, ISVs and Media companies globally. With over 100 customers in 32 countries, Tanla provides solutions in the areas of Voice, Video, Messaging, Application/ Content Licensing and Mobile Payments and is the first company to launch 3G VAS services in India.

Tanla's Mobile Payment Gateway is connected with more than 100 mobile operators and processes mobile payments in over 160 countries through operator, credit/ debit card billing. Leading content aggregators, ISVs and hand set manufacturers including Nokia use Tanla mobile payment gateway to market their applications/ content globally. Its License Manager product is embedded in more than 300 million Nokia handsets globally. Located in 9 countries, Tanla employees more than 300 telecom professionals

Key Numbers

Market Cap.: ₹ 320.23 Cr.

Current Price: ₹ 32.90

Book Value: ₹ 61.91

Stock P/E: 22.01

Highlights of Q2 FY16

- International A2P messaging hub is operational from Oct 2015. 2 large international clients have been boarded in Q2 and they have started commercial traffic in October 2015, which will ramp up over the coming quarters.

- Delay in commercial launch of the Singapore hub was a result of implementing the changed regulations for International messaging outlined by TRAI.

- Domestic - Total volume processed in Q2FY16 is 11.75 billion messages as compared to 11.64 billion messages in Q1FY16, an increase of 156% over Q2 FY15 and 1% over Q1 FY16.

- India A2P messaging hub recognized as the preferred platform for delivering mission critical transactional messages like OTP’s, transaction, delivery and security alerts due to its industry leading processing times.

- M-Payments - 45.4 Mn transactions were processed during Q2 FY2016 compared to 47 Mn Transactions in Q1 FY2016.

Turn around story

In FY14, the management decided to move away from a high capex and long gestation businesses to a more B2C transactional one. They decided to derisk from lumpy concentrated revenue sources to a more diversified and margin enhancing clientele. The renewed focus started paying off and company partnered some major telecom players like Vodafone to provide messaging services. Tanla currently has a 60% market share in A2P messaging.

Disclosure – Not invested

Cupid Ltd – Helping the world play safe! (02-11-2015)

@sagararya At this time i donot see any buying opportunity for multibagger returns atleast 10X in this stock.

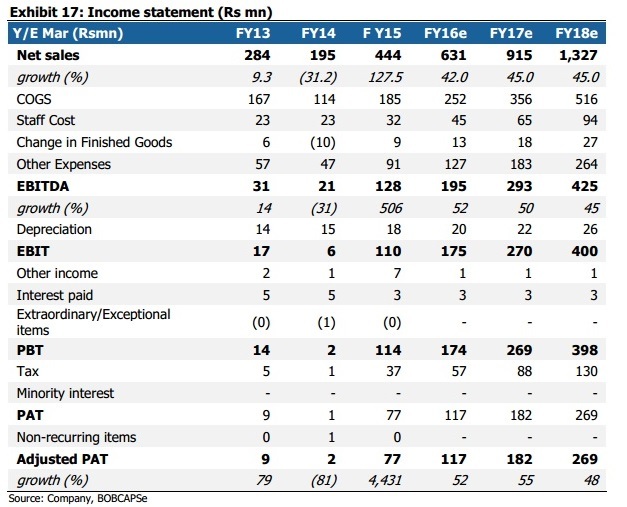

1. If you see the BoB report on Cupid(Attached screenshot), It says it will have around 26 cr profit(Esti). So you can derive the chart of future projection of profit. As per my view the sales are going to get stagnant after 3-4 years.

2 . The management is saying they will issue dividend every quarter that means the company is not going to invest in further expansion

3. It is Global tender business so the future orders depend on winning the tenders, Cupid has stronghold in South Africa vs the competitor has in South America(Brazil). Again they may be having territory restriction if you see the news for winning bids in last few years.

4. Considering the PE multiple of 30 at that time also, we an get the MCAP of 1000cr and share price at around 1000 . If the company is not able to deliver good number of sales then the share price may also get stagnant.

5. You can see the story and stock movement of its closest competitor which is in US. The share price got halved when they announced stopping of dividend payment every quarter

Disc: Not invested. My view may be biased for not to buy the stock at current price. I reserve the right to be wrong.

Idfc amc-change of guard (02-11-2015)

Is idfc amc good anymore whith kenneth leaving? Is the new manager equally able?