Check this out -

This interview happened in August which falls in second quarter. The MD mentions that they had taken up the repairs during the quarter. But they may have managed around it, so that the stoppages didn't affect a lot.

Check this out -

This interview happened in August which falls in second quarter. The MD mentions that they had taken up the repairs during the quarter. But they may have managed around it, so that the stoppages didn't affect a lot.

While EVA is the right way to measure things, it is really not as path breaking as it is made out to be.

EVA is better than EV/EBITDA or P/E or P/S or P/BV to value companies.

But it is just DCF in a new bottle. To be specific DCF after removing Opportunity cost in a new bottle.

Cupid results were music to my ears after a rather subdued results from my other holdings:

Salient points:

On H1 EPS of 6.41 (FULL year FY 15 EPS is 6.93),

I predict, H2 FY16 to be better than H1 and full year EPS could be around 16-18. I think the full quarterly effect of the new large order may not have been reflected in this quarter but over the year the revenue growth will further catch up.

Quantitative and Qualitative points have both improved and the story could be on the way becoming a secular one.

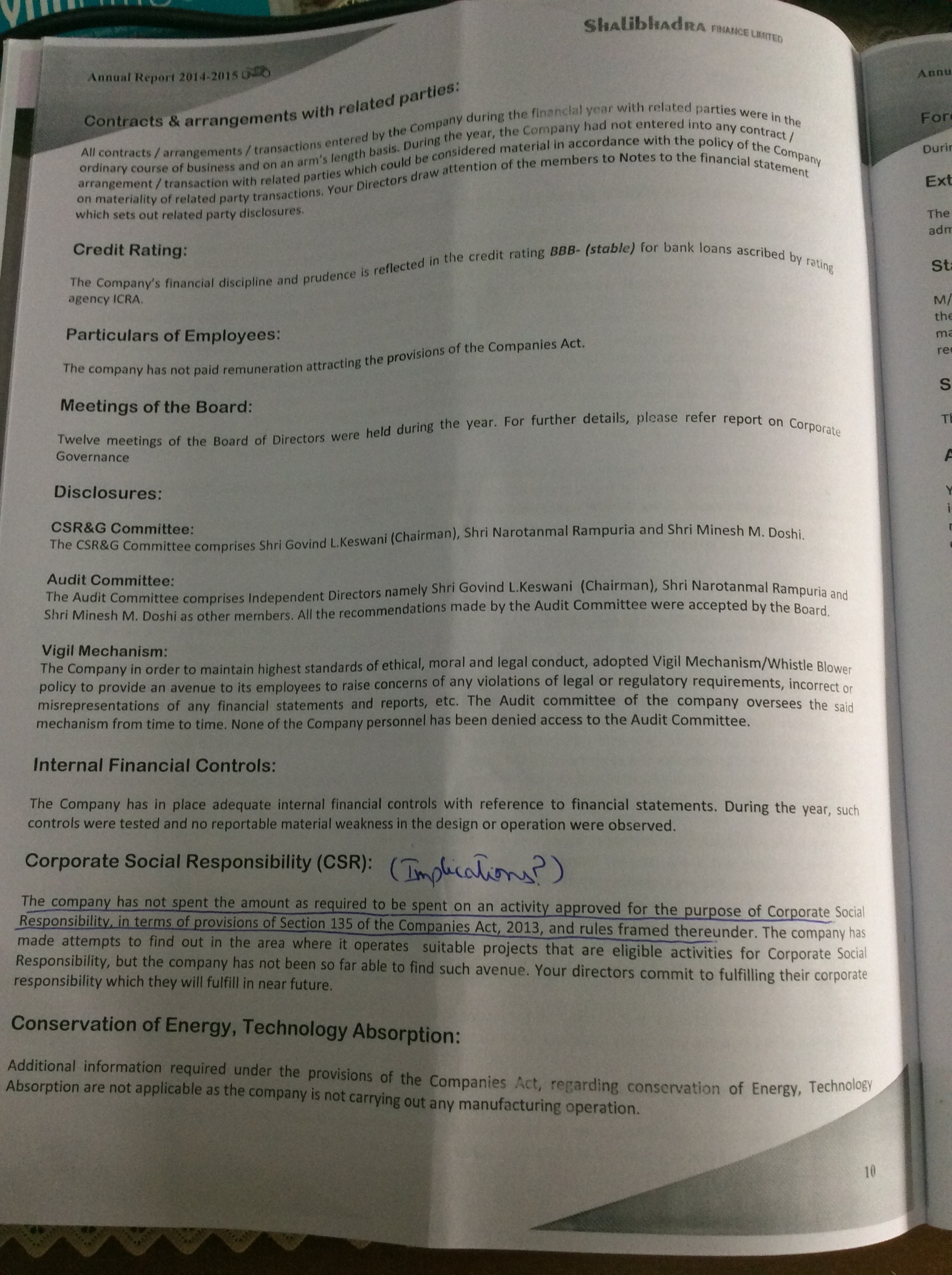

As mentioned earlier, I spoke with Minesh Doshi (MD) on Wednesday to inquire about the annual report and dividend payment.

He said that they don't have any soft copies of the report and the BSE needs to scan each page and upload it on their site which is why it's not been uploaded on their site yet. I have received a physical copy of the AR yesterday and I'm sharing the relevant sections here.

Regarding dividend payment - He mentioned that this is the first time they are doing an electronic transfer (ECS) of the dividends which is taking time. (Although he sounded apologetic of the same but this is no excuse and I'm not sure whether they're liable to pay interest as of this day)

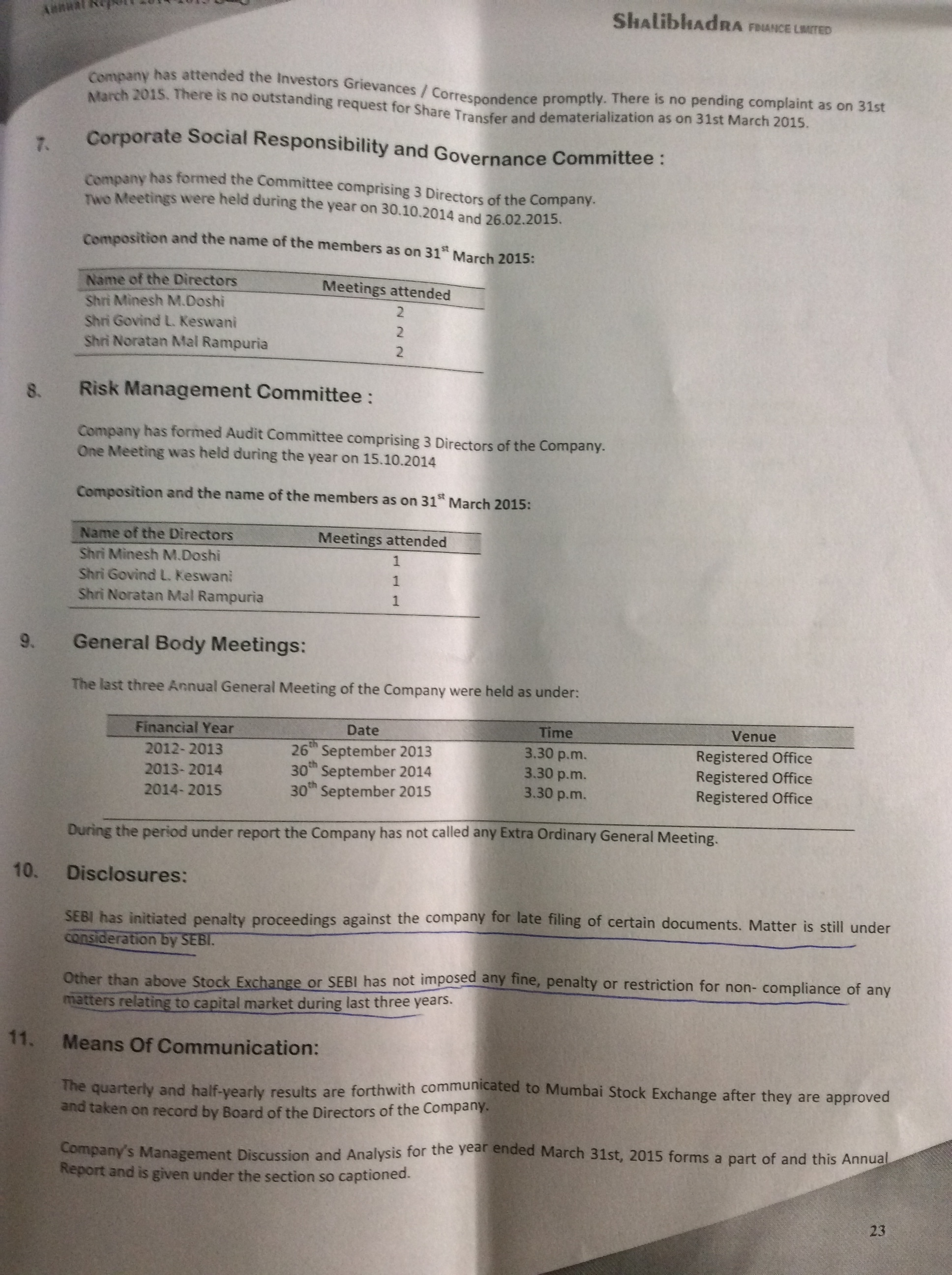

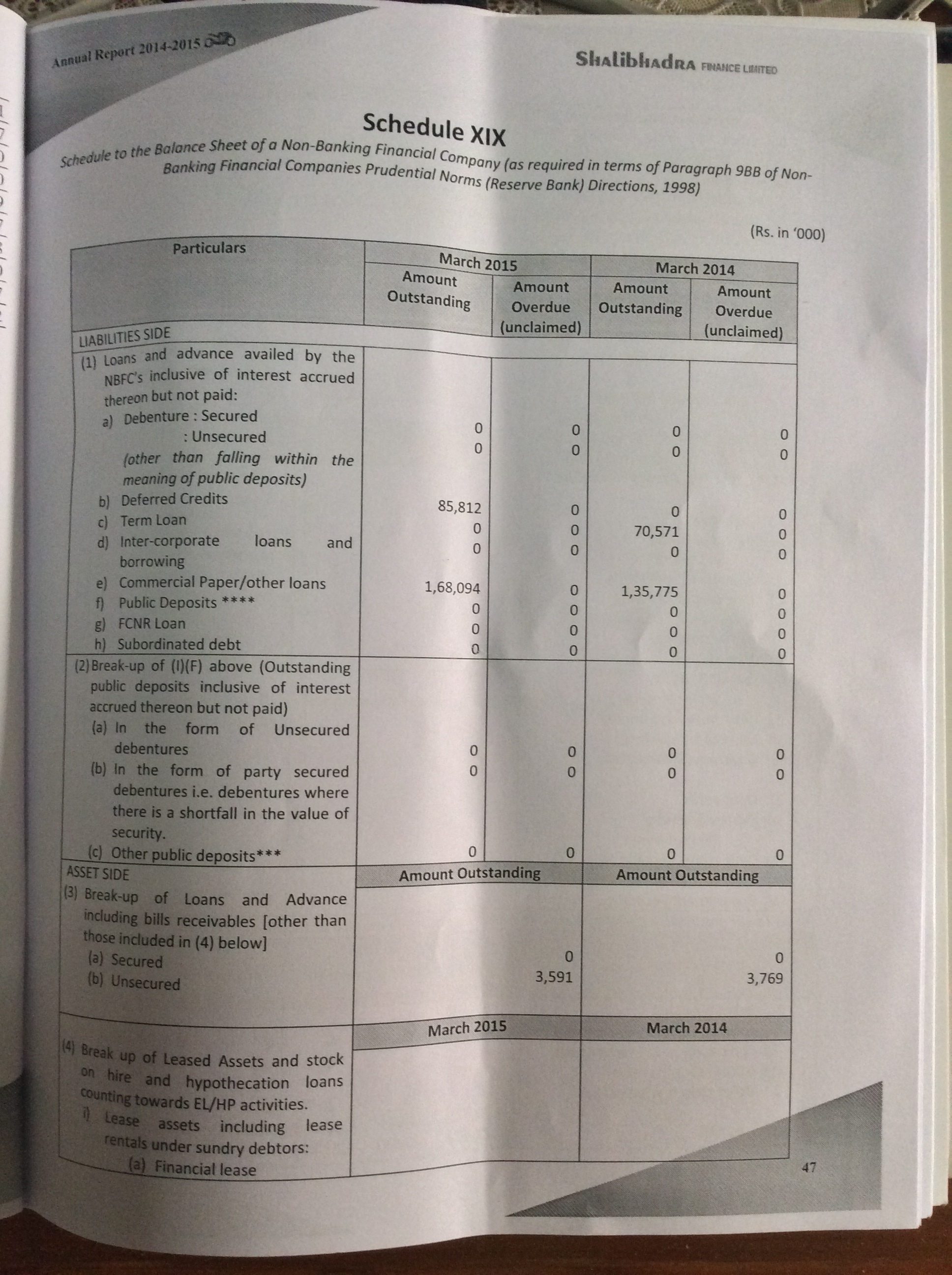

Certain highlights of the annual report :-

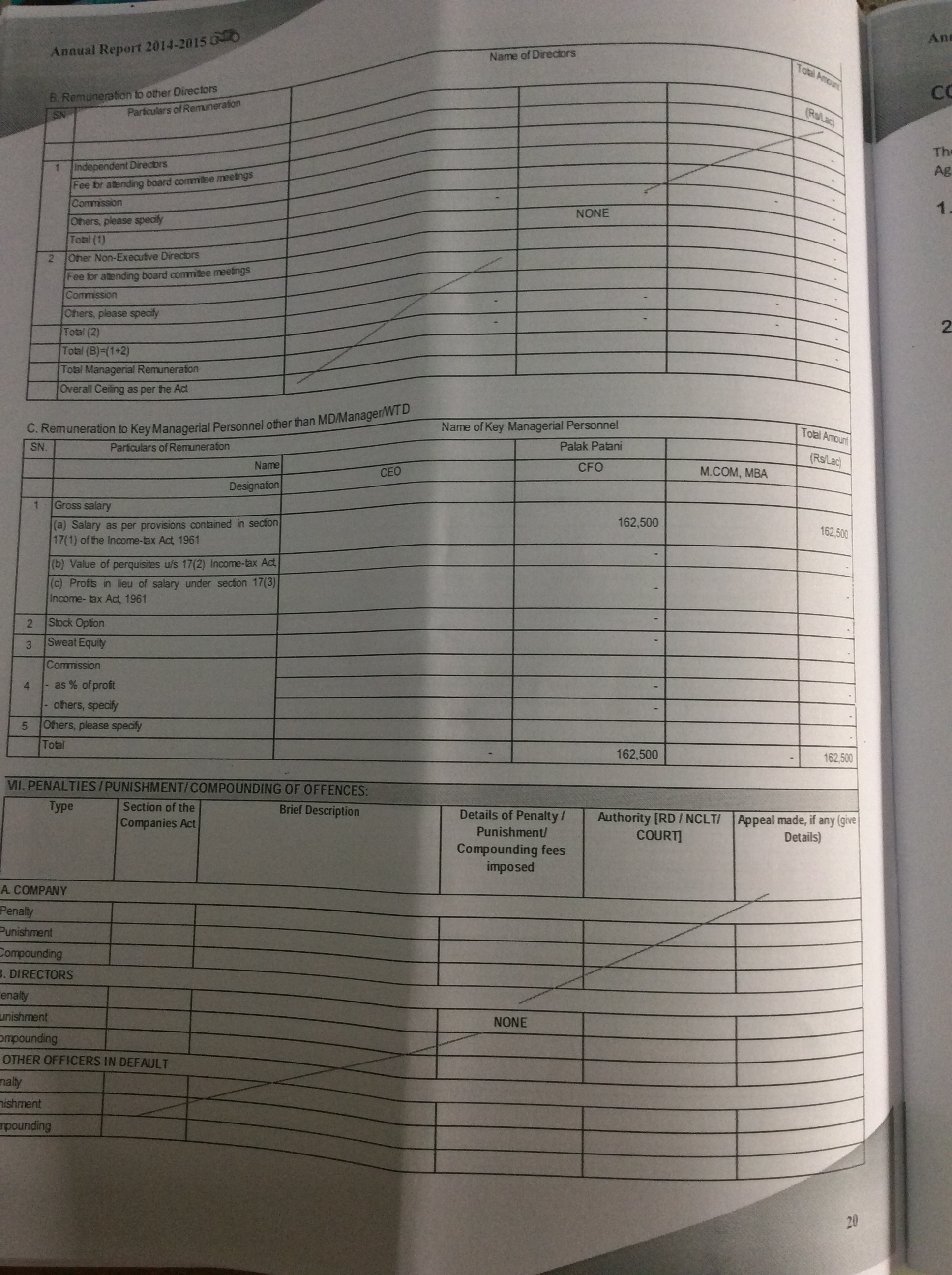

1. 15% growth in live contracts

2. 0% remuneration to directors (this is really surprising for me. Are they already too rich and this business doesn't matter to them or do they have another business running in parallel? They definitely can't sustain themselves on dividends - amounting to 30 odd lakh for 20+ family members.

3. They haven't done any CSR activity in the FY based on their profit. Would be great if someone can share the implications of that?

4. SEBI has initiated penalty proceedings against late filing of certain documents. This is under investigation - how serious is this?

Disc - Invested

One of the positive factors in recent time is increasing gap between cotton prices and polyester prices. Though cotton prices fell but fall in polyester prices was more steep as it is crude derivative. Polyester is raw material for Sarla. Yes Gaurav, you rightly pointed out about crude tailwind benefits to Sarla. But historically (last 10 years), Sarla has enjoyed 45%+ gross margin, management is of the view they sell value added products which gives them these high margins. In addition, USA plant is also adding to margins as it is stabilizing.

But yes, will surely take your point on concall about volume and realization growth. Thanks

Yes true...Also if even it gets the accord - I read some lines in the article where the whole scheme developed is I think to compete with the Chinese low cost products. Keeping this in mind and our relations with the US and other countries in the world (thanks to Mr. Modi) - It will be easy for India to be a part of this TPP. Assuming we are a part of the TPP and China is not - we as well as Gimell (singapore) will have an advantage over China's Wingloo...

This is all long term - 2-4 years...But this can be great for Kitex.

A very good realistic interview post IPO closing.

You are going to have to deliver quarter on quarter because you are going to be a listed entity. Let me talk to you about specifics. If you can take us through the kind of applications that you have got as far as the QIB portion is concerned. Can you take us through the number of applicants that actually came in, in the QIB category?

A: I know that the anchor book had more than 40 investors. QIB of course saw a huge amount of response as you said, close to 20 times subscribed. More than just the numbers what we feel is sense of pride and the kind of investors who have now come in either after a long period of time into India or for the very first time in an IPO in India. So, it is just the quality of people and these are some of the biggest players, some of the most sophisticated investors from around the world who have seen a lot of companies around the world and some in India as well. That is what kind of makes us feel good with what we have been able to do and once again a lot of trust in us now, lot of faith in us now, we have got to kind of be able to deliver on that faith and trust.

Possibly because many of these people actually have holdings in some of the very best airlines around the world, some of the most profitable airlines around the world. They have had holdings there for a long period of time.

India is a complex story. The airline business in India has been very different from what you see in many other parts of the world. In that for someone to really appreciate what IndiGo is doing, how IndiGo is just so structurally different from anybody else. However as we become a listed company, as people start watching us more carefully, as people start seeing us on delivering on some of the things that we have been saying in the roadshows, I think the understanding for the airline business and more importantly how IndiGo is just so very unique and different from everybody else is something that will grow in on the Indian investor as well.

What kind of demand environment are you expecting. We are at the start of the festive season now. In the short term, medium term and in the long term all kinds of estimates have been put out by IATA, CAPA, so on and so forth about what the long term promise looks like. But let me start by asking you about the short term demand environment, the medium term and then talk about the long term prospects.

A: We expect it to be in the kind of late teens. So, 18-20 percent year-on-year (Y-o-Y) for the next few quarters just as it has been in the past. Going up to 9.5 percent Compound Annual Growth Rate (CAGR) over the next 20 years but what I am saying is not rocket science. You look at India, look at the size of India, look at how underpenetrated the aircraft market is. A country of 1.3 billion people, less than 400 commercial airplanes in this country. So, there is going to be huge amount of demand. It is for people like us to be able to take advantage of that opportunity, execute to that perfection and add more and more airplanes, more and more capacity so that more people can fly and hopefully if cost structures start coming down even further then the propensity of travel increases even more and then the growth takes an even bigger kicker.

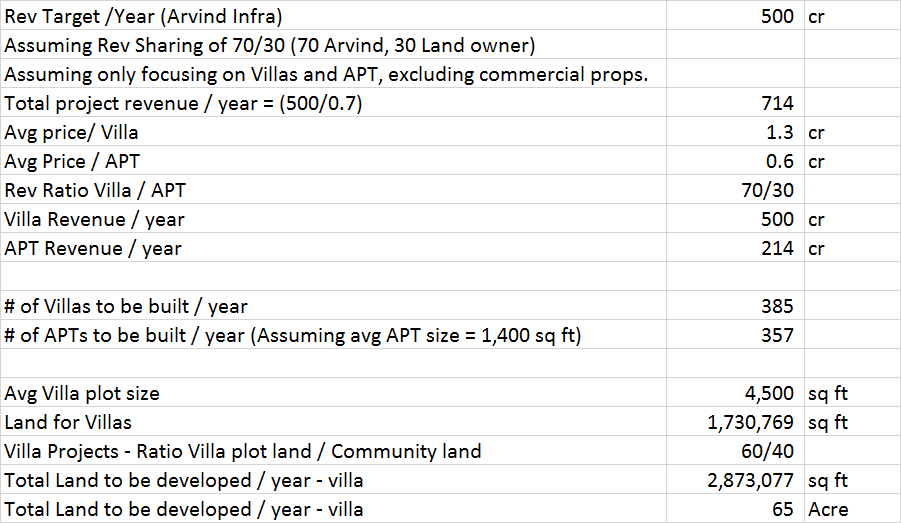

Hi Vinay, thanks for filling us in on the beyond 5 project. I think the revenue forecasts of management seem to be pretty reasonable based on the discussions in this thread, there is a significant probability that they will meet their top line numbers, concerns mainly may be on the bottom line though, potential cost overruns, project delays due to regulatory delays etc.

I think the more important question is, can they at the least maintain this revenue trajectory, i.e. Do an average of 500 crores worth of sales/ year consistently (if not grow that further) ? So the key is can they find enough worthwhile projects in the coming years to sustain this 500cr/ year revenue, especially given the fact that so far they have chosen to restrict themselves to just 2 geographies, BLR & Ahemdabad. Clearly they may venture into other markets, but then, in those markets they don't have any brand recognition, so would land owners be willing for JV's in those other cities in the same way they are in Ahemdabad?

Let's try and see how much of development work they need to do each year.

Clearly we can debate on the assumptions above in terms of avg size / villa or price/villa etc, and we may arrive at slightly different total development numbers. In any case the key questions are as following

The key point is project pipeline (apart from those already announced) I haven't seen them add any new projects for a while, do deals for more JV's etc.

Does anyone happen to know about the "New Haven" upcoming project? how big, where etc? And not too sure what to think of their megapark project, would small businesses be willing to shell out so much money for a fancy workshop / industrial shed?

Disc: significantly invested at cmp

Omg rks. That was an awesome reply . I am indeed thanks to you. I did not expect a reply so early. I have collected some material on EVA and would love to share it here with you. With your efforts and if other join in we can make this EVA thread a great place to learn.

Yes , I too have read the arguments in favour of EVA and they are pretty impressive . we need to calculate EVA of Indian companies correctly . would you like to take the initiative. I will give whatever limited knowledge I have abt EVA.

Also thanks abt the miller approach . I am curently reading earnings power box and EVA