Consolidated Q2 2016 results:

Top line growth: 39%

Bottom line growth: 187%

India: Flat (Due to discontinuation of certain promotional schemes and hygiene initiatives)

US: 326%

Brazil: -18% (+19% on constant currency basis)

Consolidated Q2 2016 results:

Top line growth: 39%

Bottom line growth: 187%

India: Flat (Due to discontinuation of certain promotional schemes and hygiene initiatives)

US: 326%

Brazil: -18% (+19% on constant currency basis)

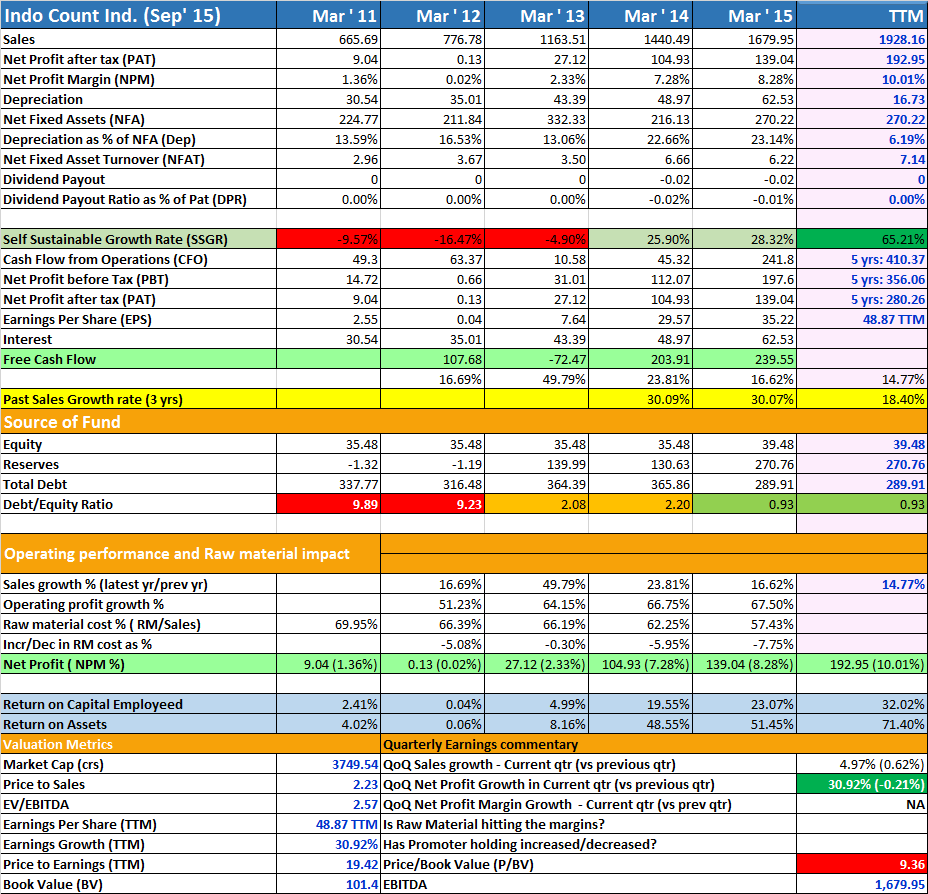

Good company with good growth rates. Good Self Sustainable Growth Rate. Debt reduced. Fantastic RoA and impressive RoCE.Valuation wise also at 2.23 levels is not horribly high. 9 times BV.

For Self Sustainable Growth Rate, pls read: http://www.drvijaymalik.com/2015/06/self-sustainable-growth-rate-measure-of.html

Note: FCF and EV values may be wrong as I have done it as per my understanding.

Promoters are above average on all three fronts of integrity,passion and competence,which one should look when evaluating a company or promoters. Retail side is going more towards mfs or pms in place of direct equity.Opportunity is big as this trend has just started.I am equally bullish.

Return ranking of sugar stocks in last 1 month:

(1) Dalmia Bharat Sugar - 191 %

(2) Dwarikesh Sugar - 175%

(3) Dhampur Sugar - 81%

(4) Triveni - 68%

(5) Rajshree sugar - 59%

Some other sugar stocks return : Sakthi sugar (58%), Balrampur (38%), Oudh sugar (36%). So generally UP based sugar stocks with lighter balance sheet and smaller MCAP seem to be outperforming. Still 3-4 times return in next 2 years cannot be rules out from these levels if things play out as expected. Govt is also talking about some rational sugarcane policy in next 1-2 months which augur well in near term. Proposed conditions imposed by govt can weed out marginal and weaker players from the sector.

Read here about my concerns about RM supply and possibility that Ambika is already using 5-7% of global supply of PIMA + GAZA. http://forum.valuepickr.com/t/ambika-cotton-mills/865/291?u=anil1820

To get clarification on the same I attended AGM. Would not post on the details of AGM as someone has already posted the same. Few highlights

1. MD said he is not aware of the market size or past historical growth of market.

2. Ambika is using 5% of Pima plus Giza global production.

3. No more spindles expansion.There is a very high possibility that overall market for Ambika niche cotton is not very large and is not growing. So its unreasonable to expect them to grow volumes at 15% CAGR for next five years. I was under impression that Ambika holds less than 1-2% of market share and can grow comfortably at 15% CAGR Whatever growth will happen post 30K spindles expansion will be driven by forward integration. Promoter is a capable man and am not doubting that forward integration will be any problem. But my understanding that current business could grow at 15% or higher volumes for next 5-7 years was wrong.

I don't think he is being too conservative is saying that no more spindles expansion. With already 5-7% of global supply which might increase further with current expansion, spindles expansion may no longer be feasible.

I have 3 observations

1. There has to be other competitor in India which is exporting engineering quartz because number do not match up. (Asian Granito also makes quartz as I read in their investor's presentation).

2. Their Apparel business remains a drag with 4 cr loss in this quarter. (may be promoter is siphoning money off from there).

3. Finance costs has increased from previous quarter with more or less same structure. I think last time also management were charging the interest which they were supposed to, so why there is an increase in Finance Cost?

Would be glad if you can throw any light on this.

Disc. Had increased my holding to 15% of my portfolio from 5% after looking at the stone update data. Considering to reduce the allocation because my assumptions (like monopoly in engineered quartz, etc) appears to be wrong after watching today's results

The company does not make cash flow from operations

Q2 Results out :

Sales up 25% , EBiTDA up 44% , PAT up 49%. EBITDA & PAT margin at 22% & 11%.

H1 comparison:

Sales up 39%, EBITDA up 49% , PAT up 56%

Considering the fact that ByKe suraj plaza became operational only in September, Q3 & Q4 numbers should be even better .

Bykes online travel portal is in beta stage, while it looks good it remains to be seen how far & deep would Byke go in promoting the portal once its launched.

You may find this useful - A company should be known by the company it keeps, I had written it as a guest post a few months ago.

Warm regards,

everything is alright.

actually capacity utilisation is 60% which will increase with time.

the stock is down because of monsoons are not good.

kaveri seeds is available at a pe of 10.

excel crop at 14 X so all agri stocks are down sentimentally but are sound bets fundamentally.

also there is a pest attack in the north so september results are expected to be good.