Brilliant results for Q2. Stock was up 20%...still has a lot of steam left.

Posts in category Value Pickr

Bloom Dekor- A plywood and lamination microcap (18-10-2015)

http://valueinvstr.blogspot.in/2015/10/indian-plywood-industry-value-migration.html is the original article, plz. check

Bloom Dekor- A plywood and lamination microcap (18-10-2015)

Indian Plywood Industry - Value Migration On The Way

The

Indian Plywood industries is at the cusp of a new era. Over the last

few years, the organised players (Century Ply, Green Ply, Kitply etc)

have been growing at double the rate of the overall industry. This

signifies that there is value migration happening from the unorganised

unbranded products to the organised branded ones. The overall organised

sector is growing 20-25% CAGR. Organised sector is 30% of the overall

plywood sector.

The overall plywood

industry size is Rs. 180 billion (source: Greenply AR 2015). The MDF

industry size is Rs. 13 billion growing at 15-20% over the last 5 years.

MDF

is engineered wood made from wood (fibres), glued together using heat,

resin and pressure. It is also a superior substitute for cheap

unorganised plywood. It faces competition from imports. Demand in

this sector is driven by ready-made modular furniture, modular kitchen,

ready-to-move into offices/retail outlets, a need to substitute low

quality plywood, affordability, increasing awareness of customers of

better alternatives and shortage of time.

The

Indian govt has imposed a ban on new licenses for manufacturing due to

the environmental impact. This will help the existing majors.

Growth Levers

GST & its impact

• Remove inter-state tax anomalies

• Remove differential with unorganized sector hence a value migration from unorganized to organized players

Other growth levers

• Home renovation cycle is declining

• India's per capita income rising along with disposable income

• Rising urbanisation and aspiration levels amongst people

• Govt focus on "Housing for All" -- Rs 22,407 crores allocated by

FinMin for 2015 to create 6 cr (2 cr urban + 4 cr rural) complete houses

by 2022

• Government Announcement regarding construction of 100 smart cities

• Focus by HFCs on Tier-2, Tier-3 locationsOver

the short term (< 1 year), the industry may have moderate growth

owing to the subdued demand in real estate sector. However, the growth

levers are likely to kick in over the medium term (2-3 years). The

industry looks to have bright prospects over the long term (10 years).

It would be interesting to keep a watch on Century, Green and any new

player in this space.

Bloom Dekor- A plywood and lamination microcap (18-10-2015)

Bennet & Coleman has stake in a lot of cos where they take stake in lieu of advertising and what is called "paid news " . Can anyone point out if they indeed paid cash for their stake .

Virat Crane Industries Limited (VCIL) – sure shot multibagger (18-10-2015)

Virat Crane hit the ceiling price of Rs. 63.70 on BSE. Up 30% for the month. I understand under new rules it will not be allowed to go higher during the current month. Perhaps a good time to accumulate gradually. There is a strong buzz that the Co.'s performance in the current year is improving & an interim dividend is a possibility.

Bajaj Finance Limited (18-10-2015)

Bajaj finance god a nod to set up a housing finance Company as a wholly owned subsidairy

Bloom Dekor- A plywood and lamination microcap (18-10-2015)

I invite @Donald @ayushmit @MoneyWorks4ME @vml @pratyushmittal and others in making the case easy for me and others to understand in this business

Bloom Dekor- A plywood and lamination microcap (18-10-2015)

http://www.bloomdekor.com/products/ is the website of the company. With that out of the way, Lets look at the ratios and take some confidence before I introduce you to the nature of the business.

Market Cap.:

₹ 19.83 Cr.

Book Value:

₹ 25.40

Stock P/E:

8.16

Dividend Yield:

2.07%

Face Value:

₹ 10.00

Enterprise Value:

₹ 48.20

EPS:

₹ 3.55

Graham Number:

₹ 45.04

EBIT:

₹ 6.63 Cr.

EVEBITDA:

5.09

PEG Ratio:

-1.23

Debt to equity:

1.81

OPM:

15.22%

Return on equity:

4.25%

Return on assets:

8.07%

Average return on equity 5Years:

0.37%

Dividend Payout Ratio:

59.42%

Exports percentage Now:

0.00%- It used to export earlier

Exports percentage 5Years back:

21.58%

Promoter holding:

52.02%

Piotroski score:

7.00

Altman Z Score:

1.86

Profit growth 5Years:

-6.62%

Profit growth:

248.17%

YOY Quarterly profit growth:

176.36%

CROIC:

14.13%

OPM 5Year:

8.58%

Sales growth 3Years:

5.40%

Operating cash flow 5years:

₹ 27.45 Cr.

Average return on capital employed 10Years:

7.11%

Average return on capital employed 3Years:

8.59%

Return on invested capital:

12.03%

Investing cash flow 10years:

₹ -24.79 Cr.

Cash from operations last year:

₹ 3.95 Cr.

Inventory:

₹ 32.34 Cr.

Days Inventory Outstanding:

193.58

Profit growth 3Years:

6.37%

Market Cap to Sales(Kenneth Adrande metric):smile:

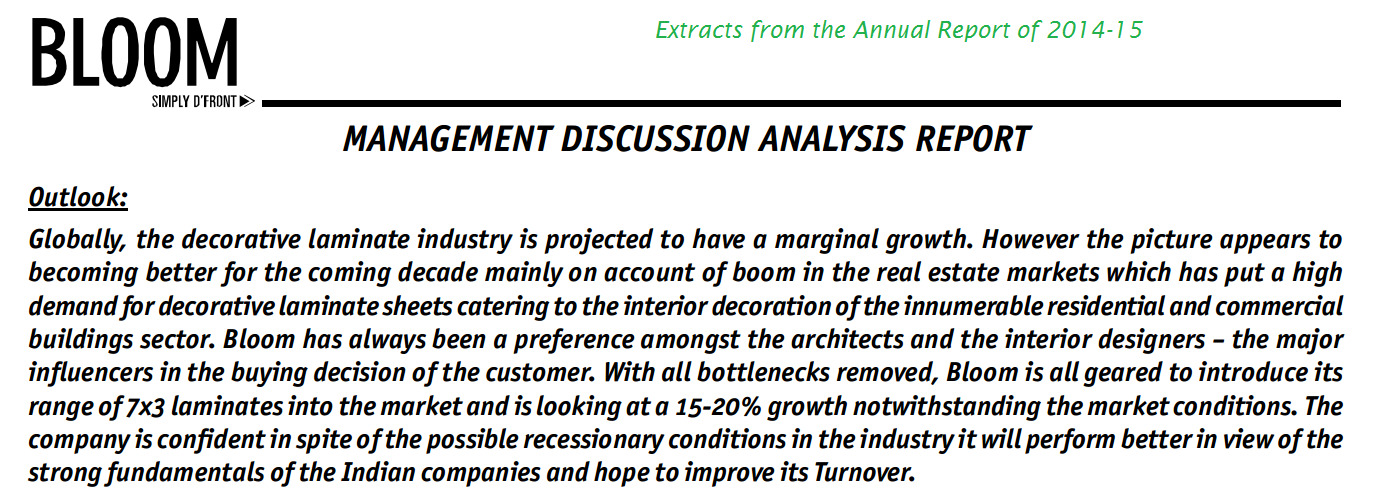

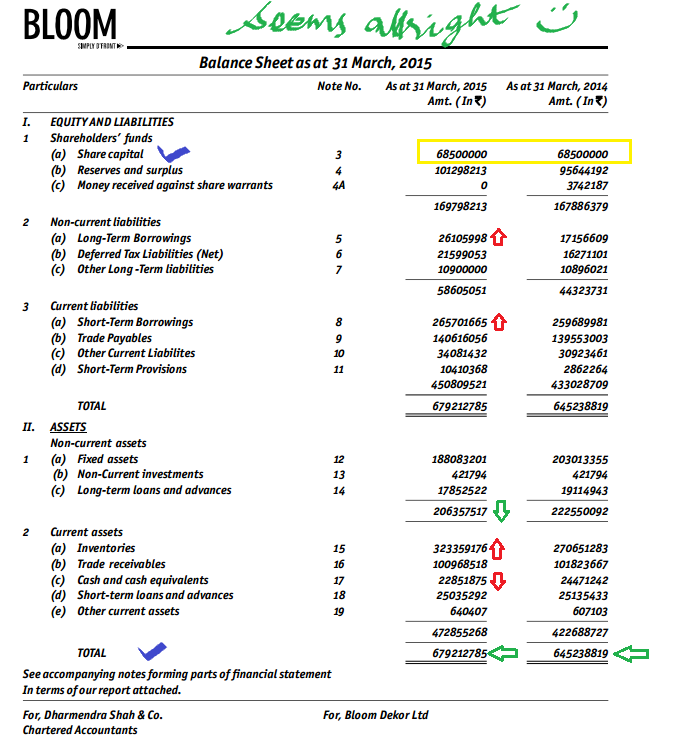

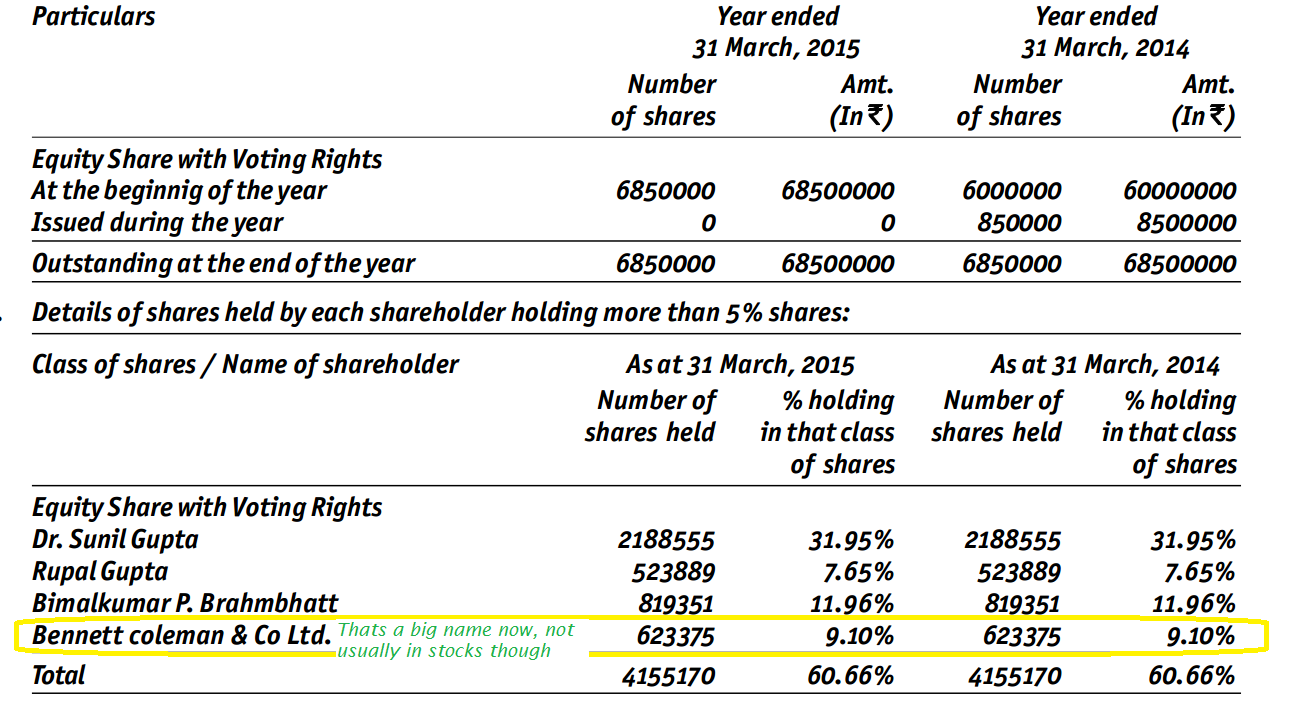

0.32Now the funny thing is Times of India has a holding in this company. It has been doing well for itself as the above ratios state and most of all its a small company, so small that price action can make it hit either circuit filters on Index. Its known to a few as a door making and a designer company. It is involved in e-commerce and selling advise online. Its brands are Bloom and Olive. They are a company from Gujarat and have a solitary plant where they make the products from wood and its wastes. It has branches in all major metros.

On the plant, this is what they say:

A long awaited continuation of the prelude, a brand new collection with the same values.

Elegant and contemporary, yet reminiscent of the classic. Authentic

wood-grains offer immense warmth and satisfaction. Interiors of today

demand a fresh look, where one’s eye is always in search of the

not-so-seen.

URBAWUD collection intends to address this need, to assist designers

create contemporary interiors for the existing urban lifestyle and

tastes.

Bloom Dekor is proud to present this special range of Laminates that

also include improvised colour tones of authentic wood-grains.

Address:

Bloom Dekor Limited

2/F, Sumel, S.G. Highway, Thaltej,

Ahmedabad – 380 059,

Gujarat (India)

Big news is that, it pays dividend and quiet frequently. Its also growing its OPM very consistently and generates cash flows.5262250315.pdf (2.7 MB) Take a good look at this awesome looking design of Annual Report and pass comments on the quality of it. What Bennet and Coleman knows that we dnot know, lets find out?

Payment Banking – Disrupting Banking (18-10-2015)

I have always been bullish on the Indian financial sector. My logic is simple. Any industry where there is a very large disconnect between demand and supply is bound to do well. India is a cash / credit starved nation and any business which provides credit to people and businesses will do well over a very very long time.

The history of Indian banking is very interesting. Refer to Banking in India on wikipedia for a good overview. By now, most people are used to the ubiquitous ATM machines and do not consider private banks as fly-by-night operators who will take their money and run away. We are at the cusp of the third major wave in Indian banking (nationalisation in the 70s and privatisation in the 90s being the first two). With the 11 new licenses given out by RBI for new payment banks, the playing field has been (once again) forever changed. Ten years down the line, banking will not be the same as today. Brace yourself for a huge disruption in the coming years.

So what are payment banks? For simplicity's sake, it is a "technology driven bank", mainly mobile based which will cover most of the services provided by a regular bank except giving loans. They can take deposits of upto Rs 1 Lakh and pay interest on it, provide debit cards, transfer money from one account to another.

The 11 players who have got the licenses include some very very prominent names - Airtel, Vodafone, Aditya Birla Nuvo, Reliance, Mahindra, India Post, Dilip Sanghvi (promoter of Sun Pharma), Paytm, Cholamandalam and NSDL. All of them are big players in their own fields. Three of them stand out distinctly - India Post, Airtel and Vodafone. Their reach and penetration is really unmatched. Just as an example, Vodafone m-pesa accounts for more than 50% of the GDP of Kenya on its platform.

Already, we are seeing a beginning of "Uber"isation of services. Players like Vodafone & Airtel who are already there with you. It is so much more convenient if you can just use the mobile to pay for your kirana purchases or on public transport or at petrol pumps.

Where does that leave the existing banks? The existing large players will push strongly on their apps (HDFC, ICICI, SBI etc). The brunt of the disruption in my opinion will be borne by the mid sized PSU banks and the smaller private banks. We already saw a DCB Bank being routed on the bourses because they accepted the increased competition from these new players. There will be more to come. The age of easy-CASA money may be behind us. The mid sized banks would now have to tie-up with some of these payment banks or invest heavily in their own app infrastructure.

Let us keep an eye out for the trio - Airtel, Vodafone and India Post for the next leg of banking disruption.