Rechecked the report. Mistake on my side. Apologies. Will edit the message.

Regards,

Ramakanth

Rechecked the report. Mistake on my side. Apologies. Will edit the message.

Regards,

Ramakanth

This is not accurate. Please check.

Their Q1 capacity utilization was ~60%. For the whole FY16, NCL expects(in Company MD's own words) a capacity utilization of 75%.

Thanks,

Ravi S

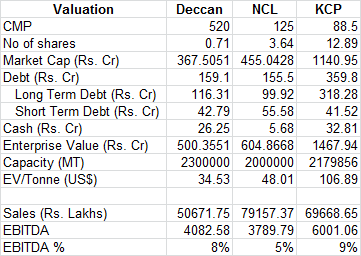

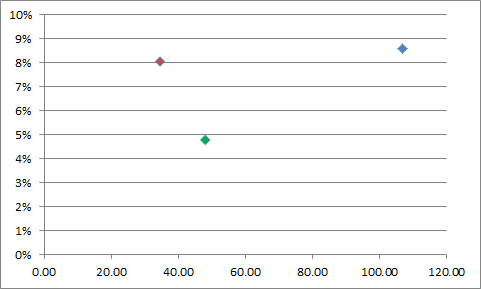

Hi,

The EBITDA margin vs EV/Tonne graph for three companies shows NCL to be at higher valuation for its EBITDA margin.

The above numbers are from their FY15 AR.

Red - Deccan; Green - NCL; Blue - KCP; Y axis- EBITDA margin %; X Axis - EV/ Tonne (US$/Tonne)

Crane is sure a household name in AP & TG.

Durga Ghee, Heard of it but not sure, at least I have not seen it occupuying a shelf space of dairy at any super stores.

When I was small I don't know what betel is, we just know crane pouch packs are used along with betel leaves.

Promoters are looking to be in a hurry to add more verticals non relative businesses which is not good.

Are they talking of unlocking the real estate value they sit on ?

Anyhow it is a common misunderstanding that Guntur is gonna be capital. to be precise the area selected for capital falls in Guntur and is near to Vijayawada city than Guntur.

Do not generalise the place Guntur, it is too big a geographical area. Chirala, Bapatla, Tenali, Sattenapalli, Macharla, Dachepalli, Narasaraopet, Vinukonda, Mangalagiri all are in Guntur and real estate value differs by leaps. One end a acer may not cost more than 2 lac and one end u might not get one fot 50 lac, I am talking of pure agri lands.

Anyhow are the management looking at unlocking land bank value ?

I am trying to do a basic check on all the stocks I own. Please correct me if I have missed any basic parameters.

Company: Cyient

Pros:

Zero Debt

5 Yr sales growth: 23.48%

Profit growth: 15.56%

ROE: 17.83%

Current price < Intrinsic value

Net cash flow: 192.52

Consistent dividends. Last year: 25.43%

Cons:

Low promoter holding.

Being a Mid cap, ROE is comparatively less(10 year ROE for TCS: 44%.If compared, TCS has given far better returns. I am not able to find any advantage in Cyinet over TCS apart from better sales. Can someone please help to find if there are any?)

Decision: HOLD

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Sorry I am a bit lost here with your calculations whilst evaluating the company.

You say

1) market cap of Sical is 900 cr so 50% is 450 cr. 1/6 of 450 is indeed 75 cr (as you suggest) so the value of the holding should be 5/6 (discount = less by 1/6) which is 375 cr.

2) Similarly for the Mindtree valuation. 16.6% of 10,500 cr is 1743 cr of which 5/6 is 1452.

Both together contribute 375 + 1452 = 1828 approx. Add cash of 197 = 2025 so you get the other parts of the company for 6756 - 1828 = 4732 cr. Then add 2100 cr for debt EV = 6832cr (as opposed to your calculation of 7900 cr).

The difference in calculations is that you discount the value of the holdings of Sical and Mindtree to 1/6 whereas I discount by 1/6.

Maybe I am doing something wrong. Please advise.

Nevertheless, the story does not look good to me with the political angle and capital allocation.

BTW, apart from Rakesh Jhunjhunwala I believe his mentor Radha Kishen Damani is also an investor through his Derive investments. But why go by them. RJ also invested in A2Z maintenance and Bilcare.

Regards

Kumar

The ZAHORANSKY Customer Magazine

Shaily Plastics Engineering from India is Capturing the Brush Market with support from ZAHORANSKY

"In our cover story, our Indian customer Shaily Engineering Plastics

describes how all-round support from ZAHORANSKY – from product development

through to start of production and the implementation of a new technology

– works in practice. This story and other current highlights about the company

are waiting for you in the new issue of CONTACT".

http://zahoransky.com/files/PDF/Contact_Digital_01-2015_EN.pdf

Transaction banking is ofcourse going to be more critical because in developed countries the core banking segment is pretty stagnant because of stable population base.

All of these transaction banking , core banking , risk management are individual components with a plug and play feature. This is the basis of what in IT is called as component based architecture.

No bank will go for the entire suite as the risks would be too high. So you plug in areas with maximum demand. E.g. IDFC has chosen IDA for its transaction banking component only while its core banking suite will be something else.

Another info Rakesh Jhunjhunwala has further upped his stake in IDA as per the latest shareholding pattern. That is the reason for the current upswing.