took a look. The promoters have pledged 61% of their holding and it translates to 14% of total holding. Given that the promoters hold only 24% and have pledged 61% of that, IMHO - the valuations won't be a runaway....

PS - not invested

Posts in category Value Pickr

Neo Corp-Growth Machine in Technical Textiles(CAGR 45%)! (10-10-2015)

Support for fresh portfolio building – Thanks (10-10-2015)

- I would certainly advise you to read the entire thread and understand the 'context' in which the statement was made before passing your judgement about other peoples' statements.

- The comment was made with regards to investing in 0 debt companies which doesn't lead to wealth destruction. Also - I never said Kaveri Seeds is a bad company. As for wealth destruction, great businesses can destroy wealth as well. (If you invested in Infosys at its peak in 2001 - you needed to hold it till 2008 peak to just get your capital back. In my book that's wealth destruction, not sure what your definition is)

Since you're talking about price levels of buying. Let's take the case of an investor buying Kaveri Seeds on 1st June, 2015 at Rs. 950 after it declared it's FY15 results. At that point the company has a

4 year revenue and profit CAGR of 48% and 63% respectively. 0 Debt and ROE > 30% with a P/E of 22.

In any sensible investor's mind this company is not expensive with such great growth and profitability unless you have insider information about the company's future growth. At best, you'd think if the growth stops, I shouldn't expect any great upsides. So as the Q1 FY16 results roll in with a PAT of negative 2-3% YOY, that certainly shouldn't be the end of the world as it was never trading at an exorbitant P/E of 70-80+ !

But you know what - markets think differently and slash this 0 debt company's Market Cap by half!Losing 50% of your capital within 4 months of investment may not make a company bad but it would take several years of great results before it matches any other good investments (17-20% CAGR) apart from the emotional stress that the person would go through. And the point is 0 debt doesn't save the company from huge downsides!

Neo Corp-Growth Machine in Technical Textiles(CAGR 45%)! (10-10-2015)

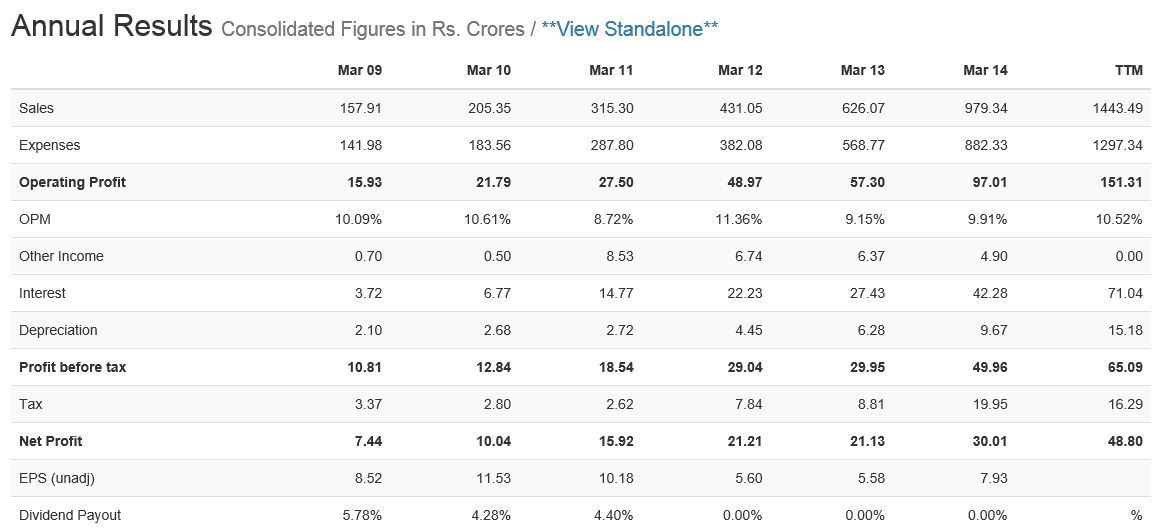

Updated based on the consolidated figure:

Revenue CAGR(5 year & 3 year) : 45%

NP CAGR(5 year) = 32% , 3 year: 24%.

For convenience of all, pasting the details from different sites:

1)From Company' official blog:

a)****Neo Corp Offers Avant-Garde Packaging Solutions

Across the country renowned leader in Packtech industry, Neo Corp International Limited has been delivering the best packaging solutions since its inception. Led by Mr. Sunil Trivedi, the company is holds an expertise in the field and this is aided with its use of ultra-modern technology. Neo Corp provides the most superior and cost effective solutions for storage, carriage and protection.

Neo Corp provides textile based temporary containment, carriage, storage and protection of industrial, agricultural and other goods. Mr. Sunil Trivedi, Chief Managing Director of Neo Corp International Limited, believes that packaging is an ideal application for textiles. From heavy weight woven fabrics which can be used for bags, sacks, FIBCs, wrappings for textile bales and carpets to lightweight woven fabrics used as Leno bags and other food and industrial product wrappings, Neo Corp deals in a variety of products.

Neo Corp produces three varieties of products under its Packtech industry:

Low GSM Products: Neo Corp presently manufactures PP/HDPE woven fabric which can be converted into Sacks/Bags, Wool Packs, Box Bags and Custom Design Bags. It is made of Polypropylene and the product range includes fabrics, box bags, sand bags, valve bags, bale wraps, wool packs, woven sacks, etc.

Leno Bags: Leno bags are permeable which allow air to pass and helps in keeping the product fresh. They are very flexible, efficient and can carry loads of over fifty kilograms. They are used for packing onions, potatoes, garlic, ground nuts, fruits and vegetables, flowers, etc. They are safe and remain fresh for longer durations. They can be easily re-used and washed. They have superior aesthetics, are chemically inert, cost effective and recyclable and have excellent mechanical properties.

FIBC: Neo Corp also provides a variety of filling and discharge options. Various kinds of filling options are available at Neo Corp which varies according to the difference in products. For example, tops are not required for cheap products, duffel top provides easy access whereas draw cord permits air flow but still confines the product. Neo Corp also helps people choose the right discharge options which saves both time and money. It also provides lifting options and liners and accessories.

b)An international Leader of Packtech, Neo Corp diversifying:

One of the international leaders in Packtech industry, Neo Corp International Limited (NCIL) has been expanding significantly. The company has a range of growth initiatives which have led to its diversification into Geotech and Agrotech segments also, adding to Packtech. With the company’s healthy financial past and its profits, it has made its place into National and Bombay Stock Exchanges as well as Luxembourg Stock Exchange. Neo Corp has had an excellent export performance and an equity base of 38.02 million shares. This has helped the company enjoy Government-recognized Star Export House Status. A planned capital investment and constructive management culture has helped NCIL encash all the opportunities that have come with easing down of trade norms.

NCIL’s two main subsidiaries are:

◾Europlast Limited

A UK-based company, Europlast Limited sources, stocks and distributes technical textiles to wholesalers and retailers of the product throughout Europe. The company has its headquarters in London, UK and was incepted in the year 1998. NCIL has been offering better returns by virtue of this subsidiary. NCIL has also been able to keep proximity to end users wherein the fidelity is higher, owing to Europlast.

NCIL has benefitted in more than one way through this subsidiary. It has also been providing better customer service and has a minimized credit risk due to debt insurance cover availability in UK for supply in whole of Europe.

◾IPC Packaging Company Pvt. Ltd.

IPC is a Bangalore-based manufacturer of PP / HDPE woven FIBC, jumbo bags, sacks, tarpaulins, box bags, PE liner etc. NCIL acquired the company in November 2014.

Spread over an area of 2.62 lac sq ft and a built up area of 2.04 lac sq ft, IPC is a hi-tech production plant and is situated very close to the industrial sector. NICL’s acquisition of IPC has advantaged the company in many ways.

Other subsidiaries of NICL include:

◾Sacos Indigo Private Limited

◾Netflex Infracon Limited

◾Polybase (HK) Limited

◾Polylogic International Private Limited

2)Chartered Accountant blog:

NEO CORP INTERNATIONAL LIMITED(NCIL) – BSE CODE-523820

NCIL is a Public Listed Company with an equity base of 38.02 million shares.

NCIL since its inception was dedicated towards making tailor made products under Packtech and now it has the status of one of the best and reliable suppliers in Packtech products internationally.

It has also entered two more segments of technical textiles namely Geotech and Agrotech.

It is listed only on BSE as of now. It was trading on NSE through Madhya Pradesh Stock Exchange (MPSE).MPSE is in the course of decognitiion hence NCIL permission to trade on NSE was withdrawn since 30th January 2015. The company has filed an application for relisting and should be traded on NSE soon.

NCIL is also listed on Bourse de Luxembourg(Luxembourg Stock Exchange).

CHARTEREDINVESTOR PICK

Technical textile sector is one of the most innovative branch of the industry in the world, ranking as one of the five high tech sectors with the greatest potential for development. The success of technical textiles is primarily due to the creativity, innovation and versatility in fibers, yarns and woven/ knitted/ nonwoven fabrics with applications spanning an enormous range of users. The ability of technical textiles to combine with each other and with others to create new functional products offer unlimited opportunities for growth.

Traditionally, North America and Europe have been the major markets for technical textiles in the past but in recent years, the sheer volume of demand from Asia Pacific has outpaced demand from North America and Europe. With better technology capabilities, ever increasing demand from different end user industries, technical textiles are expected have a huge market to cater to globally.

India’s export of technical textiles has grown from US$ 624.95 million during 2007-08 to US$ 1355.04 million in year 2012-13 with a CAGR of 17% indicates encouraging global demand for India’s technical textile products. Furthermore, the import of technical textiles has grown from US$ 835.82 million during 2007-08 to US$ 1434.97 million in year 2012-13 with a CAGR of 11% shows that Indian consumers have significant demand for technical textiles products.

These statistics highlight not only concerted domestic needs, but also India’s potential to address global demands, for technical textiles products. With advancing technology, higher integration with global markets and greater sensitization to market needs, the Indian technical textiles industry demonstrates significant potential, for the development of local industry and prospective entrepreneurs.

Technical textiles are an important part of the textile industry and its potential is still largely untapped in India.

NCIL MANAGEMENT:

Neo Corp is run by learned and highly experienced people from the related fields. Few of them are:

Mr. Shrawan Kumar Patodi : Eminent Lawyer having vast experience in the field of low and 10 years of experience as export executive. Educational qualification - B. Com. M.A., LL.B. and D.H.B.

Mr. Ladharam Patel : 40 years of experience in the manufacturing business.

Mr. Rollande Coderre : An entrepreneur from Canada having experience in vast number of fields like packaging, construction, etc. Educational qualification - Degree in Business Administration and business accounts & finance

THE NUMBER GAME

Let us have a look at the financial results of past years.

Neo Annual consolidated numbers from screener : Last year EPS 12.84

The numbers speak a lot about its performance. The return on the capital employed in to company over a period of 3 years is above 16%. Also the cash flow has been improving. At current levels, NCIL is trading at 2.5 PE which is very much lower as compared to the industry PE of 22. Also the business has huge potential to grow. Trading at 60% of its book value provides huge ground for upmove.

CONTROL MEASURES:

The company has hired world class professionals for proper control over the business activities. This has helped to improve productivity, provide better services, reduced cost and increased returns especially on human capital. The company’s internal control systems are commensurate with the nature of its business and the size and complexity of its operations.

STRENGTHS:

· NCIL products are of ISO quality standards and the BRC & Astho will enable NCIL to enter rich e markets.

· Worldwide ever increasing demand.

· It is also into business of Geotech and Packteck. Thus agricultural and infrastructural activities will give impetus to the growth.

· It has a large domestic market which helps to spread the risk.

· New acquisitions will add further to increase in proximity and develop new and better customer relations.

· NCIL has the highest production capacity of technical textiles in India.

WEAKNESS:

· The market is price sensitive and thus is susceptible to pricing pressure.

· Competition from other countries.

With a view to take on the competitors in the global markets, NCIL has been increasing its business and developing client relations. It had its business spread across 20+ nations and has been serving 550+ clients.

It has 6 subsidies namely

Europlast Ltd

Sacos Indigo Pvt Ltd

Netflex Infracon Ltd

Polybase Ltd

Polylogic International Pvt Ltd

IPC Packaging Co Ltd

Europlast Ltd was incorporated in UK in 1988 and was engaged in sourcing and distribution technical textiles. The acquisition of Europlast was very crucial. Europlast Ltd was operating for over a decade and established itself as the leading player in its business in Europe. Acquisition of Europlast has proved to be very much advantageous in the form of better customer services, reduction of risk on account of credit sales and also reaching out to more clients.

In the previous financial year NCIL made a big strategic more by acquiring IPC Packaging Co Pvt Ltd. IPC was acquired in November 2014. IPC Packaging Co. Pvt Ltd is based in Bangalore, the IT hub of India for the past 6 years and leading manufacturer of PP / HDPE woven FIBC, Jumbo Bags, sacks, Tarpaulins, Box Bags, PE Liner etc.. IPC has a huge hi-tech production plant spread over 2.6 million sq ft which is located very close to the Industrial sector. IPC was and is being run by veterans with experience of over two decades. This acquisition puts NCIL at the top in its business with highest production capacity in india.

In addition to the technical textile business, Neo Corp also represents Indian Oil Corporation Ltd as Del Credre Associate cum stockiest for the state of Madhya Pradesh. There are two production lines of 300 KTA each for Polypropylene (PP) with Spheripol technology license from Basell, Italy. The product portfolio includes entire range of Homopolymers, Block Copolymers and Random Copolymers.

There is a dedicated HDPE plant of 300 KTA using Basell (Hostalen) slurry process. The product portfolio includes Unimodal as well as Bimodal HDPE grades for various application segments such as Film, Blow Moulding and Pressure Pipes.

The low petroleum prices will benefit to a great extent the company’s polymer business.

AWARDS AND RECOGNITIONS:

· Neo Corp enjoys the Star Export House status recognized by the Government of India for the Company’s excellent export performance.

· It has a Trading House Certificate which is valid for a period of 5 years which ends in 2019. A trading house is an exporter, importer and also a trader that purchases and sells products for other businesses.

· On 22nd September 2014 its Inhouse R&D Units recognization was renewed upto 31st March 2017.

· NCIL is also a member of the Flexible Intermediate Bulk Container Association(FIBCA).

All the above discussions depict Neo Corp has a huge potential for a great up move and will prove its mettle in the coming times.

Firstcall Research has given "BUY" call on Neo Corp with target 64:

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (10-10-2015)

Chintan, Great analysis of sugar stocks. It may be more interesting to include some of other sugar companies like Rajshree sugar (13500 tcd), EID Parry (34750 tcd), Triveni (61000 tcd), Parrys sugar (4000 tcd), Thiru Arooran (8500 tcd).Please find various sugar companies mcap potential (rough estimates) if sugar stocks behave in similar fashion as during last major sugar cycle between 2003 to 2006. Some of these projections may look unbelievable.

Sugar Companies MCAP Potential.doc (31.5 KB)

Nifty PE crosses 24|A statistically informed entry-exit model! (10-10-2015)

I do not think that is correct, in case of the largest Index, i.e. Nifty. Nifty constituents had delivered on an unweighted basis negative trailing twelve month earnings growth as on June 2015. There have been recent replacements in Nifty that did not deliver, for instance United Spirits, but that was soon replaced by an older constituent that was brought back, Zee Enterprises. Again NMDC, a recent entry was replaced in Sept 2015.

In other words there seems to be a higher chance of a recent addition getting replaced whereas older new remain. The ones that got removed had poorer results than the incumbents. This would not have happened if the quality of earnings were improving.

Warm regards,

Support for fresh portfolio building – Thanks (10-10-2015)

Its a pretty bad statement that Kaveri seeds have destroyed the wealth of investors. Firstly one bad quarter/year does not make a company bad. Secondly it depends upon where you have bought stock in terms of its price - there are many great companies which loses 50% from recent high but it does not make them bad companies anyway. It seems now a days investors of today does not have patience long enough to ride through a company cycle over yrs neither have wisdom to buy stocks when fear is there.

Please be responsible in making statements.

Nifty PE crosses 24|A statistically informed entry-exit model! (10-10-2015)

Madhusudan kela speaks of how quality of index earnings has got better over time due to weaker companies going out of the index and being replaced by stronger companies.

By extension, past PE data/trends may not be true reflector of current valuations of the indices.

Support for fresh portfolio building – Thanks (10-10-2015)

Regarding the cash flows matching profits, I completely agree with you. Even I give high importance to the same. Yes, how the markets are today, there seems to be no importance to cash flows, however, times change, and things become clear in the long term.

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (10-10-2015)

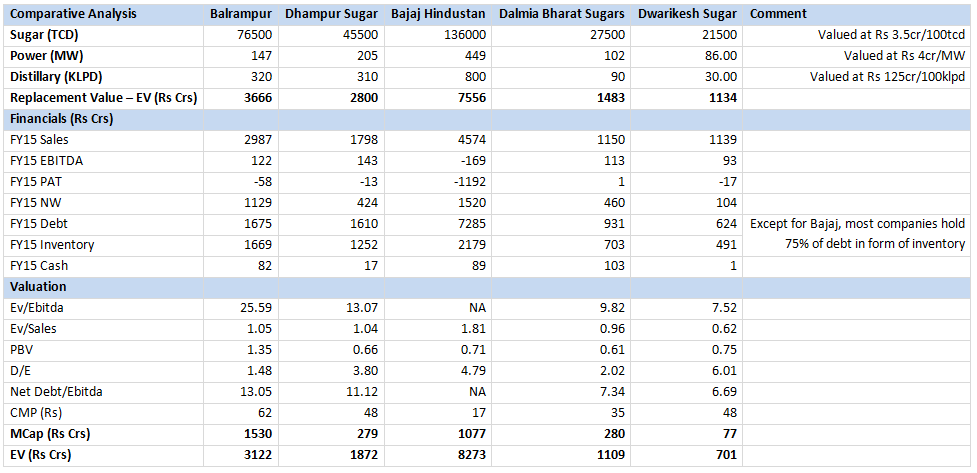

I tried to check few sugar companies based on their capacities and compared it as below:

• Balrampur remains best play in sugar sector with strongest balance sheet

o Compared to Balrampur, Dhampur Sugars have similar capacity of Cogen and Distillery however sugar capacity is half of what Balrampur have. Dhampur’s MCap Rs 279cr vs Balrampur’s Rs 1530cr. On Leverage side, Dhampur is more levered at 3.8x D/E than Balrmapurs’s D/E of 1.5x based on FY15 numbers.

• In Small cap, Dalmia Sugars remains better play given best in the industry recovery rate and have history of turning around sick units which they acquired in Kolhapur. It is one of the very few sugar company to report net profit in FY15

o However, Dwarikesh Sugars have almost similar capacity but have MCap of only Rs 77cr vs Dalmia’s MCap of Rs 280cr. This is partly due to high leverage in Dwarikesh (6x D/E). However, both companies have over 75% of debt locked in inventory.

• I would like to highlight that Debt figure is based on FY15 numbers and there is high likelihood of these figures at present will be much lower after liquidating sugar inventory as well as release of financial assistance by UP Govt in Q1-Q2. For e.g Balrampur had debt of over Rs 1675cr which came down to Rs 1200cr in June and another Rs 200cr which got released by UP govt will bring that debt figure to Rs 1000cr.

• Have not compared Shree Renuka in the list as their losses and debt figures are too high to make any sense plus their Brazilian ops is under bankruptcy.

One can play around the replacement cost for divisions - changing the numbers as feel fit - but just to highlight here...in FY13 and FY14 Dalmia Sugar have acquired 2 units in Kolhapur one was operating and another one was closed for 7 years and have turned it around..Operational one was bought at Ev/tcd of around 5cr (2500tcd at Rs 125cr) while closed one was bought at Rs 1.4cr (Rs 1750tcd at Rs 24.3cr). I have taken Rs 3.5cr/tcd valuation which i think is fairly conservative. Cogen (Rs 5cr/mw for a wind farm, Rs 4cr/mw for cogen is fair) and Distillery (based on interaction with Balrampur Chini IR).

Discl: Not invested in any of the above mentioned stocks, but as mentioned earlier it does look interesting.