As suggest by @desaidhwanil, an appropriate and meaningful disclose is expected from Mr. @abhijitchokshi

Posts in category Value Pickr

CCL Products (07-10-2015)

Firstly, SUPER CONGRATS for forum members for rightly recognising this company in its diaper stage. I'm a late entrant but still the company is sucking its thumb. Barring surprises, I would like to exit when it reaches adolescent stage or middle age.

I have updated my portfolio thread with my entry into CCL Products and here is the link to it (tried copy pasting the specific content but the format is gone, so putting the link here):

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (07-10-2015)

D/E of Balrampur Chini is close to 1.5.

My richdreamz portfolio – visit my portfolio to learn together! (07-10-2015)

I have entered into CCL Products this week. I'm done with my portfolio adjustments by introducing new companies for that ALPHA. There will NOT be any new entrants into my portfolio. Only re-alignments of the weights going forward.

Weightage: The stocks which are introduced for that ALPHA will be capped at 20-25% of the total portfolio.

PORTFOLIO

Stocks introduced for ALPHA: MPS, CUPID, CCL Products. (cap at 25%).

Core stocks: Repco, Gruh, PI Industries, Page industries. (cap at 75%).

Rationale for CCL Products (I have already explained the rationale for MPS, Cupid:

- Improving RoE/RoCE until FY18 where we have certain visibility.

- Reduction of debt and probably settle around 0.1 D/E or Zero debt by FY18.

- Super visibility of free cash flows

- Increasing dividend as a %ge of net profit with increasing cashflows

- Vietnam plant at 75% utilisation by FY 17 and then increase the Vietnam capacity to 20000 MT by capex of about 20 million USD funded entirely by internal accruals. No tax on Vietnam revenues for next 3 years and later 50% tax - effective tax rate is going to be low for foreseeable future.

- Immediate revenue visibility of 25% for FY 16 and 30+ EPS growth. (mostly built into current price, still scope of surprise exists)

- No recent history of equity dilution, ethical management, promoter holding increased from 3-4 years back and stabilised around 44%.

- Upside due to new big European client and entry into Japanese markets (very sticky market where long term revenue visibility would be high and management sounded positive on this new business).

- This is NOT a commodity business and also NOT a real estate intensive (no plantations). I really liked that they do the RAW MATERIAL purchase as per JIT (Just In Time) policy so they are completely insulated from coffee prices though realisations could vary by 7-8% in case of fluctuations as per management.

- Own brand retail foray: Very difficult preposition. Nescafe and Bru has SUPER mindshare of customers and breaking this could be difficult. However, the coffee is priced less than 50% the price of Nescafe for same quality - now beat this. Management only has to make people realise this. Difficult though.

- I'm Hyderabad and CONTINENTAL COFFEE has a shelf place beside Nescafe and Bru in Vijetha Super market. I took both the bottles and compared the price, packaging, bought home both of them and tasted. ( I will put my observations in CCL thread).

- Better late than never even though the valuations are a bit high and IF all the above story plays out well, there WILL be a PE re-rating as we cannot have a company growing at 25% plus, with near zero debt levels, with RoE and RoCE levels above 30, increasing dividend, free cash flows at 24 PE. Retail foray success (IF) will provide even further PE expansion.

Request forum members to provide feedback on this post. Many thanks!!

NCL Industries – Resumption of growth? (07-10-2015)

More release of pledged shares has been reported to exchanges. Market seems to be appreciating this development

Jubilant life sciences (07-10-2015)

Jubilant has been showing some interesting price trends in the last couple of months - I tried looking at this company in detail: Here is my write-up:

Summary of the below write-up:

1. Normalization of CMO (High positive impact)

2. Growth and pricing in Radiopharma (Medium positive impact)

3. New Generic molecule launches (Low positive impact)

4. Life Sciences (Neutral – positive in Niacinamide is negated by Pyridine)

5. Rupee depreciation – (Medium Negative impact)

Stock Story -

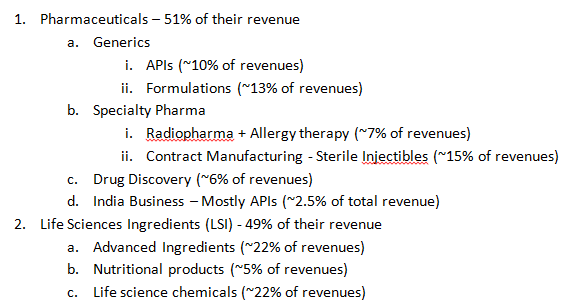

Jubilant is an integrated pharma company present in over 100 countries (incl Japan, China) covering a wide spectrum of the entire value chain in pharma industry – ranging from drug discovery to formulations business.

India business contributes ~27% of their topline. So the rest 73% is from their international operations.

Pharmaceuticals:

Generics(API + Formulations): Jubilant currently has 25 USFDA approved APIs/Formulations. Almost all of the molecules have very high competition. For instance 20/25 molecules have more than 12 players. In pharma whenever the competitive intensity is very high, generic companies usually don’t have pricing power. Even the recently approved molecule Zolmitriptan (Zomig) has 12 players. This molecule has a market size of ~ $100mn. Generics is NOT Jubilant’s forte. The attached spreadsheet has the complete list of their approved molecules.

Jubilant Life Sciences.xls (27 KB)

They have a total of 32 pending approvals from USFDA. – No Para IV filings – so even these filings may be competitive.

Speciality Pharma:

Radiopharma looks like the core strength of the company as it is a very complex field in medical chemistry and it has its own competitive advantages. The complexity of this business will create entry barriers. Jubilant has global leadership in the following products:

1. I-131 – Thyroid Cancer

2. MAA – Lung imaging

3. DTPA – Lung & Renal imaging

But this segment forms a very low % (~4-5%)of the overall revenues for the company. Hypothetically, even if this segment were to double in the next 1 year, Jubilant’s topline will grow only in low single digits. It is akin to having a lower allocation to a strong stock in a PF.

Contract Manufacturing:

Jubilant acquired Contract Manufacturing expertise through the acquisition of Holister and Draxis. They are one of the global leaders in Contract Manufacturing of Injectibles(among top 5 Contract Manufacturing injectibles in North America). Contracts in this business vertical are long term in nature and in some cases some of these contracts are multi-year contracts. Jubilant has 6 out of top 10 pharma majors as its customers. This is one of the stronger holds for Jubilant. But this segment suffered significantly due to USFDA warning letters for Spokane & Montreal facility. Management says Spokane operations have normalized now.

Life Sciences Ingredients(LSI):

Jubilant has global scale in producing the following:

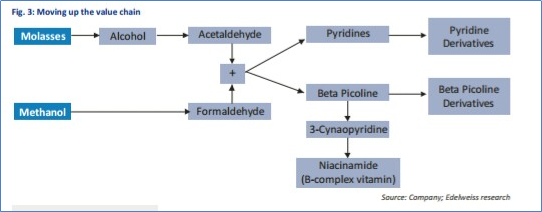

1. Acetyl

2. Pyridine(raw material being Acetyl which is produced in-house)

3. Pyridine derivatives

4. Symtet (value added product) – 24,000 MT capacity

5. Vitamin B3 – Niacinamide (value added product) – 10,000 MT capacity

Expenses as a % of total sales for this vertical has remained constant at approximately ~87%. So the cost advantage has not come from Jubilant Life Sciences vertical. This is a commoditized business with predictable business and as a result margins usually range around 15%.

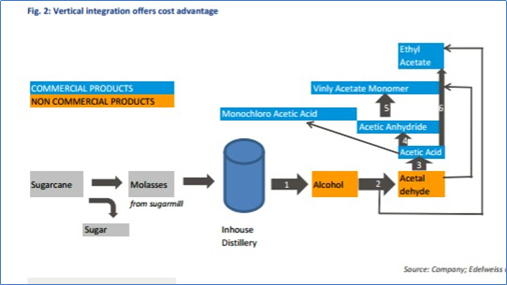

Company Produces Acetyl Inhouse:

Produced Acetyl is used to Manufacture Pyridines:

• In LSI vertical, the story is about operating leverage & Pricing Power as they have very large capacities in Pyridine & Niacinamide

• It is also about cost effectiveness – But Jubilant-LSI is already a cost effective player globally.

Methanol Prices have corrected significantly – lower oil being one of the culprits. Methanol is a key raw material for JLS.

http://www.platts.com/latest-news/petrochemicals/berlin/epca-european-methanol-to-stay-around-eur300mt-26229304

- Is there a Turnaround? –

Lower Raw Material Prices: The top-line has remained flat, though the improvement has come mainly from higher EBITDA. This EBITDA improvement is only due to lower raw material costs + price increases. Wouldn’t all companies benefit from lower raw material costs? Positive

Would rupee depreciation benefit Jubilant? – Check the below #s:

Currently their dollar denominated debt stands at $445mn + Rupee denominated debt at 1951 crores. Expressed in rupee terms their total debt stands at Rs 4785 crores. Rupee has depreciated from 63.34(Q1 closing) to 65.53 on 30th September. Assuming that their debt levels remains constant they will have an MTM notional loss of ~ 84 crores. Will this be offset from increase in topline? ~73% of their revenues is dollar denominated, which is approximately $167.35mn. Assuming constant revenues as of Q1, their topline would improve by only 31 crores. negative

Note – I have assumed constant revenues because, Jubilant has not been a story of improving topline. Its actually about improving EBITDA & improving borrowing profile(dollar denominated debt to rupee loans).- Management commentary on capacity utilization of the following facilities will be a key monitorable:

a. Niacinamide - Jubilant undertook a price increase of 10% for Niacinamide on June 16th for all its non-contract customers. positive

b. Pyridine – major market being china. There are lot of regulatory issues. So no meaningful improvement here. But the management says all the stress is already factored in. - They have a reasonably big exposure towards Chinese markets. Slowdown + yuan depreciation negative

- Montreal & Spokane operations have normalized(earlier they had a USFDA warning letter so this plant was operating sub-optimally) – big positive. Their contract manufacturing business suffered significantly due to this. Some of their customers walked out due to this. Management subtly says some new customers have come in.

Management Commentary on CMO Normalization:

“The production of the existing products goes on when the warning letter is there also.What stops is only the new product development. During that period,where the customers have alternate site,they would prefer to do in the alternate site, but they continue to remain customers.Only thing is,the additional orderflow was not getting generatedwhen the warning letter was there. So now that status has been changed.So customers know that the

site is okay for manufacturing, so the customers come back and that is why we say that normalization is underway.” - Aripiprazole – I did not understand this part. Have they started supplying this API to Torrent/Alembic?

Jubilant is like a portfolio of 6-7 businesses. That is to me is a negative because gain from one business will be offset by under-performance in the other vertical(Positive Pharma versus Below par Life sciences).

It is like concentrated portfolio vs a diversified portfolio.

Having said that, even from the current levels Jubilant looks interesting(due to falling raw material prices, stronger Radiopharma & normalizing CMO) even after factoring in around Rs 50-60 crore MTM losses. Their debt levels is a cause of concern.

Thanks,

Ravi S

Disc - No position as of now.

PTC India – A No Brainer (?) (07-10-2015)

"It is not what you are looking at, it is what you see...."

Henry David Thoreau

Dear Elusionist,

Why complicate everything with these "holding company discounts" and this and that.

Just look at it as a standalone company that you - a billionaire investor - are being offered for sale. Forget about everything else.

The sale price is Rs. 60 per share. The company has Rs. 28 in cash in the bank - CASH. Another Rs. 34 if you calculate a very conservatively valued market price of a listed company called PTCFS (forget about it being a subsidiary and everything). That is more than the price you are paying in the first place.

THEN. You have another Rs. 31 in cash receivables etc. - none of which is dodgy or doubtful. And you have a 11% stake in the Teesta-III HEP in Assam. And you have own stakes in Athena Power and others.

ON TOP OF THAT. You are getting a wonderfully run business which is the market leader in its field whose rather conservative management expects business to grow at 10-15% in the next few years. More if a few macro issues are resolved.

So would you buy the whole company if you were a multi-billionaire.....because I don't know how you became a billionaire if you haven't already taken that deal....

And as far as your comment to the effect that "...but the Company will never sell those shares...." are concerned - then theoretically the only way to value a company is its Dividend Yield. That is all the money you are REALLY getting. They are not going to give you the assets - so the book value / asset value should mean nothing. They are not going to give you their earnings - so the cash flow also has no meaning.

When in fact it does. That is what you and I look at when we purchase equity ownership in Companies through the medium of the Stock Markets - don't we??

Just look at it as if you were a billionaire buying the entire Company. Forget about everything else. It is all yours. You will never go wrong that way.

Also, by the by, two very important developments are going to help this Company in the future.

a) Recap of the SEBs should be approved by the Cabinet today itself. This will help in two ways. First the possibility of them having non-performing receivables decreases. Two, the SEBs will now be in a position to purchase more electricity.

b) There is a humongous push for rationalization of the grid linkages over the next few years. That too will increase the business for them.

My two cents.

Regards,

Mohit

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (07-10-2015)

The inventory levels of Sugar are still high, but post December 2015 the Ethanol prices are fixed at Rs.49 which is very lucarative and the govt incentive of Rs.4000/T of sugar if the industry crosses the 4MT of Sugar exports. These two can be huge booster for the industry. We can look at playing this with Balrampur Chini (Debt to Equity is just 0.4 inspite of huge capacity) and can also look at Praj Ind an indirect beneficiary of revival of Ethanol blending.

Disclosure : Not invested yet, but tracking closely.

Vivek Gautam Portfolio (07-10-2015)

Hi

I wanted to know your views on it as you are holding Aurobindo Pharma

Regards,

Kapil Gupta

Avanti Feeds (07-10-2015)

India continues its rapid volume growth of 34% in the US, despite overall volume declining by 10%

- Strikingly in contrast, all other major countries have shown a decline in volume, with Ecuador and Vietnam falling by 20% and 40% respectively in August

- Market share of Indian shrimp import has increased to 31% in the month of August 2014, from 21% last year

- Year to date market share has also improved from 17% last year to 23% this year

- However there has been a major decline in prices of shrimp in the US..to $8.75 from $10.83/kg last year

Source : http://www.undercurrentnews.com/2015/10/06/us-september-shrimp-import-value-volume-dive/

Disclosure : Invested from sub 500 levels