Thanks Ashish. there are many infra triggers in the region. Google will give you all the details.

Posts in category Value Pickr

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (04-10-2015)

Transportation of cement is one of the biggest costs. Local cement companies will have huge cost advantages compared to those far away. The cement required has to be supplied by all...one guy just cant do it. the rising tide will lift all the boats, we just need to see which will give the maximum ride with highest margin of safety.

Sagar is a confusing story. They sold a plant. Then they bought another plant. Debt levels are also high.

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (04-10-2015)

really impressed man. good write up.

the company is located at such a perfect location. also a tech zone is planted in raysellam district, a dam,a capital, polavvaram canals.

its being at the right place at the right time.

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (04-10-2015)

They already sell in all the south markets. I believe they have a decent brand recall but obviously will get dwarfed by the biggies. Which is why i feel it is a specific 2019 stock story.

Radico khaitan: a ignored spoiled child (04-10-2015)

Radico Khaitan is one of India's oldest and largest liquor manufacturers. Formerly known as Rampur Distillery which was established in 1943. It was only in 1999, that Radico decided to launch and market its own brands, thereby embarking on a period of phenomenal growth. To further boost its production capacity of bottled and branded products, the company has tied up with bottling units in various parts of the country.

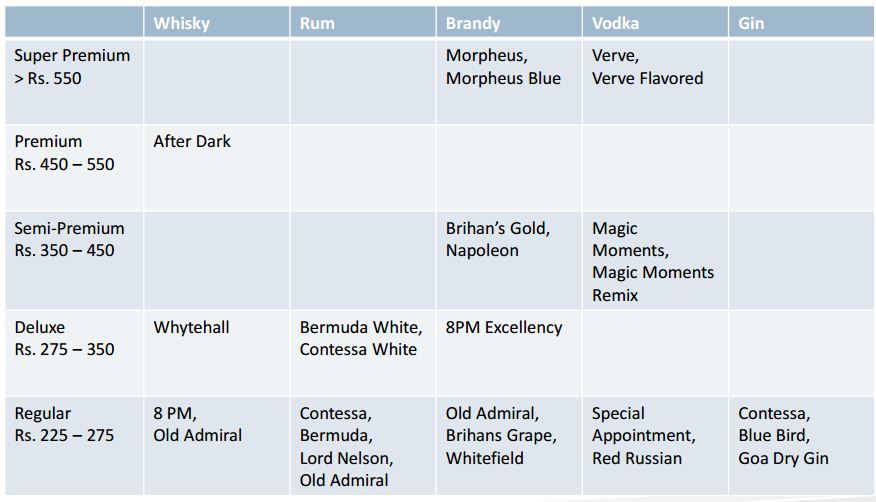

Radico Khaitan Ltd today has four millionaire brands in its portfolio. Radico's flagship brand, 8 PM Whisky, launched in 1999, was a runaway success. In the first year alone, it sold one million cases - a record for any Indian or foreign brand operating in India. This also made it the first brand in the liquor industry to makes it to the Limca Book of Records. The other millionaire brands are Magic Moments Vodka, Contessa Rum and Old Admiral Brandy. Today Radico Khaitan has brands that straddle almost every market segment and price category.

Radico Khaitan is India's oldest alcoholic beverage company. It entered the IMFL segment in 1999, with the launch of its flagship brand, 8PM. RDCK has three distilleries in Rampur, UP and holds 36% Interest in a JV in Aurangabad, Maharashtra. It owns six bottling units and maintains 27 contract bottling units. It holds 8% market share in the IMFL industry and ~24% market share in the CSD segment. The company offers all types of liquor, except for beer and wine, in regular and premium categories.

RADICO KHAITAN PRODUCT SPREAD

INDUSTRY OUTLOOK

The Indian liquor industry is a high risk industry due to higher taxes and innumerable regulations governing it. As a result, Indian liquor companies are suffering from low pricing flexibility and have insufficient capacities, which is consequently leading to their poor financial performance.

During FY2011 to FY2015 Indian liquor companies witnessed pressure at the operating level due to high competition and firm ENA prices. During the same period, various Indian liquor companies like United Spirits, Tilaknagar Industries, Globus Spirits and RKL reported EBITDA margin reduction of 1,255bp, 1,198bp, 850bp and 448bp, respectively. Also, the companies have high debt on their balance sheets, thus resulting in higher interest costs, and in turn lower profitabilities.

IMPROVING SIGNS

Liquor companies suggests that the industry has now bottomed out. It is now expected the industry’s pricing environment to likely get better going ahead due to the following reasons:

(a) Since the last two years, the industry has not received any significant price hike in its products due to delay in approval by state governments for the same.

Radico Khaitan has received price hikes in only a few states in the last eight quarters. Hence, the industry is now expecting significant price hikes in the coming financial year.

(b) The industry leader – United Spirits - is facing pressure at the operating level and the company has a huge debt on its balance sheet. Hence it is expected that the company’s new Management would shift focus on profitability over volume growth, which in would lead to increased scope for other liquor companies to hike prices.

Higher mix of Premium products to drive profitability for RKL

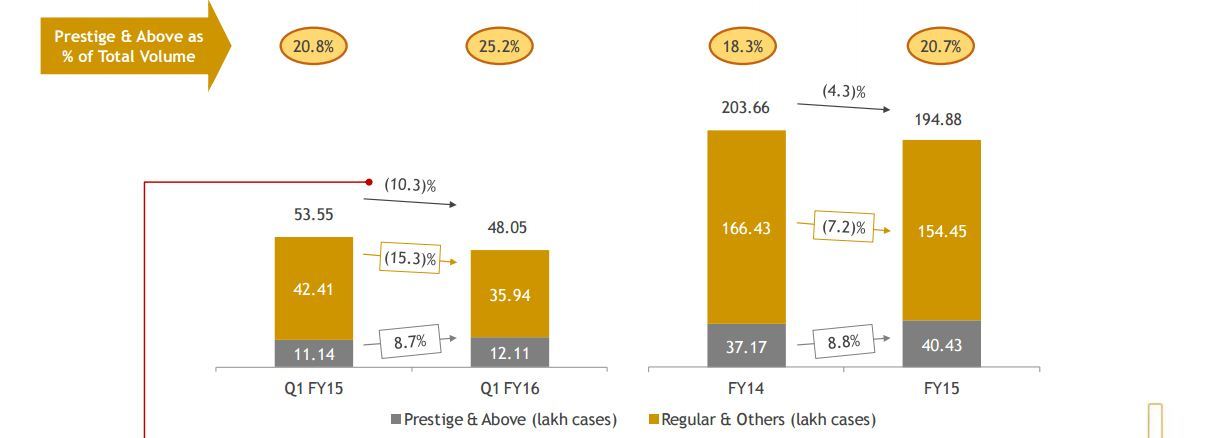

In the IMFL segment, more than 20% of the company’s volumes come from prestige and above products like Magic Moments Vodka and Morpheus Premium Brandy, and the balance from regular and others brands like Old Admiral Brandy, Contessa Rum, 8 PM Whisky etc. The company’s prestige and above brands command higher margins than regular and others brands. Since the last seven years, the company’s prestige and above brands’ volume has reported a CAGR of ~26% and their share in the product mix has increased from 7.9% in FY2009 to 20.7% in FY2015 and to 25.2% in Q1FY2016 due to strategic defocus on low margin products.

RKL is now more focused on selling higher margin products like Magic Moments Vodka and Morpheus Premium Brandy. Also, we expect volume contribution of prestige & above category products in IMFL segment to increase which would improve the overall margin for the company and result in higher profitability.

Raw material prices expected to ease

The price of extra neutral alcohol (ENA), a key raw material for the company, to remain stable and potentially even decline going forward. This is because sugar production during the October 2014 to May 2015 period has risen by ~16% yoy to 27.9mn tonne, which is an 8-year high production level. As a result ENA (a by-product of sugarcane) production too would be higher this year.

The procurement cost of petrol (excluding taxes) has reduced from ~48/liter in July 2014 to ~34/liter in July 2015 due to falling crude oil prices. Earlier, oil companies were procuring ethanol (to blend with petrol) at 44-45/liter when the procurement cost of petrol was around ~48/liter. Now, the price of petrol is around ~34/liter and ethanol costs around48-49/liter which makes it unviable to blend ethanol with petrol. Thus, this would cut down demand for ethanol and lead to a decline in its prices.

Wide distribution network with strong brands

RKL has a strong sales and distribution network with a presence in retail and offtrade outlets in the relevant segments in different parts of India. Currently, the company is selling its products through over 45,000 retail outlets and over 5,000 on-premise outlets. Apart from wholesalers, a total of around 300 employees divided into four zones, each headed by regional profit centre head, ensure an

adequate on-the-ground sales and distribution presence across the country.

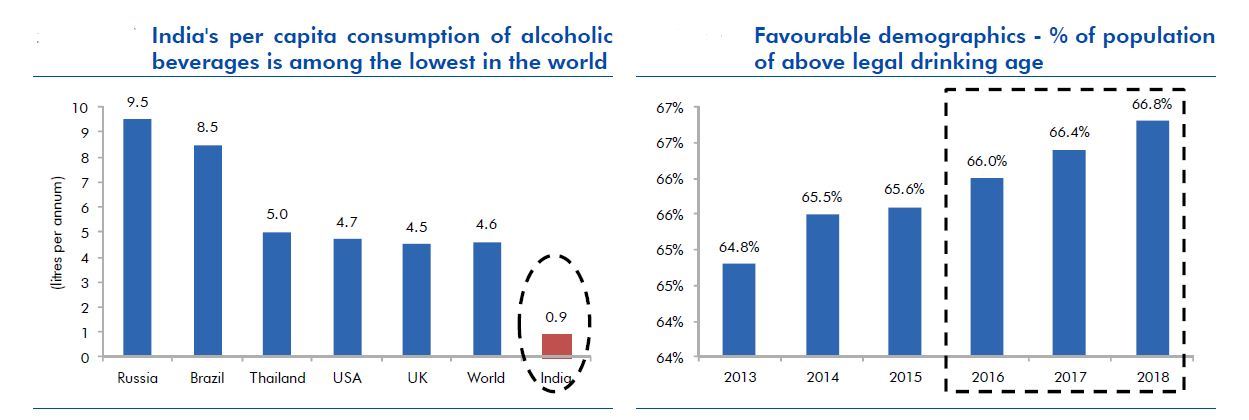

LOWEST PER CAPITA CONSUMPTION IN INDIA AND FAVOURABLE DEMOGRAPHY

HIGHER FREE CASH FLOW AND REDUCING DEBT

According to latest company presentation, it is focusing on cash flows and have reduced debt fro 903cr to 849cr in fy15.

CHEAPER THAN MOST LIQOUR COMPANIES

RADICO KHAITAN IS TRADING AT SIGNIFICANT DISCOUNT TO UNITED SPIRITS AND WE CANNOT CONSIDER TILAKRAJ INDUSTRIES BECAUSE OF VERY BAD SHAPE OF CURRENT OPERATIONS.

KEY RISKS

1. Indian liquor markets are highly regulated and have many taxes.

2. Liqour price increase is a political calss generally.

further relevant views are invited

Disclosure: i dont own any equity in the dicussed scrip.

Alembic & Alembic Pharma (04-10-2015)

Is this kind of news might impact FDA body towards future approvals and stringent scan on the current products currently being shpped?

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (04-10-2015)

Nicely researched report.

one more thought is, building a capital requires huge quantities of cement and generally it would be better to acquire cement from 2-3 vendors who are large enough to provide in such huge quantities. Does Deccan cement currently have that capability? How does its capacity weigh when compared to giants in this industry.

OUT OF TOPIC: Also, investment thesis depending on capital construction may not be a safe idea, as we never know what Chandrababu Naidu would do while giving tenders to cement companies? Given that the opportunity is so huge, he may build a cement plant or buyout an existing one and up the capacity so it becomes captive plant for capital needs? Or Crony Capitalism may play a part here and all cement procurement tenders would go to some of his buddies' business outfits. Again, as indicated, this is just to be careful thought as dealing with govt. orders will have its share of red-tapism, I do not imply that this will happen.

How does Sagar Cements look like in comparison to Deccan cements?

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (04-10-2015)

Very nice write up. But why would you think it can compete with UntraTech/ACC/India cements, are they not in a position to serve the demand of new construction? And what will happen after the capital construction boom slows after 4-5 years? Does the managament have inherent quality to expand the foot print and explore newer markets?

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (04-10-2015)

I have been wanting to write this for a long time, finally got around to it thanks to a long weekend , most of which was dry !

Deccan Cements is one of the smaller cement companies in the south. What impressed me most about the company is the financially disciplined conservative management and the

Lets begin with the most basic facts

Started in 1979 by a technocrat MB Raju

The plant started productionin 1982 current capacity is 2.3 million tonne per annum

The plant is 165 km from Hyderabad and appx 175 km to Guntur district, where the new capital of Andhra Pradesh ( Amravati ) is going to come up

The plant manufactures a wide variety of cements, including specialty cements. The regular grades of cement manufactured include OPC 43, OPC 53, PPC and PSC. Specialty cements produced include S53 for railway applications, SRC (Sulphate Resistant Cement), Low Heat Cement, Low Alkali Cement etc. ( source : Co website )

One of the main inputs in the production of cement is limestone. Deccan’s own captive limestone mine, having abundant high quality limestone, is contiguous to the plant premises

The other main input is power. Here also the company is more or less self sufficient with a Captive Thermal Power Plant (15MW), Hydro-electric Power Plant (3.75MW) and Wind Mills (2.025MW) under its fold.

Equity is only 7 cr

10 paid up

56% with promoters

No pledge. No warrants outstanding. No equity overhang

CMP 445. Mcap 311 cr

Long term debt as on 31st March 2015 was 116 cr. Thus total EV = 427 cr. I am ignoring short term debt on books as current assets > current liabilities by 50 cr

Thus EV per tonne in USD for Deccan is = 427cr converted to $ divided by 2.3 million = 28$ per tonne, which is way off the rates at which integrated cement plants have been valued in the recent past ( JPsold its plants to Ultratech for 140$/tonne . Lafarge recently sold 5.15 mt plant to Birla Corp for 5000 cr at an implied value of 149$/tonne )

Q1 2105 operating profit was 28.73 cr as compared to 6.42 cr in the same quarter last year

Last year the company sold 1.07 mt of cement against an installed capacity of 2.3 mt, implying a capacity utilization of 46%.

Even at this level of under performance, the company made 89cr of operating profit for FY15.

The EBITDA per tonne comes to 830/- for last year. Cement prices have since then firmed up and now realizations are upwards of 1000 per tonne.

Q1 EPS is 19.88 ( not annualized )

Stock already owned by IL&FS trust (9.5%) and UTI Midcap (5%). Institutional ownership is up by 10% over the last 4 quarters

Sagar cements releases monthly sales figures for themselves . Sales are up 18% yoy with accelerated growth in recent months. EBITDA per tonne is also up. Should apply to Deccan also.

what i like about the company

To the best of my knowledge , the company has not diluted the equity since its listing

Company increased its capacity from .3 mtpa to 2.3 mtpa without raising capital. It was funded from internal accruals as well as debt.

company has no capex planned in the near future

company generated 408cr as cash flow from operations between FY2010 to FY2015. This needs to be seen in the backdrop of the downturn of Andhra fortunes after the demise of YSR Reddy in 2009. Also, the subsequent Telangana issue has hampered growth in Deccan’s key markets

Out of 408 cr CFO, the company repaid loans worth 359 cr ! ( gives comfort on realness of the number )

By FY16 , the company is expected to be debt free.

The operations seem to be very efficient in terms of wage cost. Comparison of peer companies is as follows

Company name Wage %

Sagar Cements 4.56%

NCL 4.22%

KCP 3.84%

Deccan Cements 3.01%

The executive directors take the minimum wages as per the companies act ( source page 41, FY15 AR )

Company will benefit from its proximity to both Amravati and Hyderabad.

Construction of the capital will lead to a multi year boom for cement companies operating in the region. Search 'Amravati Andhra Pradesh Capital ' on google images to see the image of the proposed city.

Valuation for FY19

Investment has to be made with a 3 year horizon

I am assuming capacity utilization will hit 80%

Sagar cements in their latest concall have indicated an EBITDA figure of 1500 per tonne in AP already. I am assuming it at 1200 per tonne in 2019

Debt will be zero.

Tax rate will be 25%

The number can look something like this

Total capacity : 2.3 mtpa

Capacity Utilization : 80%

Total sales : 18.40 mt

EBITDA per ton : 1200

Total EBITDA in lacs : 22080

Less Dep in lacs : - 2000

Less Tax in lacs: -5020

PAT in lacs : 15060

number of Shares in lacs : 70

EPS : 215

Given the potential for development in the region, capacity utilization of 80% seems reasonable.

Also, the company would have close to 400 cr of cash generated from FY16/17/18 operations. I also believe with no impending capex / loan repayments, the company may aggressively step up its dividend payout or go in for buybacks.

Sometimes , a boring companies in a boring business can generate a lot of wealth. I believe Deccan at this juncture merits closer viewing.

Mcap when posted : 311 cr

Disclosure : invested at these levels

Duke Offshore – Hidden Gem? (04-10-2015)

I also have investment here. Not very sure of moat and its competitors but when I saw work from defense then I took that as moat.

Also, I saw base for profit was very small for sept and Dec. So, if it could give positive results in coming qtr then we can hope of big gain. Old tender won still have time to expire so pretty safe. But I don't know why its profit was low for sept and Dec qtr and why it posted very good result in March qtr!

Due to low liquidity, we can't add big money here. Just 1 lakh rupees can buy nearly 2000 shares and most of the days, 2000 total shares traded.

I am also hoping gain from recent de freezing of oil fields by govt. Tenders for that will start in 3 months time from now. What do u think of that? Can it get anything from there?

Invested here.