No representation of certain good sectors like IT and agrochemicals,

KVB and Jagran prakashan I have doubts over if they deserve a place in such a concentrated portfolio

Posts in category Value Pickr

Ranvir’s Portfolio (29-09-2015)

Varun 2020 portfolio – 2 strategies (29-09-2015)

Well, I think on the long-term, the difference in cost of capital between India and USA is about 7%....

Varun 2020 portfolio – 2 strategies (29-09-2015)

When he made this statement the interest rates were not as low as today - and anyways in India as well ROE of above 15-18% is perfectly ok and is sustainable over long term for financials business - the more above 18% is better

Varun 2020 portfolio – 2 strategies (29-09-2015)

ROE > 15% in USA or India?

Cost of capital is significantly different in USA and India

Varun 2020 portfolio – 2 strategies (29-09-2015)

Sunny

D/E ratio in case of financial stocks do not matter and should not be looked into so much

I would suggest that you read warren buffet take on how he values financial stocks as he is in the past and even today the biggest investor of financial stocks especially banks - he suggest to always look into ROA and then ROE over long term - ROA should always be greater than atleast 1.5 over time and ROE >15 % on sustainable basis

As for pledging of shares I have highlighted this in my thesis - its a small issue looking at credibility of Rashesh Shah - am overlooking into it

Hindustan media ventures: a play on literate india? (29-09-2015)

Hi Ashish

Welcome to the forum. There is already a reasonably detailed thread on HMVL. It's quite informative and discusses most of the points you elucidate in detail. Have a look. Might be helpful.

Sachit

GRUH Finance – mini HDFC (29-09-2015)

I know some famous investors have been making apples-to-oranges comparison between India's mortgage-to-GDP ratio and that of developed countries like USA.

Lets try to put that in perspective.... How fair / unfair is such comparisons??? Two key things come to my mind.....

- Housing loans interest rates in India are at 12%-14%, while in US/Germany they are 2%-4%

- Only 6% of Indians are employed in organized sector, while in US more than 90% are employed in the formal sector

What the former means is that the EMI on a 15 year housing loan in India would be ~ 2x of the EMI on the same housing loan in USA/Germany.... So, in effect on a like-to-like basis, India's mortgage-to-GDP ratio has to be multiplied by 2x, which makes it 20%

What the latter means is that only a far smaller number of the people contributing to India's GDP are credit-worthy. For a like-to-like comparison - you may want to shave off at least 2/3rds of India's GDP in the mortgage-to-GDP ratio.... which in effect means that the mortgate-to-GDP ratio goes up another 3x (that is, from 20% to 60%)....

If you take these 2 factors into account, you will realize why a 10% mortgage-to-GDP ratio in India, is probably worse than a 70% mortgage-to-GDP ratio in USA/Germany.....

Just a word of caution to people who have excessively high allocations to Gruh/Repco - Because these lend to the borrowers from the informal sector, they are a double-edge sword - don't find yourself in the wrong place when the wrong edge of the sword swings towards you...

Disc. Not invested. This is not a recommendation - please do your own research.

Hindustan media ventures: a play on literate india? (29-09-2015)

HELLO GUYS.

THANKS FOR YOU FOR LETTING ME A PART OF THIS WONDERFUL FORUM.

LET ME INTRODUCE MYSELF.

I AM ASHISH GUPTA, AGE 21

STARTED INVESTING IN 2010.

LOST 2LAC IN 2011 AND THAT LED ME TO INTROSPECT AND VALUE INVESTING.

OK NEVER MIND, TODAY I WANT TO DISCUSS ONE STOCK WITH YOU.

HMVL

- owner of HINDUSTAN

*LARGEST NEWSPAPER IN BIHAR, JHARKHAND. SECOND LARGEST IN UP.

PROS:

1.CONSTANTLY INCREASING OPM FROM 17.07 IN FY10 TO 20.33 IN FY15

NET PROFIT MARGINS INCREASE FROM 10.31 TO 17.20.

ROE INCREASE FROM 14% TO 19.19%.

MARKET CAP OF RS.1650 CR AND NET CASH OF RS 576CR.

BIHAR ELECTIONS ON ANVIL.

INSPITE OF GENERAL ELECTION ADSPENDS IN Q1FY15,

IT SHOWED A REMARKABLE INCREASE IN Q1FY16.

PROFIT INCREASED BY 23%.DECREASING PRICE DIFFERENTIAL BETWEEN ADRATES OF ENGLISH AND HINDI NEWSPAPERS.

INREASING READERSHIP AND CIRCULATION REVENUE.

CONS:

1. NO SPECIFIC AGENDA FOR DEPLOYEMENT OF CASH HOARD.

- VERY LOW DIVIDEND INSPITE OF HEALTHY CASH FLOWS.

THIS STOCK DESERVES A DEEP LOOK AS IT IS AVAILABLE ON PE OF 10.

Nitin Spinner – textile yarn story (29-09-2015)

Note that in towels India gained but not at the expense of China, whose share has also jumped from 23% to 26%. In sheets though the dominance is clearly visible.

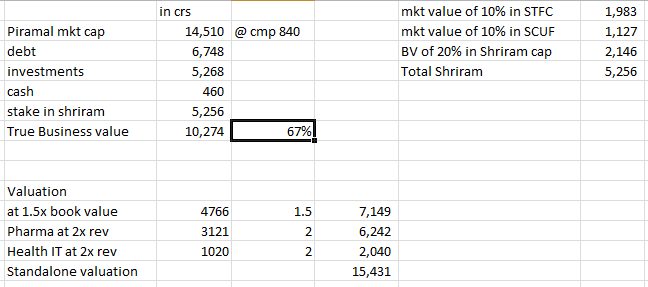

Piramal Healthcare (29-09-2015)

Dear Dhawanil sir,

Thanks for your valuable inputs to this thread and to the forum. I have been invested in Piramal for few years and I use a rough back of envelope valuation. Very glad to know it is in lines of senior investors like your's.

Query - I am backing out investments (non Shriram) to arrive at true business value and comparing it against standalone valuation that includes NBFC book.

Are these investments different (via Piramal Realty) or they are part of NBFC books leading to double counting.

Will appreciate if you could share your views. Thanks for your time.

Regards,

Sai