Vivek -Thanks for the information. Quite disconcerting this article is. Lets see the development in future. I guess the AGM is scheduled on 29th Sept. Will take a call only after that.

Posts in category Value Pickr

Strides_Arcolab (22-09-2015)

this acquisition could be good in the longer run. However, in the immediate future the challenge is going to come from its significant emerging market exposure. This part of operations will face huge fx pressure in the coming months due to fed hike or overall eco weakness and that is keeping the market edgy. Even Australian exposure will face currency challenges due to commodity weakness but it can be hedged by moving manufacturing to India over the next one year. Only thing can save them is faster rump up of developed world formulations.

Strides_Arcolab (22-09-2015)

this acquisition could be good in the longer run. However, in the immediate future the challenge is going to come from its significant emerging market exposure. This part of operations will face huge fx pressure in the coming months due to fed hike or overall eco weakness and that is keeping the market edgy. Even Australian exposure will face currency challenges due to commodity weakness but it can be hedged by moving manufacturing to India over the next one year. Only thing can save them is faster rump up of developed world formulations.

Varun 2020 portfolio – 2 strategies (22-09-2015)

Kishor Hi - Yes I said that and I have good stake in Glaxo Consumer. TTK Prestige especially after Nalanda Picked up stake at 2700 something never stopped its journey and currently its too expensive for me to buy it, I also believe that emergence of online platform has disrupted the business model of both Hawkins and TTK prestige and unless they do something soon they will start losing market share. Anyways I am positive but only below 3000. P&G never corrected a lot. I keep on trading on it though for 100 bucks time and again as it is safe stock to trade. Bajaj Corp is very expensive.

Pidilite has excellent growing and niche business model but I find it too expensive. Have not done any intrinsic value calculations but at more than 40 PE I have no courage to buy for investments. Since I am an Architect I meet lots of sales representatives of Pidilite about their products. Last interaction at few weeks back suggest that they are finding it tough going as there is a massive real estate slow down. Their water proofing and insulation products are slightly expensive as compared to peers and even the best of builders don't look at brand in this area of building as they need cost cutting. Fevicol and Fevistick are only growth drivers till real estate picks up. My believe is fundamentals are good but the stock its pricing too much expectations and there may be some disappointment going forward. Stock may not correct much but there could be time correction.

Titan - Few weeks back I came across lots of start up apps with a business model of renting out the jewellery. If this becomes a trend in future then it many impact the Titan business though in small way. Titan is in a business currently where you in need valuations at your side for investments. At current valuations though it has corrected a lot I still find little value.

As Warren Buffet Says - Investors of today will not benefit from yesterday's growth

Varun 2020 portfolio – 2 strategies (22-09-2015)

Kishor Hi - Yes I said that and I have good stake in Glaxo Consumer. TTK Prestige especially after Nalanda Picked up stake at 2700 something never stopped its journey and currently its too expensive for me to buy it, I also believe that emergence of online platform has disrupted the business model of both Hawkins and TTK prestige and unless they do something soon they will start losing market share. Anyways I am positive but only below 3000. P&G never corrected a lot. I keep on trading on it though for 100 bucks time and again as it is safe stock to trade. Bajaj Corp is very expensive.

Pidilite has excellent growing and niche business model but I find it too expensive. Have not done any intrinsic value calculations but at more than 40 PE I have no courage to buy for investments. Since I am an Architect I meet lots of sales representatives of Pidilite about their products. Last interaction at few weeks back suggest that they are finding it tough going as there is a massive real estate slow down. Their water proofing and insulation products are slightly expensive as compared to peers and even the best of builders don't look at brand in this area of building as they need cost cutting. Fevicol and Fevistick are only growth drivers till real estate picks up. My believe is fundamentals are good but the stock its pricing too much expectations and there may be some disappointment going forward. Stock may not correct much but there could be time correction.

Titan - Few weeks back I came across lots of start up apps with a business model of renting out the jewellery. If this becomes a trend in future then it many impact the Titan business though in small way. Titan is in a business currently where you in need valuations at your side for investments. At current valuations though it has corrected a lot I still find little value.

As Warren Buffet Says - Investors of today will not benefit from yesterday's growth

Thomas Cook India-Will it move like Warren Buffet Stock (22-09-2015)

Trouble brewing?

According to a media report, Quess's (a subsidiary of Thomas Cook), IPO hit road block. There is a difference of opinion between Prem Watsa and the original promoters of Quess. The company had acquired 74 percent stake in Quess (earlier known as IKYA) in February 2013 for Rs 256 crore. As on September 8, 2015: Watsa’s Fairfax holds 67.86 percent stake in Quess. The remaining 32.1 percent Stake in Quess is held by Ajit Isaac and employees. Report says that Thomas Cook is against allowing Isaac to increase his ownership to higher than 25 percent. Quess contributes around 80 percent to consolidated topline and 50-55 percent to EBIT. CNBC TV18 has not verified the story independently and can not vouch for it’s authenticity

Thomas Cook India-Will it move like Warren Buffet Stock (22-09-2015)

Trouble brewing?

According to a media report, Quess's (a subsidiary of Thomas Cook), IPO hit road block. There is a difference of opinion between Prem Watsa and the original promoters of Quess. The company had acquired 74 percent stake in Quess (earlier known as IKYA) in February 2013 for Rs 256 crore. As on September 8, 2015: Watsa’s Fairfax holds 67.86 percent stake in Quess. The remaining 32.1 percent Stake in Quess is held by Ajit Isaac and employees. Report says that Thomas Cook is against allowing Isaac to increase his ownership to higher than 25 percent. Quess contributes around 80 percent to consolidated topline and 50-55 percent to EBIT. CNBC TV18 has not verified the story independently and can not vouch for it’s authenticity

P. I. Industries Ltd. – A Unique Business Model can make it a Great Play on Agri & CSM Space (22-09-2015)

Quoting from this recent article

In recent annual general meetings, P I Industries Ltd and Bayer CropScience Ltd were cautious about their domestic agrochemical business and gave the impression that growth in the current fiscal year can be slower than last year, analysts say.

“On the back of three weak consecutive seasons, we expect working capital cycle is likely to deteriorate going forward. Generally, retailers sell agrochemicals on credit to dealers, which is to be repaid at the end of the harvesting season. From companies’ side, firms give credit of around three months to dealers. We expect debtors’ days to stretch further,” B & K Securities added.

This off course should not apply to the CSM part of the business as far as PI is concerned.

P. I. Industries Ltd. – A Unique Business Model can make it a Great Play on Agri & CSM Space (22-09-2015)

Quoting from this recent article

In recent annual general meetings, P I Industries Ltd and Bayer CropScience Ltd were cautious about their domestic agrochemical business and gave the impression that growth in the current fiscal year can be slower than last year, analysts say.

“On the back of three weak consecutive seasons, we expect working capital cycle is likely to deteriorate going forward. Generally, retailers sell agrochemicals on credit to dealers, which is to be repaid at the end of the harvesting season. From companies’ side, firms give credit of around three months to dealers. We expect debtors’ days to stretch further,” B & K Securities added.

This off course should not apply to the CSM part of the business as far as PI is concerned.

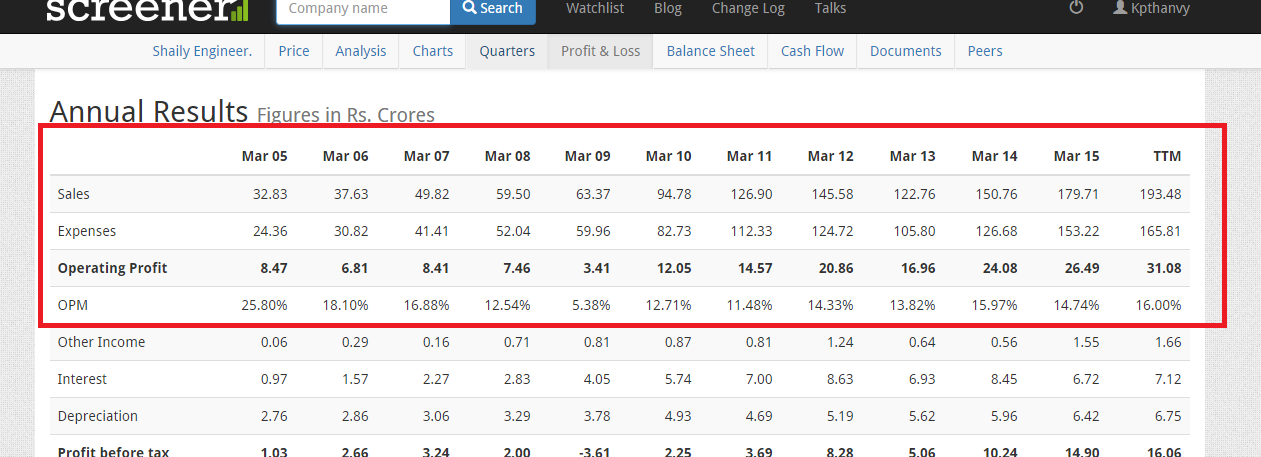

Shaily Engineering Plastic (22-09-2015)

@remonc Your question about competition:

In general my thought is, 'WHAT SHAILY MAKE WILL MAKE SHAILY ONLY" that is the way they are building up their relation with clients.

First of all we have to understand that Shaily is not a traditional plastic Moulding company. They are something unique in their approach. Shaily involved with their clients from the beginning such as Idea generation, product design, testing, Mold selection and till the end to finish the final product (In some cases for acquiring patents too). Very few companies in India providing that kind of complete solution to customers. It helps them to eliminate competition and will ensure them a long term contract with their clients.

Please check their last 10 years topline growth. Average 10 to 15% revenue growth for every year except one or 2 years. 32 crore from 2005 to 180 Crore in 2015.

Positive Biased always