@ Varun-POINT TAKEN

@satishrajan- The management in their latest concall clearly stated that the cash on books will

be used for acquisitions/inorganic growth. This to my view is a positive.

@ Varun-POINT TAKEN

@satishrajan- The management in their latest concall clearly stated that the cash on books will

be used for acquisitions/inorganic growth. This to my view is a positive.

I think one should check this post too

http://multibaggersindia.blogspot.com/2015/02/hairy-hairy-business-radix-industries.html

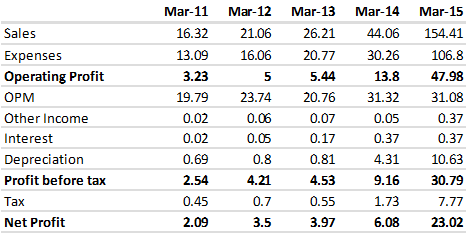

I want to write about 8k Miles Software

Market Cap 1500 Cr.

Debt 40 Cr.

PE 65, valuation is expensive,

Main Business

Providing Cloud Solutions to the Global Customers

Managing cloud applications for Global Customers with Global Partners like IBM,, Microsoft, CA Technologies etc.

Main Global Customers

MERCK, CISCO, Trimble, GSK, Adidas, Stanford University

Financials

Main Growth Factors

Companies are finding it easy to go for cloud , rather than investing in IT infrastrcuture.

For companies it is moving fixed cost in variable cost

Total Cloud market is expected to grow to US$ 282 billion ( Source Nasscom Gartner, 2015)

Explosion in Broadband and smart phone penetration with 3G and 4G services

How is 8k places

One of the early movers in the field

has global Customers

Experiences Promoters from the same field,

Disclaimer

I am not expert in the cloud field, so difficult for me to make a recommendation , however will request Value Pickr members to comment on this opportunity

Company has shown almost 10X growth in less than 5 years and still talk about the huge potential it has

Not invested , however planning to make small investment to start with

Sure. I will after 24th Sept.

@remonc, No one claim that Shaily is going to double their supply to IKEA. But one of the company may immensely benefit from IKEA entry in India should be Shaily Engineering because of their strong relations with each other. Apart from IKEA, shaily has many other areas to explore the opportunities.

Comparison about Supreme Industries: Supreme is world class company that we cannot compare to Shaily. (Even their product ranges are not matching). Then where we have to invest that is purely individuals calls after understanding the fundamentals and future opportunities of the firms. I feel Shaily made a strong foundation all ready, now it is time for grow up more faster than others.

@ankitgor44 Asian Paints recently announced plans for a new plant in Karnataka - is this likely to adopt IML heavily as indicated by you earlier? What revenues (and timelines thereof) do you foresee?

HMVL - As long as they do not have a clear cut vision for the cash in the books, the stock will continue to be mispriced. I hold it and it tests your patience. Companies holding huge amounts of cash can be difficult investments.

Bajaj Finance - could accumulate after yesterday's fall. It had run up too fast.

Generally a good selection.

@karan

Yes you are right as both the companies management has raised the concern on the future sales guidelines to flat or negative on YOY basis. But I think this good time to be contrarian and load up the stocks for the next rally when interest rates in India drop and economy starts reviving.

This two are only quality stocks with great management available in the reality space which are very less leveraged.

Poddar developers is better placed than ashiana housing owing to customer segment it addressed where there is most demand/supply mismatched.

Anticipating multibagger returns from this two companies in the future.

Disc : Invested in both the companies and together forms 5% of the portfolio

Thanks - can someone figure out how many sq. ft pokarna has sold last year - I am trying to triangulate the entire thing by looking at yield per sq.ft and RM cost per sq.ft and compare it with caeser stone and hopefully the results will give me more conviction either way.

Very Good price points in most of them. Look at either city union bank in today's fall or Shriram City union finance just in case you wish to switch over from karur Vyasa. I believe though I have rights to be proven wrong that DB corp is a much better business run by a very able management and in the right areas. Its valuations are on your side. Nalanda Capital - the most prolific investors I believe in India - I rate them over RJ have huge investments in it. Study it before buying HMV.

IT, Agrochemicals and consumer durables as sector should be there in every portfolio.