Very True..

But tht's the reason behind such healthy BS of CLSE

1...CLSE is doing Asset Light Business

2..ie...Procuring Rice from domestic market without setting up Rice mills and selling in International market at premium

3..CLSE clearly states they will spend on Marketing now own-words to improve brand Value of Maharani Rice ..Agree it can not be Compare with KRBL or LT foods

4..CLSE operating cashflow Fy 15 is 20 cr against -21 cr

5..Only play in CLSE is Low Valuation, Increase in Export,Opening in Iran Market,& Healthy BS

6..Dont expect returns like KRBL its altogether in different League

(Invested at much Lower Level)

Posts in category Value Pickr

CLSE – the next KRBL? (16-09-2015)

CLSE – the next KRBL? (16-09-2015)

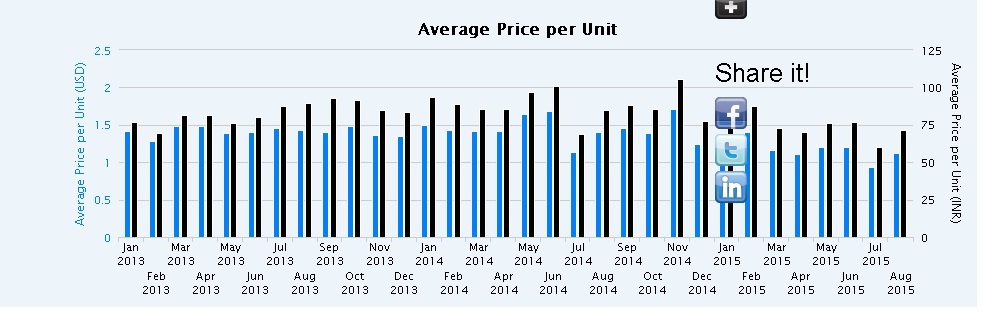

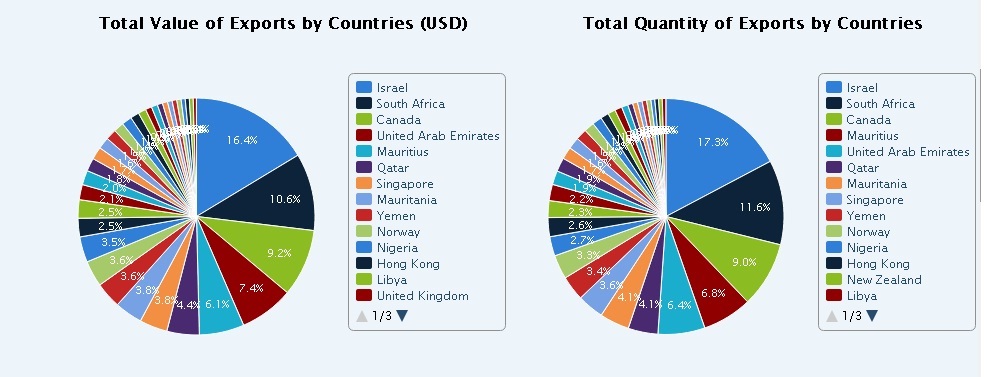

1..Chamanlal's Maharani Rice Export Data :-Showing Increasing Trend YoY

2..Chamanlal Increase its production (Not Capacity) by 35 v% in fy 15

3.Only Concern with CLSE is decrease in Realisation ie..per unit export price showing declining trend but it is compensated with increase in volume

4this is part of commodity business

(Dis:- Holding at much lower level)

POKARNA LTD ( Stock opportunities ) (16-09-2015)

Sure @Maheshcm - thanks would you know if their realizations are on par with caeser stone or higher/lower.

@sumi00 - I agree that they do not have publish full financials of subsidiaries - in this case, the subsidiary is material and is going to be growth driver. Another thing I am trying to understand is about lack of clarity on environmental, PCB clearances - quartz processing is a environmentally sensitive activity. When did they get these ?

Based on numbers, it looks a good story but I want to get to the bottom of what makes them tick.

Bayer cropscience (16-09-2015)

Key highlights of AGM by Capital Mkt

Higher sales of newer products together with increase in emphasis on exports has resulted in a 15% growth in net sales and higher operating margin for FY'15.Exports is hovering around 18%-20% of total sales and management expects it to remain around that level, given the emphasis of Parent on domestic market.

Crop protection business will remain a challenge for FY'16. Given a back to back bad monsoon and lower MSP prices have weaken the sentiments of rural India. While the company through new products and higher penetration will see a growth in FY'16, it will be an overall difficult year for the company and the industry as well.

Seeds business (about 16% of total sales) has continued to do well for the company and so is for the industry. Management expects the seeds business to further do well in FY'16, given lower penetration in the market for organized seeds in India.Some farmers are ready to pay premium for agro chemicals and fertilizers, but generally, a better monsoon and sentiment helps in doing the job of company in a much easier way than in a bad sentiment and overall challenging condition.

Varun 2020 portfolio – 2 strategies (16-09-2015)

Hi

After a long hiatus I am posting once again my portfolio for

everyone's review and comments. Have been in good spaces to get almost

150% unrealized gains on overall portfolio worth exceeding 40 lacs over

last 3.5 yrs.

From the last time I posted my portfolio there are few minor changes

a. Applied in Syngene IPO as I had Biocon - sold out at 350 completely as needed to raise cash to invest in better stories

b. Entered ITC and Bajaj Auto some time back as kind of nibbling in and then decided to get out. Reasons are I couldn't see myself invested in a company making cigarettes and causing cancer. Whats the point of earning money like this - My mother died of cancer. I switched over to Atul Auto from bajaj after a steep correction

c. Entered Supreme Industries, Care ratings and Axis bank as part of my core Portfolio which now constitutes 14 stocks - No stock exit from core portfolio

d. Yes I have 27 stocks overall in my 3 categories of portfolio but I guess its ok - as core portfolio provides stability and long term compounding and other two portfolios are more of multibagger types

My current Portfolios are as follows

Core Portfolio - forms 65-70% of overall holdings

1). Yes bank

2). Persistent systems

3). Alembic Pharma

4). DHFL

5). United spirits

6). Bayer crop Science

7). Lupin

8). Biocon

9). Marico

10). Rallis India

11). Glaxo Consumer

12). Axis Bank - New Addition

13). Supreme Industries - New Addition

14). Care Ratings - New Addition

Sub Core Portfolio

1). Agrotech

2). Vguard

3). HSIL

4).Tata Elxsi

5). Kaveri seeds

6). NRB Bearings

7). Atul Auto - New Addition

8). Aarti Drugs - New Addition

9). L&T Finance

Emerging Business Portflio as Wildcards - Less than 10% of my portfolio

1. Delta Corp

2. Lumax Auto

3. Gati

4. KPIT

Dynemic Products (16-09-2015)

There has been off-market purchases of late by promoters. Could it be that declassified promoters transferring their shares to existing promoters?

Forensics and the art of triangulation (16-09-2015)

Two broad concepts I wanted to share that I have found useful in thinking about these things:

Concept #1: Know the type of error you will be comfortable with.

Statisticians have a very useful concept of errors called Type 1 error and Type 2 error. It basically means you either err on the side of caution or on the side of aggression; a false negative or a false positive. Let us say you are not so sure about, after all analysis, whether management mis-appropriates funds that is generally expected to be minority shareholders'. You either drop the firm however cheap it may be or you go ahead with putting it in the consideration set. Now if it turns out that you dropped them and management was really "clean" then you have made a Type 1 error. If you give a green signal and you find they are mis-appropriating, then you are committing Type 2 error. Maybe you can ask yourself if you are OK with Type 1 error or Type 2 error. As for myself, in areas of integrity towards minority shareholders, I err on the side of extreme caution (or at least tell myself so  ) however cheap the stock maybe.

) however cheap the stock maybe.

Concept #2: Promoters' may be divided into 3 groups based on their "ethical nature". - this concept is raw in my mind but I find it useful to apply.

I find there are really 3 groups of people.

Group #1 are those who will wilfully violate the law irrespective of enforcement. They will not let law come in the way of their desires or ambitions. If an employee comes and tells them that this will violate this rule, the promoter will say, where is your value-add for the salary you take?

Group #2 are those who will violate the law depending how strongly or lightly it is enforced. To give you an idea recall many years ago a lot of employees were sacked at Intel in Bangalore because they 'fudged their LTC'. Now when I was an employee in a company considered highly ethical (about 22 years ago) I was just told to fill it up to get maximum tax benefit irrespective of whether I took a holiday or not. The general thinking was - this is strictly incorrect, but who looks. But once enforcement increases or at least the threat of enforcement, compliance goes up. So the moment Related Party Transactions need to be disclosed, Group #2 promoter will call up his finance guy and ask him how to manage while complying.

Group #3 are those who do not need any law to be ethical. They are by nature ethical and actively 'seek to know their duties and obligations'. They certainly err on the side of caution while interpreting the law in spirit and comply irrespective of costs. The real good news is that many such people exist, irrespective of whether they are rich or poor. An extract from a letter by Abraham Lincoln to his son's teacher captures this well: "..But teach him also that for every scoundrel there is a hero, that for every crooked politician, there is a dedicated leader." The bad news is that they may be running really poor businesses!

In my own assessment or rather theory, bulk of Indian promoters are in Group #2, some are in Group #1 and some in Group #3. In my view Group #3 is slimmer than Group #1. And more often than not our first impression of these promoters of which group they fall in turns out to be true.

Warm regards,

Syngene International IPO – Views invited (15-09-2015)

Thanks Mahesh for you response. I have read through 2014-15 AR and following are some observations/questions.

Top 3 criteria for selecting an outsourcing partner are - Quality, Consistency of Performance and Confidentiality. For first two points it becomes very important for company to hire right kind of people. The quality of research in India is rather poor and there is plagiaristic mindset. But there are some exceptional institutes in the field of chemistry as well (e.g. UDCT in Mumbai). So it would be great if we can get some insight into Syngene's hiring process + how is research culture inside the company?

AR mentions that company does business with Baxter, DuPont, Abbott and Bristol-Myers among others. And given that some of these are fierce competitors and confidentiality is a major factor in selection of outsourcing partner, what are the internal controls and practices of Syngene for these different clients? (Dedicated scientists per client? Some period if no-activity of a scientist is switching projects? How about people in senior management - can they manage two competitors? Risk of IP theft and trading by employees?)

AR mentions that total R&D expenditure of pharma companies was $139bn, out of which $105bn was outsourc-able.

The CRO discovery market is expected to grow from $14.7bn (2014) to $22.7bn (2018).

The CRO development market is expected to grow from $28.8bn to $44.6bn.

Given the discovery + development market size of $43bn worldwide in 2014 and Syngene's revenue of about $0.15bn (1$ = 60 Rs.) is rather minuscule, who are other large players in this space?

Another question is - what stops from big pharma companies (such as Bristol-myers) from setting up their own R&D centers in India (like Auto companies) instead of relying on external players?

Now some notes about balance sheet/technicals:

- The company has contingent liabilities of about 100Cr with Tax departments. If case goes against them, then it can be a short-term dampener on P & L and cash flows.

- All the directors of the company seem of foreign origin or foreign. So just curious to know what is the SEBI/RBI rule in this regard? Just a small technical detail.

Sorry for the long post. Looking forward for some good insights/discussions and learning.

Thanks,

Rupesh

My richdreamz portfolio – visit my portfolio to learn together! (15-09-2015)

Feeling a bit sad (  ) to see high quality stocks drift down a few points as the days pass by even though the broader market seems to have stabilised in a range.

) to see high quality stocks drift down a few points as the days pass by even though the broader market seems to have stabilised in a range.

Of course, I'm not doing anything stupid. I'm holding with my full conviction believing in "As long as the underlying businesses are growing, the stock prices will have to catch up like a Hutch dog, there is no other way - if not now, later".