Hi everyone, checkout my research on manorama industries, also on chocolate and CBE industry on youtube, spoiler → its a long video. (right click on the link and open it in a new tab, for some reason that is how it is working)

https://www.youtube.com/watch?v=PCvvaxSmc_k&t=2409s

Posts in category Value Pickr

Manorama Industries: Creating Wealth from Waste (25-08-2024)

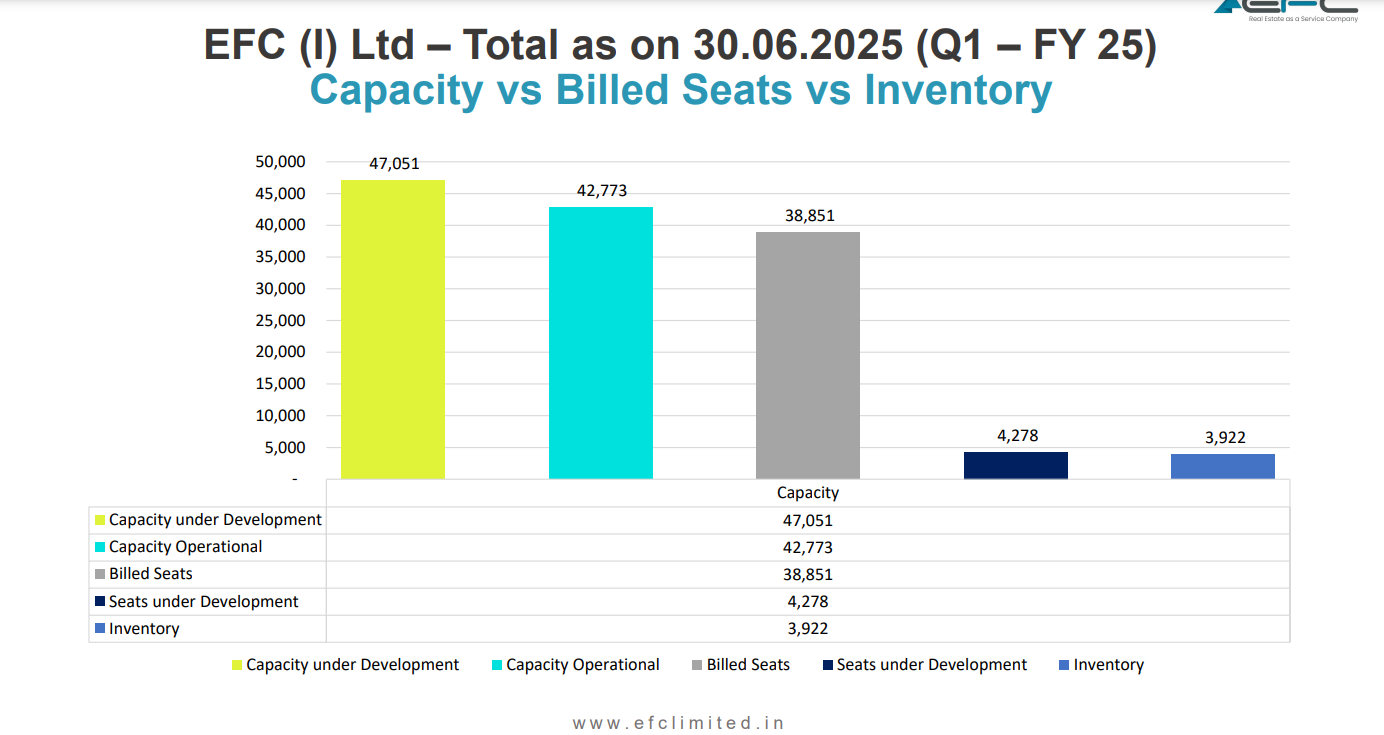

EFC – Entrepreneurial Facilitation Centre (25-08-2024)

Q1FY25 Concall Highlights:

Financial Performance:

- Consolidated Revenue: INR 105.28 Crores, up 82% YoY

- EBITDA: INR 49.62 Crores, blended margins of 45%.

- Profit After Tax: INR 15.77 Crores. More than 5X as compared to Q1FY24

- Rental Segment Revenue: INR 66.79 Crores (63.44% of total revenue)

- Design & Build Turnkey Contracting Segment Revenue: INR 35.30 Crores (36.56% of total revenue)

Operational Performance:

Managed Office Business:

- Increased leasehold area by 300,000 sq ft across 7 centers in 4 existing cities.

- Added 7,000+ seats, bringing total seating capacity to over 47,000. By the end of this year, company will easily be around 65,000-70,000 seats.

- Acquired 80,000+ sq ft property in Pune for development and leasing.

Design & Build Division:

- Secured contracts exceeding INR 75 Crores across various sectors.

- Completed a 100,000 sq ft project for Coforge in 62 days.

- Currently negotiating contracts valued at over INR 100 Crores.

Furniture Manufacturing Segment:

- Secured regulatory approvals for a new manufacturing facility in Pune.

- Workforce of 200+ people.

- Production trials to commence in August 2024, with commercial production starting in September 2024.

- As per management, one simply cannot just bring capital and starts manufacturing of furniture, thorough understanding is required along with right blend of team.

Future Outlook:

- Target to double topline by FY25, with blended EBITDA Margins of 30%.

- Management sounds confident and ready for the next 3 years.

- Managed Office Business: Aiming to add 30,000-40,000 seats annually for the next three years.

- Design & Build Division: Confident in achieving year-on-year doubling of revenue.

- Furniture Manufacturing Segment: Projected to achieve INR 250-300 Crore topline by FY26. Commercial production is set to be launched by September 2024.

- This year, company is expecting INR 50-75 Crores contribution in topline from the furniture segment.

Other Important Points:

- REIT: Incorporated a real estate investment trust (REIT) with a corpus of Rs. 499 Crores. By the end of this month or beginning of September, EFC should get approval for the registration of their REIT.

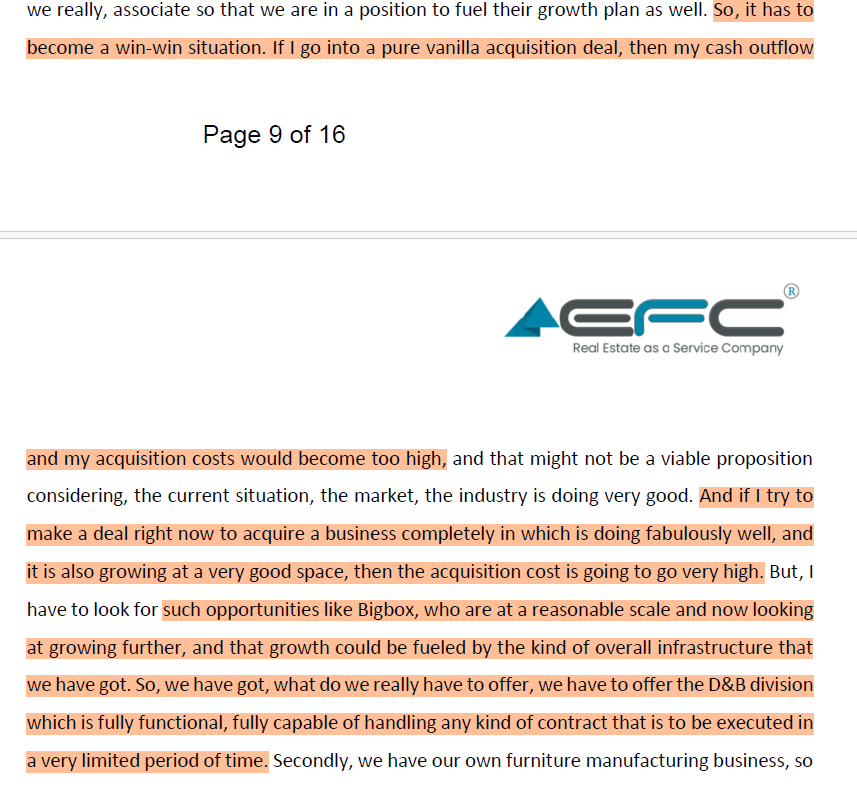

- Inorganic Growth: Focusing on strategic acquisitions like Big Box.

- Competitive Landscape: Acknowledged increasing competition but believes in their integrated business model and pan-India presence.

- Acquired a 51% stake in Big Box Venture Private Limited. Big Box was already doing INR 2 Crores topline per month, with about 2800-2900 seats and since acquisition BB has added 2000 more seats.

- Bigbox Venture, has an impressive portfolio of over 3000 seats in Pune, is aggressively expanding into NCR region, Ahmedabad and Kolkata, significantly enhancing EFC overall market presence.

- The Pune acquired property will be used for managed office space only.

- As of now, focusing on nine prominent cities only ( NCR region, Bangalore, Hyderabad, Chennai, Gujarat, Ahmedabad, Bombay, Pune and Kolkata ), but going ahead EFC is also looking to expand in other cities as well, where certain developments are happening like Indore, Coimbatore and Chandigarh.

- One Instance shared by management:

- Management admitted that inorganic growth is necessary for any company in this space.

- Management on Acquisition Strategy:

- Management admitted that this space has no entry barrier, but to get to that efficiency level at which everybody like EFC is operating, that’s not going to be very easy for every new entrant and also to become a significant player.

- All the seats which are getting developed might not get occupied immediately, because there is a lag between the development and the occupation.

Concerns:

- Management was hesitant to answer some questions regarding TCC Concept RPT with EFC.

- The competitive intensity is increasing in this sector, which needs to be watched out.

KPI Green- Turning Sunshine Into Cashflows (25-08-2024)

FCF is sum of cash flow from operating activities and investing activities which tells how much money the company needs to raise to sustain its normal operations/ growth plans (generally -ve in growth companies)

This money is raised through debt or issuing equity which can be seen under financing activities.

Investing journey of an imperfect investor (25-08-2024)

My small portfolio as of today with allocation and thesis ![]()

Macpower CNC- Manufacturing is the buzz word and CNC machines are needed. Macpower has been the heaviest bet in my portfolio. In hindsight valuations can seem to be very rich but here I’m okay to add as much as I can. I’m willing to go wrong here. My thesis is- Excellent Promotor, Operational Excellence, No debt, Prudent Capital allocator. It’s silly to be in love with a company and I might look like a fool if this doesn’t deliver what I’m anticipating. But when the promotor even at industry best margins and asset turns talks about excelling further with growth and he has clarity when he gives a reason, it’s worth taking a shot. 35% allocation in Portfolio

Shilchar Technologies- Transformers transformers all around and a lot of companies to pick. I personally feel that this one is taking a pause before going ballistic again. The management has done a capex with internal accruals and if one does the maths, even if it’s a transformers company, their margins are to be envied. **Personally don’t like their limited interactions with the investors **. But my average investment price gives me a cushion to take a pause and reflect if things go awry. 20% allocation in portfolio

Jash Engineering- Water is the new Gold and all likely it’s going to remain so. I feel here the TAM for the company is huge as alluded in their concalls. They are at the cusp of what they can deliver. Exports form a major chunk and they have established themselves in key geographies. They don’t need to go all over the world and yes, India is still not even in the frame as far as the potential is concerned. There might be a lot of business coming from here. The management has recently announced a split as well. Maybe they’d like more people to be a part of this journey ![]() 10% allocation in Portfolio

10% allocation in Portfolio

Windlas Biotech- Now Pharma is not my cup of tea but you don’t need to be a rocket scientist to understand a a management. This is one instance wherein I’m separately banking on their three different business verticals. I have my bet on the promotors as well. They have groomed their CFO to become the CEO. Not many have the courage and heart to do in small companies. I feel with the Pharma cycle they’ll do well. And yes being a small company they did a buy back too. Talk about capital allocation ![]() **10% of portfolio **

**10% of portfolio **

Ethos- We will grow, our aspirations will grow, our hectic lifestyles will push us to get luxuries to keep going. When it comes to watches who better than Ethos. Retail businesses are expensive but what sets ethos apart is that to crack this business there are many many hidden barriers to entry. Trust, assortment, service and experience. They are top notch. 10% of portfolio

HBL power- There’s been enough written about this by the stalwarts. Safety is going to be a big push. I think I’ve been one of the late entrants but nevertheless technically as well I feel it’s poised for a long journey ahead. 5% of portfolio

Techno electric- Have trimmed this down a bit as I feel it’s run up quite a bit though I have full faith in the management commentary as well as how data centre business will shape up for them.**5% of portfolio **

Frontier springs- Riding this as a railway theme small cap company. Plus their capex and management guidance of 500 Cr gross revenue means that a sharp run up might be ahead. **3% of portfolio **

Have a little bit here and there in a few watchlist stocks. Sometimes I just buy a token quantity to test if I’ve been able to technically gauge how stocks are moving.

My long term goal is to use techno funda and I feel that in techno I still need to learn a lot of funda ![]()

Smallcap momentum portfolio (25-08-2024)

Chola , DOMS and Godfrey are in the list. However note says they can’t get in?

Thanks.

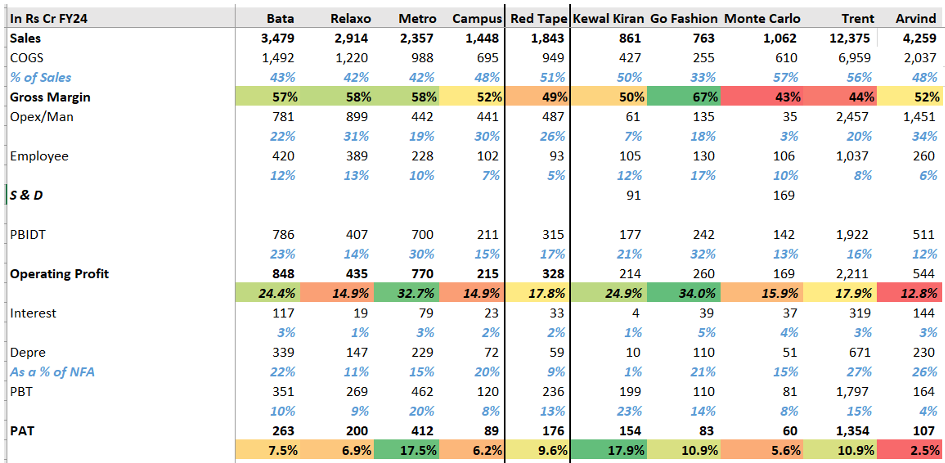

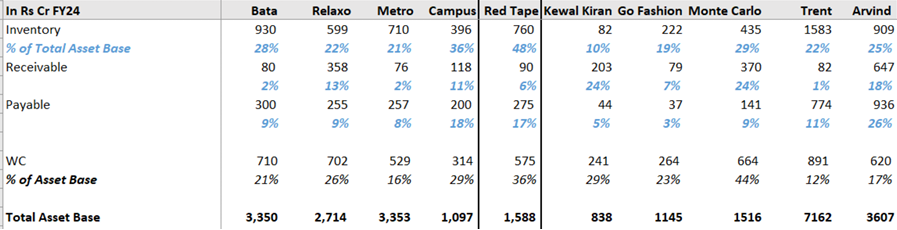

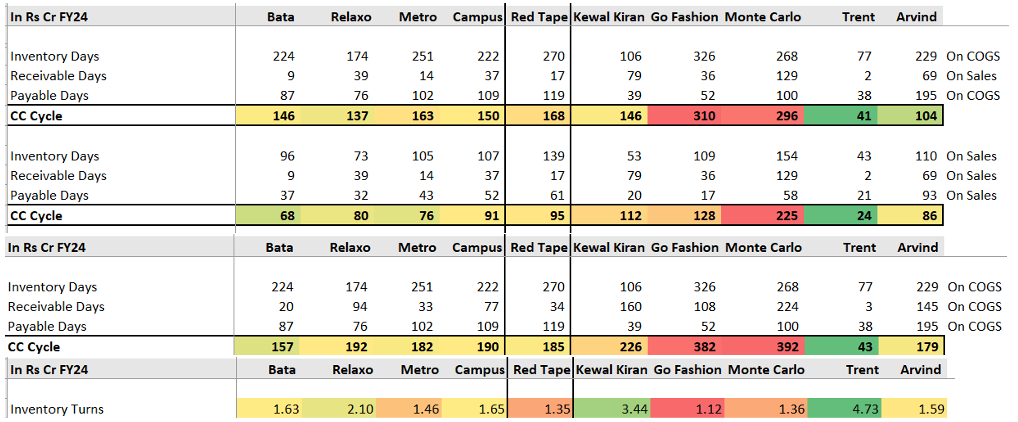

Red Tape Ltd. – The next fashion giant? (25-08-2024)

As disclosures are very less for the company, tried comparing financials to understand better

In terms of YoY growth, red tape stood out post trent

WC as a % of total assets is one of the highest for Red Tape, after monte carlo

Working Capital Days breakup is as follows – taken on basis – different denominators. Trent has best in class WC days and inventory turns

Cash Flow conversion for red tape is poor

Z-Tech India- a monopoly in sustainable theme park? (25-08-2024)

Sustainable theme park business:

- existing 6; upcoming 10 [revenue contribution : 60-65%]

- only player

- PAT: 20%+

- strong H2 due to rains in H1

- business model: EPC revenue; revenue sharing with Govt [ticket, F&B, shop rental, adventure activity, retail]

- 80-90% parks- revenue sharing मॉडल

- 20 years contract [investment is recovered in 1-1.5 years]

- Building sports park in UP [upcoming games like pickleball which is a rave in US]

25% margins in waster water management- sustainable [Mazda- compete]

Vision of the co- sustainability [sustainable parks, waste water management] & geotechnical business [designs & constructs infrastructure such as flood protection systems or river embankment systems]

Triggers:

- upcoming 10 theme parks [starting oct to march- each month one park would open]

- 20 tenders for theme parks [to win majority- by dec’24]

Industry triggers [theme park]:

- Typical theme park costs 20 times more than sustainable theme park

- Govt pay back period < 1 year [eg. waster to wonder Delhi park]

- Ticket is barely Rs 100 vs Rs 1000 for typical theme park

- States / municipalities get better swachchh rating if they do waster to art [soft trigger]

Guidance:

Revenue FY 25: 120 cr [vs 67 cr in FY’24]

PAT FY’25: 20 cr [vs 8 cr FY’24]

FY’26 [soft guidance]: follow growth of FY’25 [but min 50-60% growth]

order book [end of FY’25]- 200 Cr+

To be monitored:

- Optionality:ad revenue in park

- size of TAM for theme park

- International expansion to increase TAM [higher margin]- H2 FY’25 strategic team to be in place

- Parks won on revenue sharing model

- Govt receivables

Disc: Invested

Microcap momentum portfolio (25-08-2024)

@9916673623 you can keep the code in GitHub repository for open use

Microcap momentum portfolio (25-08-2024)

@9916673623

Sir,

How are you handling the stocks listed in less than 126 days.

I am using bfill() but facing issues in log returns and final z scores.

LM Portfolio and Information Attic (25-08-2024)

Hi all,

I am in my late 20s. I started investing in May 2021 at the peak of crypto mania to make quick money by investing in Bitcoin and Dogecoin (learnt some valuable lessons). Since then, I have been investing primarily in Indian stock markets (90%) with some exposure to US stock markets (10%). Initially, I started with coffee can approach (burnt my hands) then transitioned to an approach with diversified PF of reasonably valued stocks. I typically screen stocks from SOIC, Wealth Insight magazine, various blogs and of course by manual screening of fundamentally strong stocks and stocks in Stage 2 tool of @Tar. The XIRR with the latter approach has been decent in last two years.

Here is my current Indian PF:

| Stock Name | Current PF weight | Average Buy Price |

|---|---|---|

| All E Technologies | 9.00% | 290.96 |

| Varun Beverages | 5.87% | 713.48 |

| Senco Gold | 5.40% | 787.43 |

| Samhi Hotels | 5.19% | 193.20 |

| Interglobe Aviation | 5.01% | 2,991.83 |

| Narayana Hrudayalay | 4.85% | 1,066.09 |

| Godawari Power & Isp | 4.39% | 784.45 |

| Polycab India | 4.18% | 4,830.47 |

| Prestige EstatesProj | 4.15% | 1,270.41 |

| Equitas Small Fin. | 4.10% | 90.45 |

| Glenmark Pharma | 3.76% | 1,031.34 |

| Zaggle Prepaid Ocean | 3.65% | 324.09 |

| Kama Holdings | 3.54% | 2,634.57 |

| Nuvama Wealth | 3.52% | 3,984.48 |

| Tejas Networks | 3.19% | 1,089.68 |

| KEI Industries | 3.15% | 1,870.84 |

| Info Edge | 3.11% | 4,748.57 |

| Multi Commodity Exch | 3.01% | 3,100.91 |

| Aditya Vision | 3.00% | 2,238.49 |

| Medi Assist Health | 2.82% | 524.03 |

| Deepak Fert & Petro | 2.65% | 959.83 |

| Pennar Industries | 2.61% | 149.27 |

| GMM Pfaudler | 1.70% | 1,512.14 |

| Vadilal Industries | 1.53% | 3,690.56 |

| Arman Financial Serv | 1.46% | 2,141.64 |

| One97 Communications | 1.34% | 415.19 |

| J Kumar Infraproject | 1.16% | 850.52 |

| Tarsons Products | 1.14% | 483.85 |

| Laurus Labs | 1.10% | 430.34 |

I own 29 stocks at the moment. While this number is on the higher side, I play a basket approach in some sectors (Polycab + KEI) and stocks with less than 2% weight are tracking positions. I will be outlining the thesis/anti-thesis of top 10 stocks going forward.

| Stock Name | Current PF weight | Average Buy Price |

|---|---|---|

| Tesla | 36% | 168.79 |

| Evolution AB | 25% | 111.34 |

| Ark Genomics | 13% | 24.17 |

| Amazon | 12% | 165.59 |

| Inmode | 12% | 19.49 |

| Zapata Computing | 2% | 0.5171 |

I won’t be adding incrementally to the US PF as the performance over past three years has been abysmal. I can’t use my framework that I use for Indian Stock Markets due to higher volatility and lack of resources/conviction for US stocks.

Here is my investing philosophy:

- I typically start with 4% allocation. 6% allocation if I am convinced and valuation is good (AllETec as an example).

- I don’t average down if the business is going through headwinds. I learnt this lesson the hard way. I kept averaging down when Laurus Labs was going through price erosion in ARV prices. I made GMM Pfaudler my highest weight by average down. I have since then learnt this lesson as opportunity cost was massive.

- I typically start tracking positions with 1-2% allocation when I am still studying the business or if the business is in headwinds. I ramp up the position once I see fundamental triggers or triggers on charts.

- I only use two technical indicators: Weekly EMAs (10, 30, 40 week) and Relative Strength(RS) with respect to Nifty 500. I cut the position sizing when I see the stock is moving below 10 WEMA and RS declining. I am extra cautious when stock is below 30 and 40 WEMA. I bring down the weight to 1% if the stock is below 30 and 40 WEMA.

I will try to crystallize my thoughts and add more points later.

Here is why I started this thread:

- In the recent months, the churn rate has been high out of anxiety. I want to use this platform to be more accountable for my decisions.

- Dump and organize lessons and information I gather from various sources. Lately, I have been cluttering my mind with useless information. I hope by this activity, I can be more selective about my consumption going forward.