I first did back testing of the stocks which were in my portfolio at the initial stage of my stock market journey (2017-18). Like Reliance, Tech Mahindra, UTI AMC, Voltas, Ashok Leyland, BSE, LT etc. Later I backtested most of the ETFs and then Nifty 50 and Nifty 150.

Posts in category Value Pickr

Samhi Hotels – Turnaround with Tailwinds (24-08-2024)

BTW, I hold Thomas cook as well in my long term core portfolio apart from SAmhi.

PGINVIT impairment of investments in subsidiaries and book value (24-08-2024)

On that note, this could be a positive news as PGINVIT now has a new CEO:

https://www.pginvit.in/uploads/7de9a137-afda-422d-b380-10ada36ffeaf/INTIMATION.pdf

The new CEO, Smt Neela Das seems to be having 32 years of work experience at Powergrid.

Fingers crossed. I hope this could be the turning point for PGINVIT.

Ceinsys Tech-Engineering, Geospatial & IT solutions Company (24-08-2024)

IMO among two verticals, GIS is what it is and the other one is everything else. If we try hard, we can imagine all kinds of synergies between GIS and stuff in “everything else”. In reality, it may not make a huge difference. Even if it does, one should not give any weight to it in the valuation exercise. At least for now.

From ER&D to data centre consultation, they are perhaps trying to incubate some ideas for potential future verticals.

In ten years it may start looking like any other IT service company (minus BFSI et al) where Geo has highest weightage but has few other streams.

If I were to question one thing, it would be does company has a clear mission other than “dekhi jayegi”.

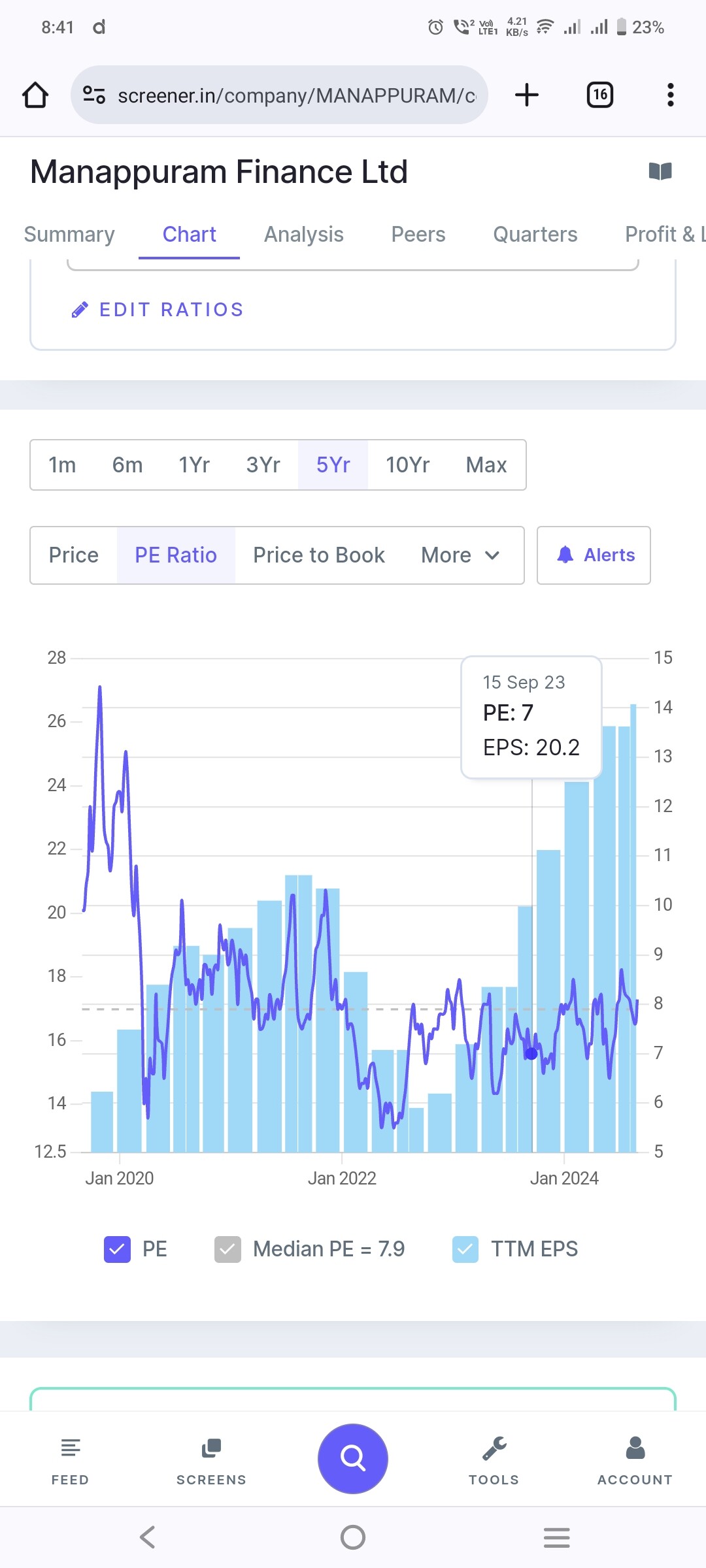

Manappuram Finance (24-08-2024)

How can a share price crash make the p/e high?

On the contrary p/e should also have crashed as p is the numerator and as a result directly proportional to p/e.

Also I don’t see Nov 2022 PE greater than Oct 2020 PE as per screener.

What we see is, share price crashed in line with EPS crash and PE remained same or actually reduced from oct 2020 to nov 2022.

Manappuram Finance (24-08-2024)

How can a share price crash make the p/e high?

On the contrary p/e should also have crashed as p is the numerator and as a result directly proportional to p/e.

Also I don’t see Nov 2022 PE greater than Oct 2020 PE as per screener.

What we see is, share price crashed in line with EPS crash and PE remained same or actually reduced from oct 2020 to nov 2022.

RACL Geartech Limited (24-08-2024)

RACL Geartech Q1FY25 concall summary –

- Management internally set sales target of 125cr but they able to achieve only 100cr

- H2FY25 sales will be 20-25% higher than H1FY25

- FY25 sales target of 550cr has been reduced but at what extend, it has not been decided yet.

- Capex will reduce for FY25

- Management now seeing 18-20% growth as compared to fy24

- Focusing on reducing debt so interest cost could not affect P&L much.

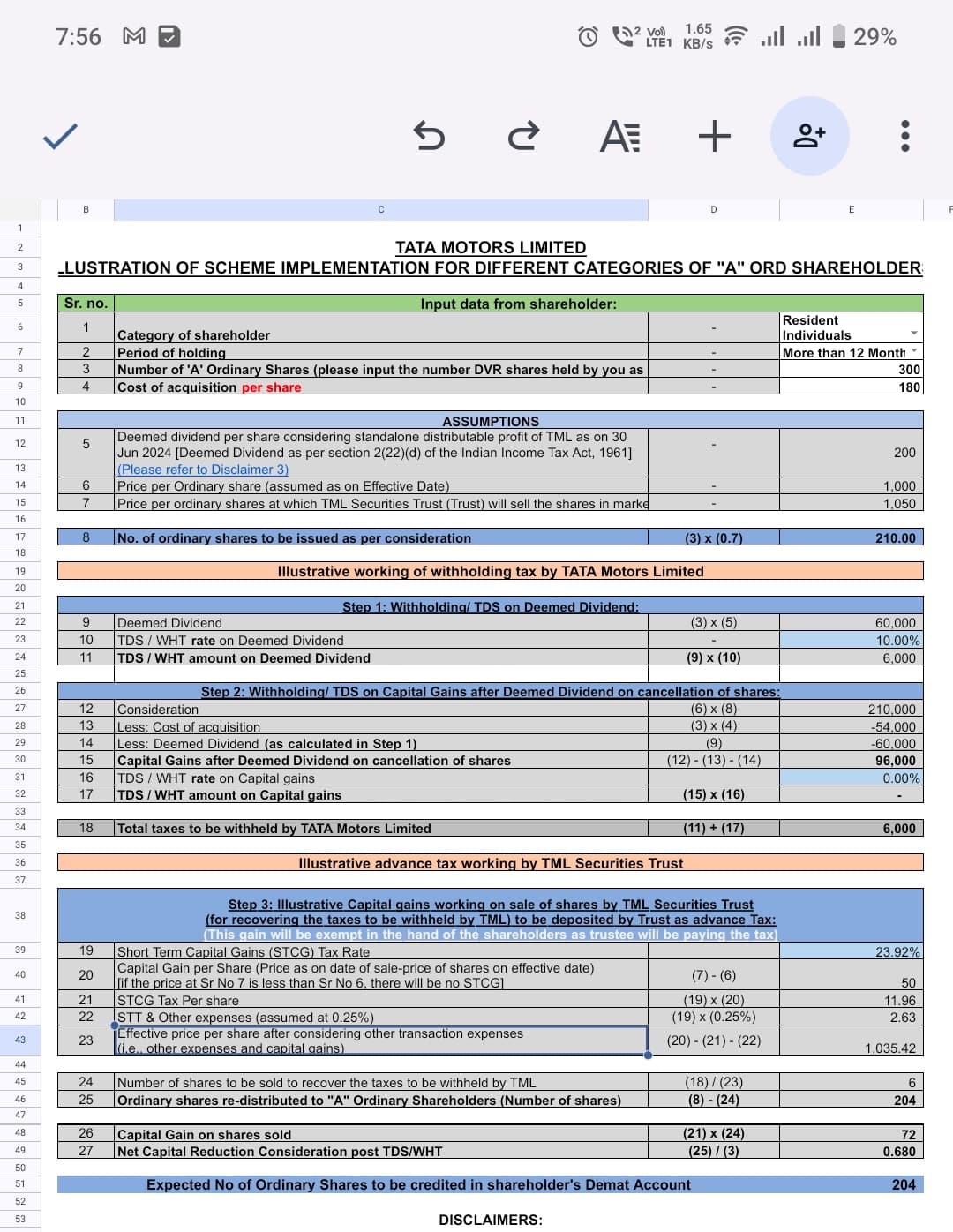

Tata Motors – DVR (24-08-2024)

Thanks for the Excel sheet.

I have put my holdings of 300 dvr shares at cost of acquisition 180 per share, all ltcg and bought after grandfathering.

I see there’s dividend withholding of 6000 TDS at 10% rate. I’m in 35% tax bracket so I have to pay 21k in total as tax.

The Excel sheet doesn’t consider shareholders other ltcg (if he has already crossed the 1 or 1.25 lakh limit).

The conversion factor of just 0.7 looks like short changing the dvr holders. I don’t see any advantage in converting the shares to ordinary shares compared to sell dvr and buy tata motors ordinary shares. It will be helpful if anyone can look at my case and say if I should convert or just sell now itself.

Is the company issuing new ordinary shares to compensate for dvr shareholders? If so, then free float is not going to reduce and eps will remain the same. No big advantage for dvr-converting and existing ordinary shareholders as well.

Sona Comstar BLW – Direct EV Play (24-08-2024)

Hello Community,

I’d like to share some key insights from the Annual Report 2024, Q1 FY25 Results, and the recent AGM:

Global Presence: The company operates with 10 manufacturing facilities, 4 R&D centers, 3 engineering capability centers, 1 tool & die shop, 8 warehouses, and over 4,600 employees across the USA, Europe (Germany, Mexico, Belgium, Serbia), China, and India.

Product Development: Out of 18 products, 6 are still under development.

Working Capital Lenders: HDFC, SBI, CITI, and Yes Bank are represented as working capital lenders.

IP Achievements: The company filed 11 patents and 10 design applications and was granted registration for 13 patents and 15 designs during the year.

Order Book: The total net order book stands at ₹23,300 crore after consuming ₹400 crore in Q1 FY25 and adding ₹1,100 crore in new orders. This represents 7.3x FY24 revenue.

Revenue Distribution: As of Q1 FY25, 33% of product revenues come from the battery electric vehicle (BEV) segment, with 72% of sales directed to international markets. North America accounts for 43% of total sales.

Growth in BEV Revenue: While the company has a diversified revenue base across geographies, products, vehicle segments, and customers, the growing share of BEV revenue remains a dominant theme.

Decline in ICE Revenue: Revenue from internal combustion engine (ICE) products has shrunk to 9%.

Revenue Composition: 33% of revenue comes from BEV, 21% from hybrids, and 37% from power source-agnostic products.

New Business Wins: The company secured its first product order for its Sensors and Software business, which will be executed by NOVELIC. Additionally, more products were added to an existing Driveline order. This quarter, the company added one new customer and one new program in Asia.

EV Programs: Currently, there are 55 EV programs across 31 customers, with 27 in production, 12 fully ramped up, and 15 in various stages of ramp-up. Another 28 programs are slated to start production over the next few years.

New Commercialized Products: In Q1, the company launched two products: In-cabin Sensors (ACAM: a critical safety feature to detect the presence of a child in the vehicle) and Park Gear (enhancing the safety and reliability of commercial EVs).

Future Product Additions: Two new products were added to the technology roadmap: an Integrated HV Motor Controller, which improves thermal management and reduces energy losses, and an Integrated Hub Motor Controller, which combines the controller and motor to reduce weight and wiring complexity, enhancing system reliability for compact and lightweight EVs.

Upcoming Developments: The company plans to introduce low-voltage and high-power-density motor solutions between CY24 and CY25.

PLI Benefits: Four products have been approved for Production-Linked Incentive (PLI) benefits, with revenue recognition starting in the next financial year.

Board Composition: No significant concerns were identified regarding board composition or related party transactions. Meeting attendance is strong, and board member salaries align with industry standards and regulations. The company does not have any material subsidiaries.

Subsidiary Support: The company has provided a letter of undertaking to its subsidiary, Comstar Automotive Hong Kong Limited, to offer financial support as needed from April 1, 2024, to March 31, 2025.

Legal Matters: Labor cases are pending before the High Court and the Labor Commissioner. Legal advice indicates these cases are unsustainable, and no provisions have been made. No monetary claims are pending.

Contingent Liabilities: The total disputed amount is ₹99.48 million (31st March 2023: ₹85.88 million), with ₹8.63 million already provided for, and the remaining amount disclosed as a contingent liability.

Warranty Provision: At the consolidated level, the warranty provision increased to ₹45.12 million from ₹20.04 million in the previous year. I’m unclear if this increase is due to higher sales or changes in customer contracts, but the amount remains small compared to the company’s overall revenues.

Overall, this is a solid business with capable management. However, the company is facing softened growth in the European market. Rising commodity prices, high interest rates, and increased fuel costs may act as headwinds.

Disclaimer: I am invested with a tracking portion and may accumulate on dips, so biased.

Kalpesh’s Portfolio (24-08-2024)

Bond portfolio 31%

Equity+cash portfolio 69%

At 9-10% interest income from bonds is more than enough for yearly expenses of my family.

Bonds provides me emotional comfort to be cool & calm in market drawdowns.