Posts in category All News

Nadda terms Congress ‘parasite party’, says it weakens alliance partners (19-07-2024)

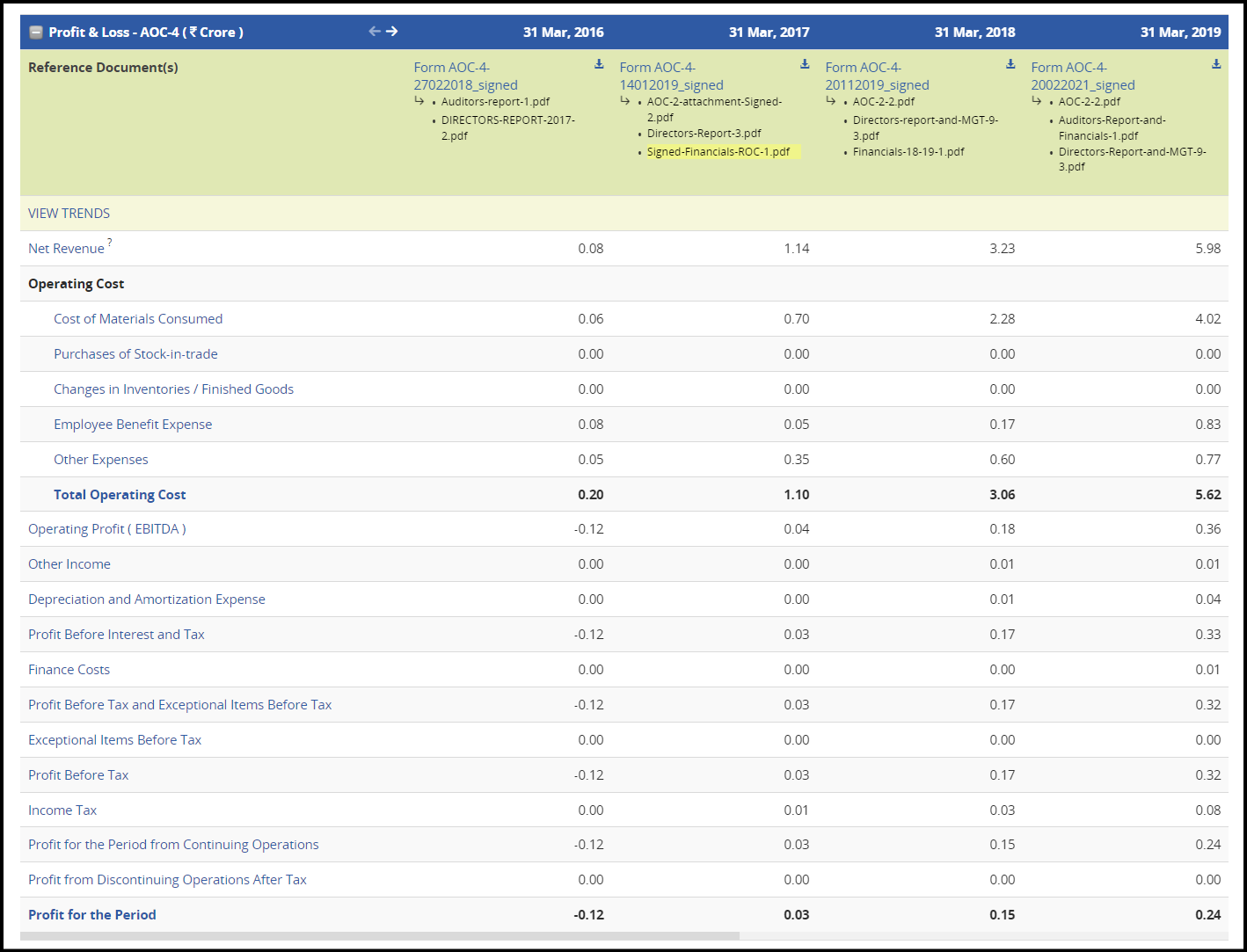

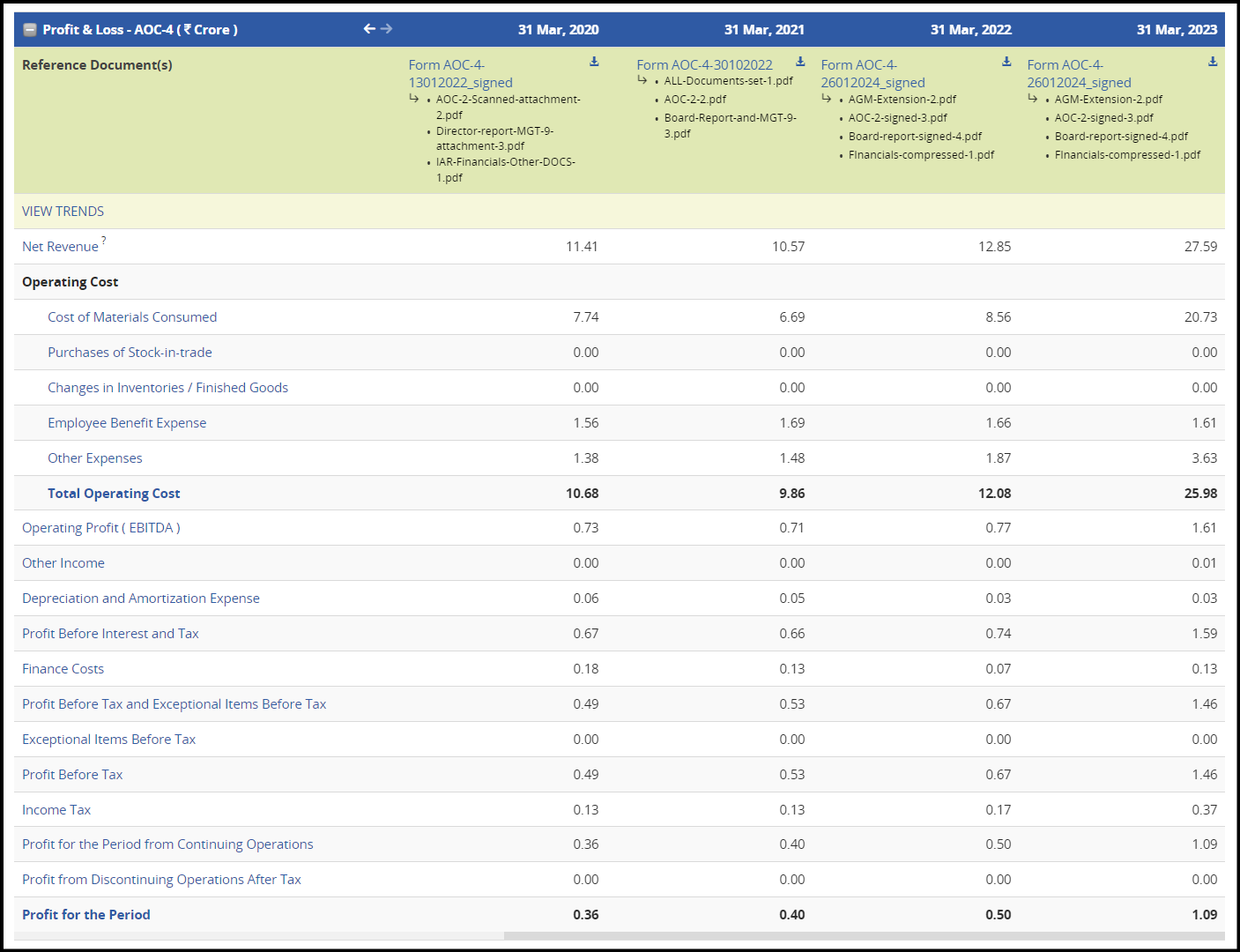

DCX Systems Ltd (19-07-2024)

There has been a decrease in promoter, FII and DII shareholdings. Promoter have sold 12% holdings in last six months. Not a good sign. In concalls they are very confident about future business but here it shows different. ![]()

Gravita India success story (19-07-2024)

Read the article… please pardon me for my ignorance…

Can any seniors explain how this thing going to affect business strength of Gravita?

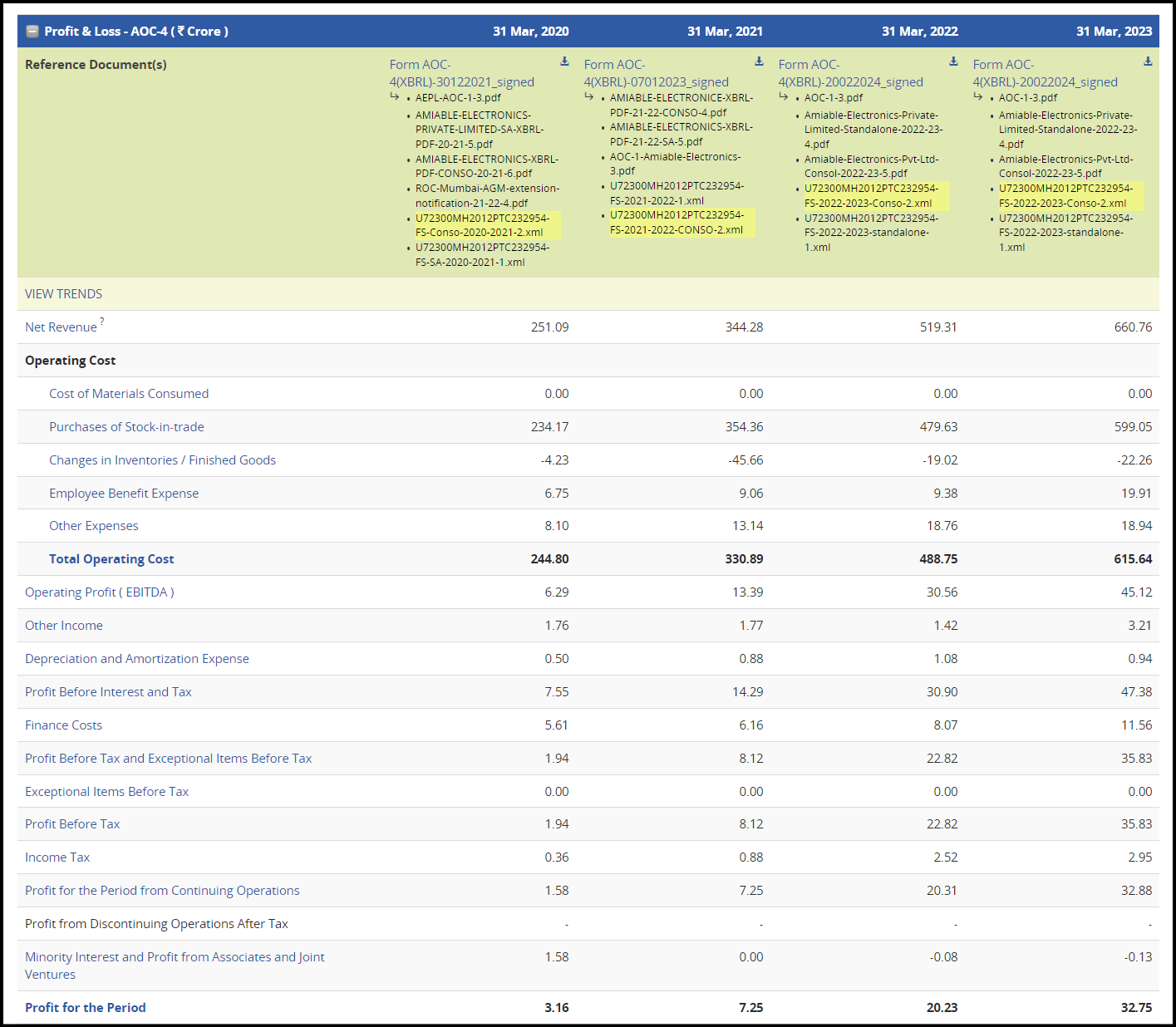

NewJaisa Technologies: A D2C Refurbished Electronics Play (19-07-2024)

Competitor Financials

Electronics Bazaar

-

Have scaled revenues from 250 Cr. in FY20 to 660 in FY23.

-

Business is almost entirely trading. Generates <10% EBITDA margins.

-

Employee expense is only 3% of revenues.

-

30 Cr. PAT in FY23, around 5% PAT margins.

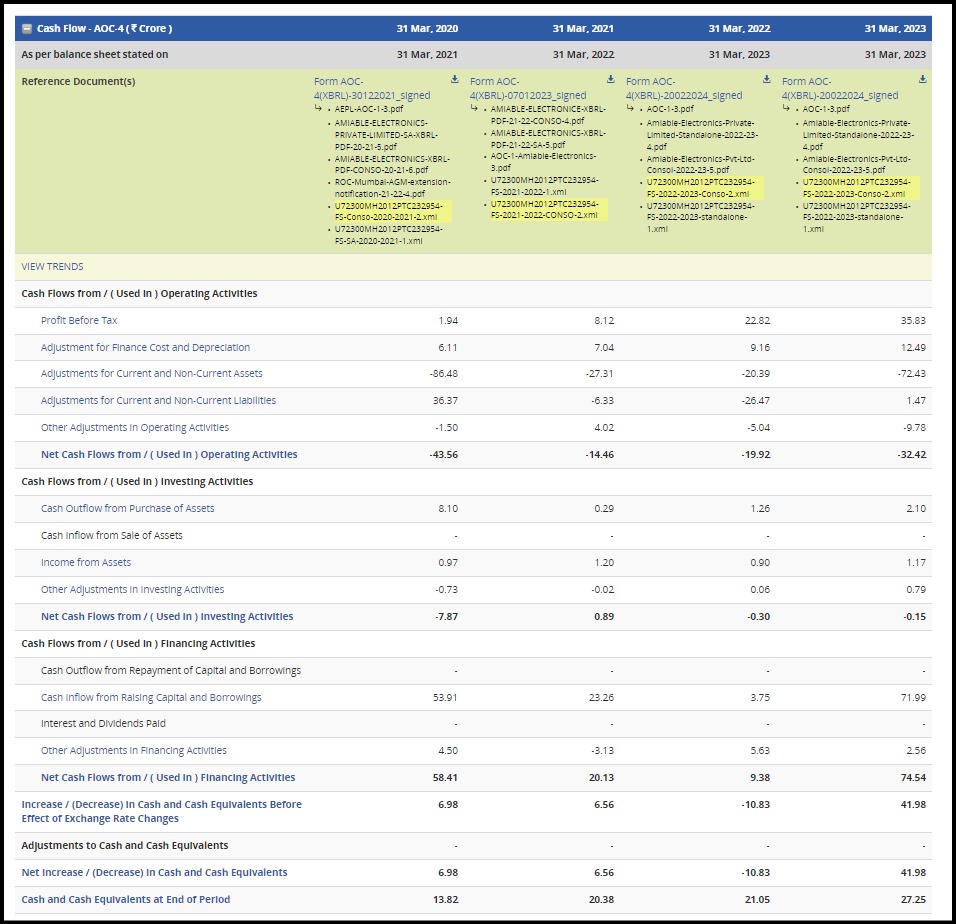

- Negative cash flows despite posting profits.

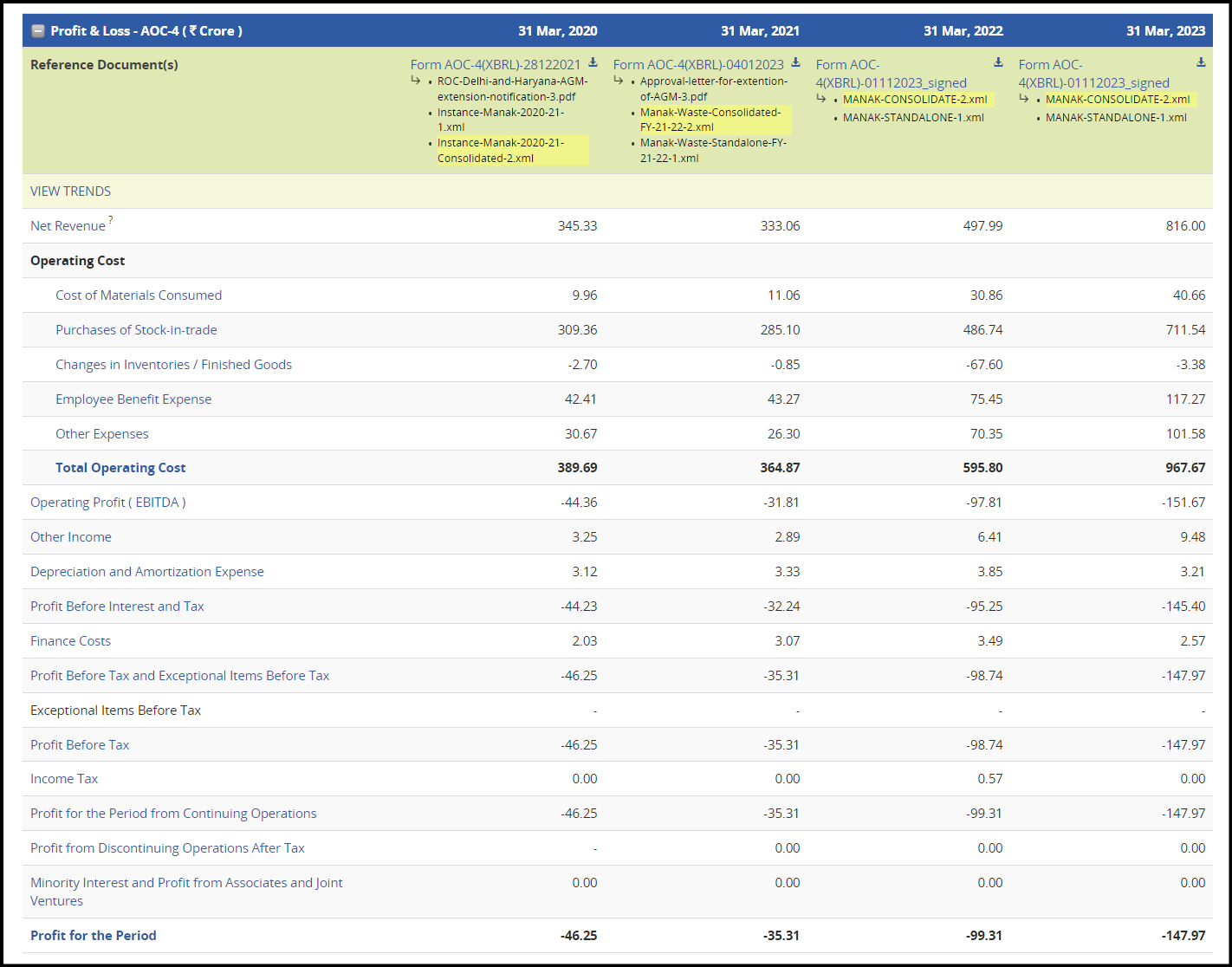

Cashify

-

Cashify sells refurbished phones + other electronics on top of laptops. Not a perfect peer.

-

Scaled revenues from 350 Cr. in FY20 to 800 Cr. in FY23

-

Employee cost is very high given the trading business. Other expenses are equally high.

-

Could have been profitable save for these two line items.

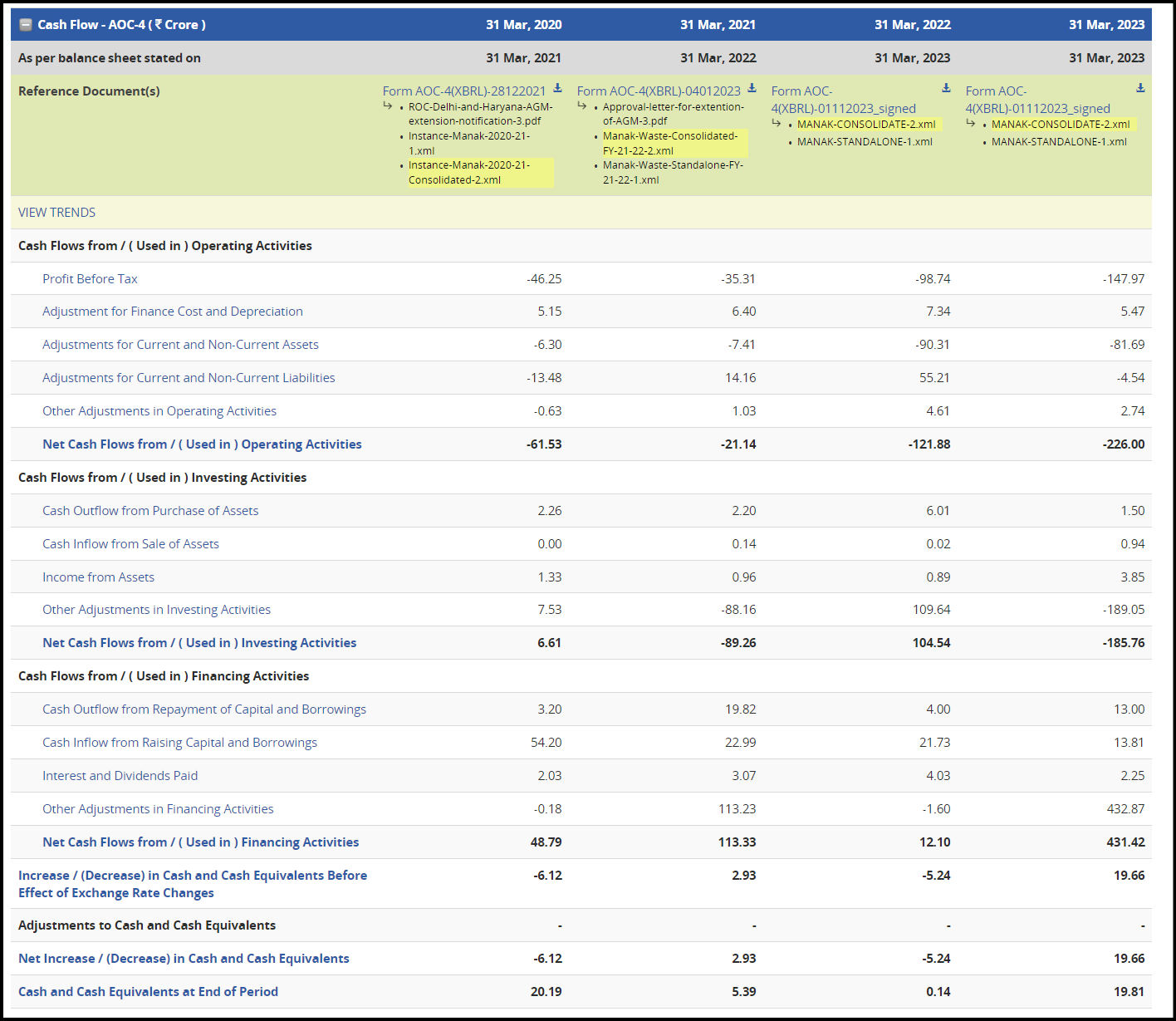

- Cash flows are equally shady with several adjustments. I wouldn’t go anywhere near this business.

Salori e-Commerce

-

Scaled to 5 Cr. in the first four years of operations, 30 Cr. at the end of 8 years.

-

24% gross margins in FY23.

-

5% EBITDA margins, 4% PAT margins.

-

Looking at these companies, no one seems to be doing any serious refurbishment work (reflected in low gross margins and high trading line items). Management’s claim of competitors being traders looks to be true.

-

This should put to bed any questions about Salori e-Commerce. New Jaisa has scaled to 60 Cr. of revenue in four years, with 47% gross margins compared to 24% for Salori.

-

Electronics Bazaar and Cashify seem to have lots of scale despite poor unit economics. With eventual forays into adjacent kinds of laptops and eventually cell phones, I would expect New Jaisa to eventually reach EB’s scale of 500+ Cr. of revenue.

Wockhardt: an NiCE story (19-07-2024)

I agree. I heard a similar point of view from someone who is familiar with the industry. His broader point was that several optionalities could emerge. This includes the possibility of Zaynich itself having positive effects beyond what was originally envisaged. His view was that clearing Phase 3 was the big hurdle, and passing this obstacle would unlock a lot of value.

Another challenge he mentioned - the relevance of this in developed markets (where drugs make the most money). I’ve got more comfort on that one after the US compassionate use case. I had comfort even earlier, but this US case allowed updating of probabilites further. MDR bacteria looks to be a relevant problem even for developed markets.

I think Donald mentioned somewhere about Ayush’s framework of “business in transition”. It is one marker I have learnt to look for also, and I can fully appreciate where he comes from. The market often reacts with skepticism when early signs of transition show up. It often gives a good risk-reward for those that are tracking and have the risk appetite.

I did mentally put Wockhardt under this “business in transition” bucket. The market sees a drug manufacturer which has faced several FDA issues in the past, and has a splotchy history. But this is taking an innovator/ research turn. The time to act is when the market is still skeptical or has not even recognized the transition. This is obviously only for those with a high risk appetite.

I remember an industry veteran pointing to all the money poured into research and suggesting that the time value of that money should be looked at. Yes, that is true for the promoters, but for minority shareholders who got in when the business was priced such that nothing would come off all the research, the money poured in does not matter. For simplicity’s sake, if they poured in Rs. 100, and I got into the bus when the company was valued at Rs. 60, I just need returns on my 60. I don’t need to worry about the 100 poured in. These views are part of the same skepticism.

It reminds me of Druckenmiller’s story when he was made Director of research at the age of 25, with even a 52 year old reporting to him.

After about a year and a half -I was a banking and a chemical analyst -this guy calls me into his office and announces he’s going to make me the director of research, and these other eight guys and my 52-year-old boss are going to report to me. So, I started to think I’m pretty good stuff here. But he instantly said, “Now, do you know why I’m doing this?” I said no. He says, “Because for the same reason they send l8-year-olds to war. You’re too dumb, too young, and too inexperienced not to know to charge. We around here have been in a bear market since 1968.” This was 1978. “I think a big secular bull market’s coming. We’ve all got scars. We’re not going to be able to pull the trigger. So, I need a young, inexperienced guy. But I think you’ve got the magic to go in there and lead the charge.”

So I see it a bit like that. Veterans are scarred. Maybe we are the naive ones, but naivette might be the factor that is required to bell this cat.

Time will tell. All the best to those who are on this boat.

Disclosure: Invested from low levels, and views could be unknowingly biased. I see this as a high-risk investment and it is one made “from the heart” for me