Axis Asset Management Company and Axis Mutual Fund Trustee have settled a matter with the Sebi by paying Rs 16.57 lakh

Posts in category All News

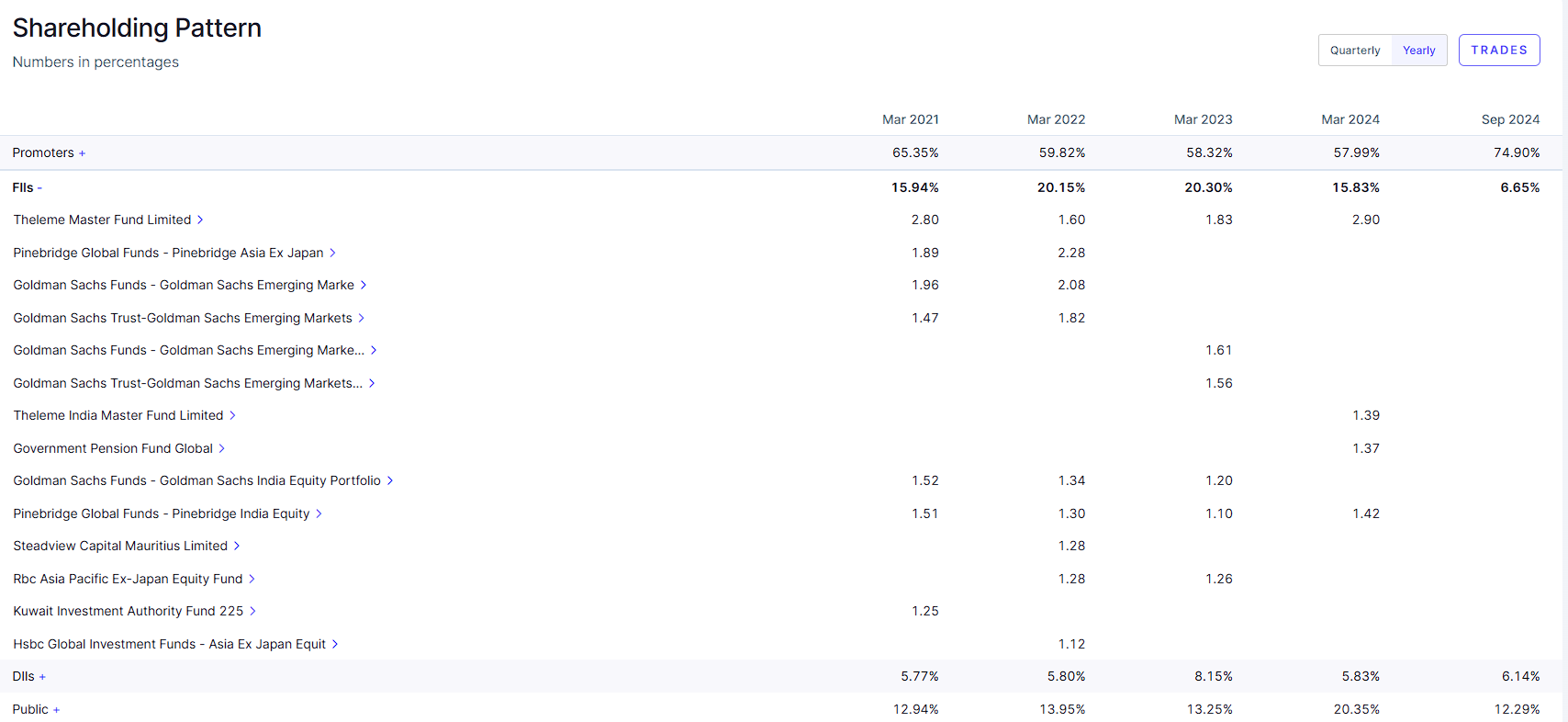

Route Mobile – Internet, Mobile & Telecom (26-11-2024)

FII’s are the major sellers for this stock; do they see any triggers or are they just moving to better opportunities available in the market?

Tinna rubber – recycling a rubbery growth path (26-11-2024)

Thanks for the info, appreciate it.

The question here is whether the EPR income is allowed as per accounting terms. It can be accounted on accrual basis or on cash basis is a different story, if its done on cash / sale basis its conservaitve which is appreciated. The revenues will be lumpy. Is it not allowed as per accounting standards to be done on accrual basis, if so then EPR should not be shown. It its allowed then there should be no issues, its upto the investor to decide.

As regards actual sale of EPR to tyre companies, to my knowledge EPR is mandated by law and all companies, whether tyre or otehrwise, will have to abide by it. Its whether it bought today or 2 qtrs later. To the best of my knowledge its not optional and done by govt to shift the onus on industry to hide their inability to manage this. The issue now is the price at which this is done.

The discussion and debate here is made out to be is that the income is not legal and should never have been in the P&L.

Am happy to be corrected on this basis facts.

Multi-Disciplinary Reading – Book Reviews (26-11-2024)

The Great Indian Fraud: Serious Frauds Which Shook the Economy by Smarak Swain (2020)

I loved this book! It’s written by an IRS officer who has likely witnessed and investigated many serious financial frauds first-hand. The book covers all major flavors of fraud that happen in India (from loan frauds to stock market frauds to GST frauds and so on). The author has covered multiple in-depth examples for each type of fraud, as well as discussed, the modus operandi of the fraudsters in a lot of detail. While I kind of knew a bit about most of the cases discussed in the book, but reading the book dispelled my illusion of explanatory depth. Also, there were some major frauds that I didn’t know much about like Bhushan Steel, PACL, Ricoh India, Anubhav Plantations etc. I will highly recommend this book to any serious investor.

Below are some notes I took which in no way substitute a reading the book itself:

1/ The Perfect Bank Heist: Loan Fraud

-

Per Deloitte, 10 per cent of all bank frauds are a result of overvaluation or non-existence of collaterals. About 9 per cent bank frauds are due to siphoning off or diversion of funds and 15 per cent frauds are attributed to fraudulent documentation. A typical loan fraud is usually a combination of these three.

-

Common modus operandi used for siphoning funds: intangible assets such as software, patent, technical design, brand, etc., are preferred over tangible assets as it is difficult to ascertain the legitimate valuation of intangibles.

-

Company committing fraud does purchase some physical assets, but at a highly inflated price. The company may purchase a building or land from a relative of the promoter. The valuation is boosted by getting a report from a certified valuation engineer. The bank remains under the perception that the land is worth the amount paid for it.

-

Shadow banks (NBFCs and HFCs) advance loans to infrastructure projects, real estate developers, logistics projects and retail consumers. In India, NBFCs have funded ~57% of commercial vehicle purchases, 30% passenger car purchases and nearly 65% of two-wheelers.

-

Before the IL&FS scandal, ~27% of NBFCs’ funding would come from mutual funds. Mutual funds would buy commercial papers from NBFCs for short periods (90–120 days) and then used them to roll over the advance. This helped the NBFCs to obtain short-term loans and allowed them to roll over the loans upon maturity. They used these loans to give long-term advances to their customers. Real estate companies were getting money largely from the NBFCs because they were not getting any lending from the banks.

-

Finally, the shadow bank defaulted in September 2018 and set off a ‘shadow bank crisis’, wherein mutual funds stopped renewing their loans to other shadow banks. Shadow banks had to pull out their advances from the market to payback. This crippled the auto and real estate industries.

-

Before 2016, two primary channels available with bankers to recover stressed assets were the Debt Recovery Tribunal (DRT) and Asset Reconstruction Companies (ARCs). The DRTs were set up in 1993, with the aim to help bankers recover debts. The average rate of recovery for DRTs between 2002 and 2009 was 37%

-

The ARCs, which started operating in 2002, specialise in sale, purchase and recovery of NPAs. Banks can sell their stressed assets to ARCs at a discount and avoid the lengthy process of civil suits. Between 2002 and 2009, banks have had an average rate of recovery of 39% through the ARC route.

-

The increasing NPA problems in India since 2009 convinced policymakers that a more comprehensive reform to handle the NPAs was required. Thus, the Insolvency and Bankruptcy Code (IBC) was duly introduced. The IBC achieved substantial success in faster recovery of bad loans. The average rate of recovery for banks and other financial creditors through the IBC route has been 43 per cent.

2/ Securities Fraud

-

There are two broad types of stock manipulation: price manipulation and volume manipulation. While manipulations can take many forms, ‘pump and dump’ is the basic price manipulation technique and ‘wash sales’ is the basic volume manipulation technique.

-

Haridas Mundhra is widely acknowledged as one of the first and a leading scamster of modern India. His was the first major financial fraud of Independent India. While he is infamous for the LIC scam, but, in addition, he was a sophisticated gamer of stock markets.

-

Loan Against Shares (LAS) is an age-old instrument used by entrepreneurs to raise loans for business. Haridas Mundhra misused LAS by taking loans against artificially-priced shares. He used the loan to artificially jack up prices so that he could get more LAS. Ketan Parekh’s scam was quite similar.

-

Parekh’s strategy was to pump the prices of select scrips and then engage in wash sales to stabilise the prices at artificially high levels. Then he used the artificially priced shares as collateral to take loans from banks and siphon off loan money. And then he used the loan money to pump the price further. As a broker, he drove the narrative that technology and entertainment companies were underpriced and that they had a strong future.

3/ EXIM Fraud – Nirav Modi

-

Nirav Modi’s fraud was being presented as a loan fraud, while it was actually an export-import fraud. This fraud was basically a trade-based money laundering.

-

The dominant narrative in the media was that two employees in PNB were issuing Letters of Undertaking (LoU), kind of a bank guarantee, to foreign banks vouching for Modi’s firms. Modi’s firms took short-term loans from foreign banks against the bank guarantees. PNB was issuing the bank guarantees without taking any collateral and refused to issue fresh bank guarantees. As a result, Modi’s firms defaulted on their old loans and the foreign firms invoked the guarantees, asking PNB to pay up.

-

This fraud was basically a trade-based money laundering. It was evident from the facts marshalled by both the CBI and the ED in their charge sheets. Most experts who attempted to understand the fraud looked at it as a loan default.

-

Post this fraud the RBI banned the use of LoU as a financial instrument.

-

Valuations for diamonds are very fuzzy, more so for rough diamonds. As a result, diamonds are ideal products for under-invoicing and over-invoicing manipulations. Complex money laundering can also be committed using under invoicing or over invoicing.

-

LoUs, bank guarantees and LCs interchangeably are conceptually similar instruments. However, they differ significantly in their contractual terms. The advantage of LoU as a financial instrument is that once it is produced in an overseas bank, the entire onus of creditworthiness shifts from the importer to the domestic bank issuing the LoU. In case of LC and bank guarantees, importers have to prove their creditworthiness to the overseas bank.

4/ Most serious EXIM fraud – country of origin (COO) fraud

-

The import of stainless steel from Indonesia into India had grown from about 8,000 tonnes in FY 2017–18 to 67,000 tonnes in 2018–19. A country does not suddenly develop the capacity to manufacture stainless steel at this pace.

-

ISSDA’s investigation concluded that these imports were of Chinese origin, but routed through Indonesia because China has an FTA with the Association of Southeast Asian Nations (ASEAN), of which Indonesia is a member and ASEAN has an FTA with India. By the virtue of its FTA with ASEAN, Chinese exporters could export to Indonesia without incurring any duty. These exports were then re-exported to India duty free because of the FTA between ASEAN and India.

-

The FTA between India and ASEAN stipulates that preferential duty rate could be claimed by an exporter to India only if the country of origin is in ASEAN. FTA benefits can be denied by India if the value addition in ASEAN region is less than 35 per cent.

-

Chinese exporters route their goods through Indonesia with cosmetic value addition in Indonesia, but manage to get origin certificates from Indonesia, thus hoodwinking Indian customs officials. This is called origin fraud or country of origin (COO) fraud.

-

Logistics costs in China are one of the lowest in Asia and much lower than India. The Chinese cost of logistics is 1% of their business. In India, it calculates to 3%. Similarly, the effective cost of electricity in India is anywhere between 12 and 14 rupees, which is higher in comparison to China. India suffers cost competitiveness by almost 9% to their competition with China on account of energy, finance and logistics.

-

Before 2018, India did not have a coordinated strategy for defending its economic borders from predatory exporters: Anti-dumping duties were imposed by the Directorate General of Anti-dumping and Allied Duties (DGAD). The Directorate of Safeguards (DoS), in the Department of Revenue under the Ministry of Finance, took safeguard measures. The Directorate General of Foreign Trade (DGFT) imposed Quantitative Restrictions (QRs).

-

Finally, the DGTR was constituted on 7 May 2018. All powers of imposing anti-dumping duties, safeguards and QRs now vest with this single authority.

-

Origin fraud works as a cheat code to circumvent the defences laid out by the DGTR. There are broadly two types of origin fraud through which circumvention of trade defences happens: transhipment and assembly operations.

-

Under transhipment, goods from the country of origin are sent to the destination country, but certificates of origin are obtained from a conduit country. Under assembly operations, parts are sent from country of origin to conduit country; they are then assembled in the conduit country and shipped to the destination country.

5/ GST Frauds

-

The problem of fake exports has become even more acute with the advent of the GST.

-

If the output GST liability is lower than the ITC (input tax credit), the government has to refund the difference amount to the firm. Refunds arise whenever there is an inverted duty structure. That is, when the GST rate on sales is lower than the GST rate on purchases.

-

For instance, the GST on non-woven fabric is 12 per cent, but the GST on fabric bags is 5 per cent. A boutique purchases non-woven fabric at ₹100, weaves it into a bag and sells the bag at ₹200. Its output GST liability is 5 per cent of ₹200, which works out to ₹10. Its ITC is 12 per cent of ₹100, which works out to ₹12. Since GST credit is more than GST liability, the boutique can claim the difference (₹12 – ₹10) as a refund from the government.

-

This is where an arbitrage opens up for scammers. The scammers incorporate a shell company, draw a fake invoice for purchasing fabric raw materials from a benami supplier and a fake invoice for selling fabric bags to a benami shopkeeper. And then they can claim a refund from the government.

-

Although GST refund fraud can happen wherever there is an inverted duty structure, large refund frauds happen in connection with the export of goods. Whenever goods or services are exported, the end consumer is located outside the country. The country does not have the right to tax an end consumer living outside its borders. Hence, no output GST is levied on exports.

-

A Delhi-based syndicates exporting tobacco through Kandla SEZ, it was found that although low quality tobacco was purchased in cash from local markets at ₹150–₹350 per kg, fake purchase invoice was drawn at ₹5,000–₹9,000 per kg. The DGGI found that fake invoices were issued by 25 different suppliers in Assam, Bihar, Delhi, Haryana, MP and UP. By the time DGGI acted against the syndicate, it had claimed refund of ₹400 crore on fake invoices worth ₹1,000 crore.

-

Sin goods attract GST at a rate of 93 per cent. By drawing fake purchase invoices, the exporters got input tax credit of 93 per cent of the purchase price. After making fake exports, they claimed the entire ITC as a refund from the government.

6/ Accounting Fraud

-

The Satyam scandal prompted lawmakers to relook at audit norms and introduce better control and supervision, a process that culminated in a complete overhaul of the corporate laws of India in 2013.

-

Accounting frauds are criminal offences under the new Companies Act of 2013. The new Act has bestowed enforcement powers to the SFIO. It has also proposed setting up an independent regulator for auditors, called the National Financial Reporting Authority (NFRA) which now exercises regulatory and penal powers over errant auditors.

-

There are now six different authorities regulating the function of auditors:

- Ministry of Corporate Affairs (MCA) regulates auditors of all companies

- The SFIO undertakes criminal proceedings against errant auditors

- The NFRA imposes penal action for audit lapses

- The ICAI undertakes disciplinary proceedings against auditors

- SEBI regulates auditors of listed companies

- The RBI regulates auditors of banks and NBFCs

-

It is relatively easier to influence small audit firms than the large ones: there are only 15 audit firms that audit 10 or more listed companies. Whereas, as many as 654 audit firms have just one listed company as their client.

-

One typical model that creates a stable fraud cycle is the equity-to-profit scheme. In this scheme, a company fraudulently shows high profits, indicating that the company is doing well. This pushes up the company’s valuation. The company then lures investors to buy its equity at a high valuation. Investors pump capital into the company. The company then converts the same capital into profits. (Ricoh India is a case in point)

-

Related party transactions (RPT) are an important innovation in the history of accounting frauds. Most related party transactions are benign and rather help genuine businesses prosper.

-

All major fraud investigations by the SFIO and other agencies in the last decade, including that of Satyam Computer Services, IL&FS, Vijay Mallya group, and Bhushan Steel group, have revealed questionable related party transactions.

-

Related parties are important to equity-to-profit schemes because they facilitate conversion of capital into profits in the books of a company.

7/ Ponzi schemes

-

The largest online ponzi scheme that has been detected so far is China’s Ezubao. It projected itself as a start-up running peer- to-peer lending and collected massive funds from Chinese residents, promising them huge returns from peer-to-peer lending.

-

Amit Bhardwaj, infamously known as the Bitcoin Ponzi King, ran a scheme that promised high returns to anyone who invested in Bitcoins through his website www.gainbitcoin.com.

-

Modus operandi of large ponzi schemes is they run front businesses such as real estate, jewellery retail, pharmaceuticals, etc., to hoodwink SEBI and other regulators. By running multiple and diversified front businesses, they create a perception that they are big conglomerates.

8/ Tax havens

-

As per Tax Justice Network (TJN) the top 5 tax havens (in terms of their attractiveness): British Virgin Islands (BVI), Bermuda, Cayman Islands, The Netherlands, Switzerland

-

Switzerland’s bank secrecy laws are famous, primarily because the country got into the business quite early on. It was a haven of peace in the middle of a turbulent Europe in the 17th and 18th centuries.

-

Another country with stringent banking secrecy laws is Dubai. It stubbornly maintains opacity of its banking transactions despite pressure from the FATF.

-

Dubai has also succeeded in becoming the world’s hawala capital. Hawala trade developed as a by-product of the smuggling racket run from Dubai.

-

Tax havens have four types of offerings: personal bank accounts, mailbox companies, foundation and trust.

9/ Trusts

-

Foundations and trusts are more popular than companies when it comes to protecting wealth. A trust has no owner since it is not a legal entity. It is merely a legal arrangement (like a contract).

-

A typical trust is a three-way arrangement. The original owner (the ‘settlor’) transfers his wealth into a trust and asks a ‘trustee’ (or trustees) to manage the wealth, for the benefit of ‘beneficiaries’. The beneficiaries are usually family members of the settlor.

-

Trusts convert assets with clear ownership into ownerless assets. They slice and dice up the concept of “ownership” into different rights and duties.

-

From a legal perspective, the settlor no longer owns the assets. He has transferred the assets into a trust. The beneficiaries don’t own the assets either. They benefit from the trust, but they do not own it. The trustees are required to manage the assets under precise instructions of the settlor. Hence, the trustees do not own the assets.

-

Trusts manipulate ownership rights so that individuals can control and enjoy trust assets while legally distancing themselves far enough from them, so that the assets cannot be reached or even known about by creditors, tax authorities, law enforcement, or public scrutiny. These legal barriers can become impenetrable secrecy barriers shielding those people who enjoy and control the assets from scrutiny.

10/ Foundations

-

Foundations perform functions similar to trusts but there are key differences between them. A foundation is a legal entity upon registration. It can, therefore, open bank accounts. It can enter into agreements or contracts and can legally undertake business activity. The founder of a foundation (akin to the ‘settlor’ of a trust) transfers his assets to the foundation for a specific purpose. The assets are managed by a council (akin to the ‘trustees’ of a trust) in favour of specified beneficiaries.

-

If a person merely wants to park his/her wealth, trust is his instrument of choice. If the person wants to run a business activity without revealing his ownership, foundation is his instrument of choice.

11/ Shell companies in India

-

Running shell companies used to be big business in India until a few years back, with major hubs in and around Chowringhee area in Kolkata, Kalbadevi in Mumbai and Patparganj in New Delhi. People who operate shell companies are called ‘entry operators’ because they provide accommodation entries to their clients’ accounts.

-

The story runs in three phases: pre-2010 period, 2010–2015 period and post-2015 period. The industry running shell companies prospered until 2010. They were run by entry operators, who had a sound pedagogy in accountancy and taxation. Entry operators usually have CA inter or CA/CS qualification.

-

Organised clampdown on entry operators began in 2010. A new section, Section 56 (2) (viia), was introduced in the Income Tax Act. The new law brought down the entire industry in a matter of months.

-

The second phase started in 2010 where entry operators sprouted in a decentralised manner all over the country. This new breed of entry operators helped match parties. For instance, if a customer wanted to convert white money into black and another customer wanted to convert black money into white, the entry operator would bring the two together by matching their requirements.

-

Entry operators acquired NBFCs which they then freely used these firms to give accommodation entries. These NBFCs became the new highways through which money flowed from the formal economy to the parallel economy and vice versa.

-

Post-2015, various government agencies coordinated their attack on shell companies. The MCA prepared a list of companies that do not have significant operations and struck off many of these companies. The MCA struck off as many as 2.25 lakh shell companies in the FY 2017–18 and another 2.25 lakh in FY 2018–19.

-

A stringent Benami Transactions (Prohibition) Act was introduced in 2015, which effectively termed shell companies as benami conduits.

Trump’s Tariffs Would Deal a Big Blow to the Auto Industry (26-11-2024)

Automakers and parts suppliers would struggle if President-elect Donald J. Trump followed through on his threat to impose 25 percent tariffs on imports from Canada and Mexico.

Lotus Chocolate Company: A Tasty Affair (26-11-2024)

A new Independent Director is on board, but one notable factor here is her position in a few Reliance group companies. This makes me feel that Reliance is not just being a stakeholder but actively participating in the company’s day-to-day business affairs.

Her work experience –