Much awaited results out.

I have been tracking this bank from last 8 quarters and I can say this is one of the best quarter I have ever witnessed as far as the business is concerned.

Yes bank is still in recovery phase and has not yet entered the growth phase. They enter growth phase after asset transfer and capital raising.

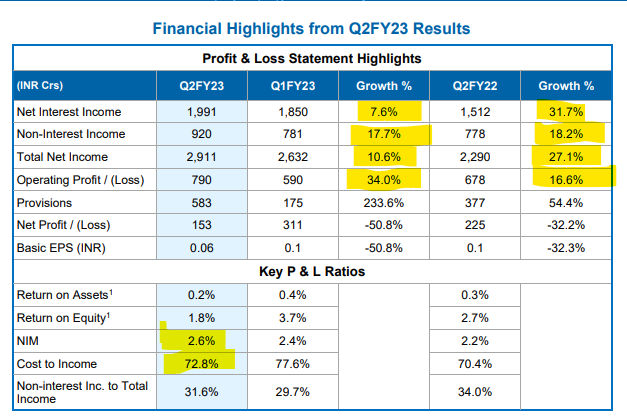

Profitability is low because of high provision and next quarter also it is likely to be high because they want to transfer asset with maximum provision. I don’t care much about provision because business is doing fantastic and also their provision coverage is at 84% so if recovery happens in future profitability is automatically going to be high because of reversal.

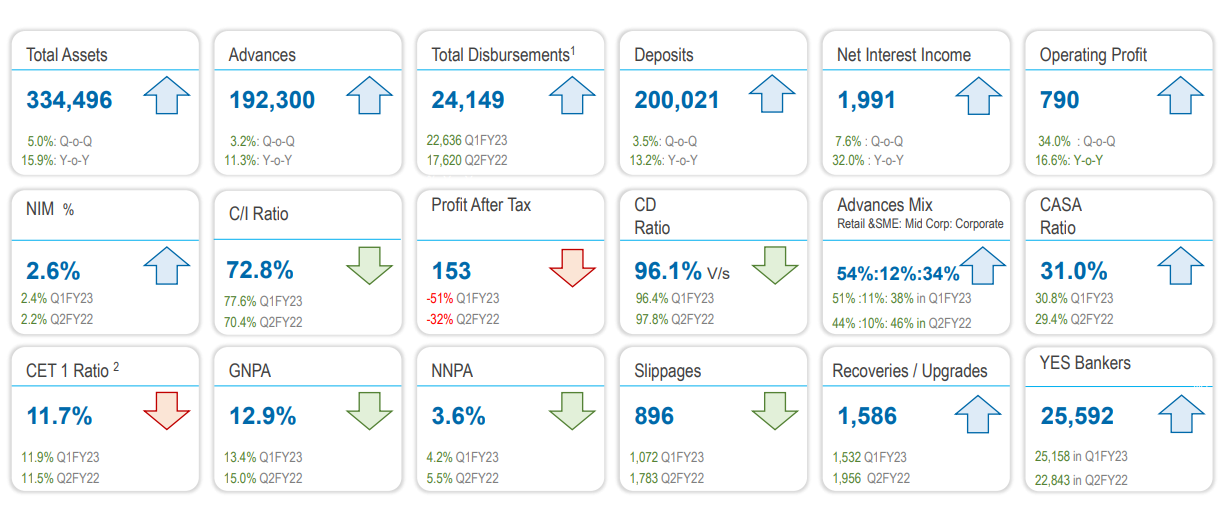

They have literally improved in all parameter

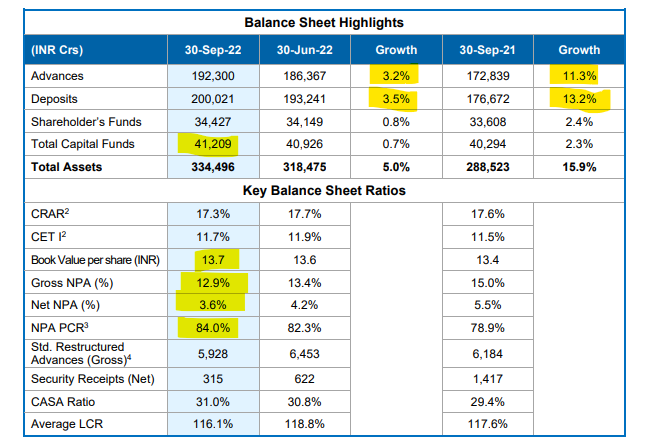

- Gross NAP and NET NPA are lower

- NIM is at 2.6 ( will improve)

- PCR at 84% and balance sheet at 334496

- Cost to income lower at 72%. Operating profit and NII higher QoQ and YoY.

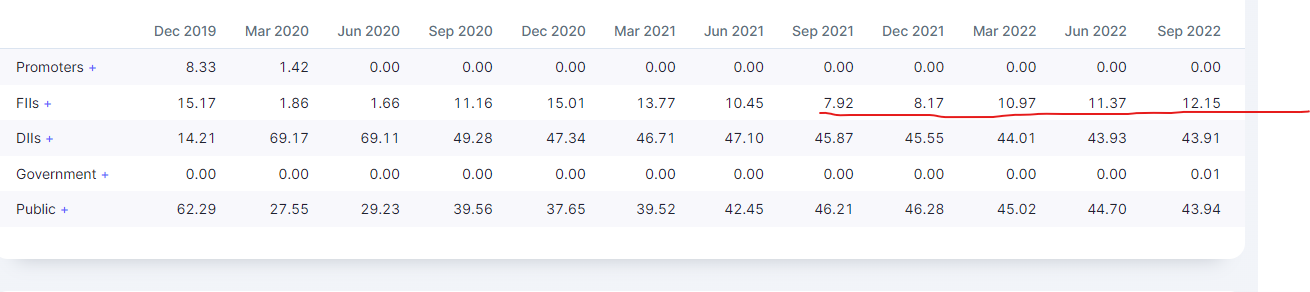

FII holding continuously increasing from last five quarter and this is without advent and Carlyle

This year profitability will not meat management estimates but on all other parameter they are on track. The more provision they do now the more reversal comes in future

Slippage is lower QoQ and YoY and 61 to 91 days bucket is lowered by 3000cr

Business performance is extremally good but still below industry majorly because of they not completely focusing on growth.

| Subscribe To Our Free Newsletter |