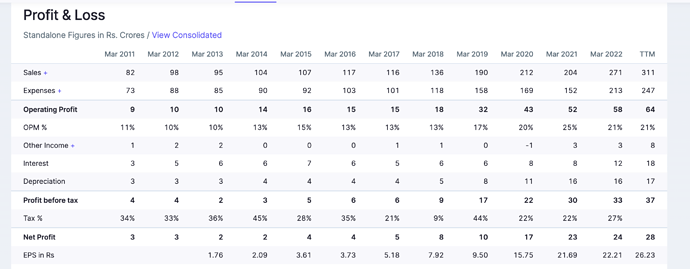

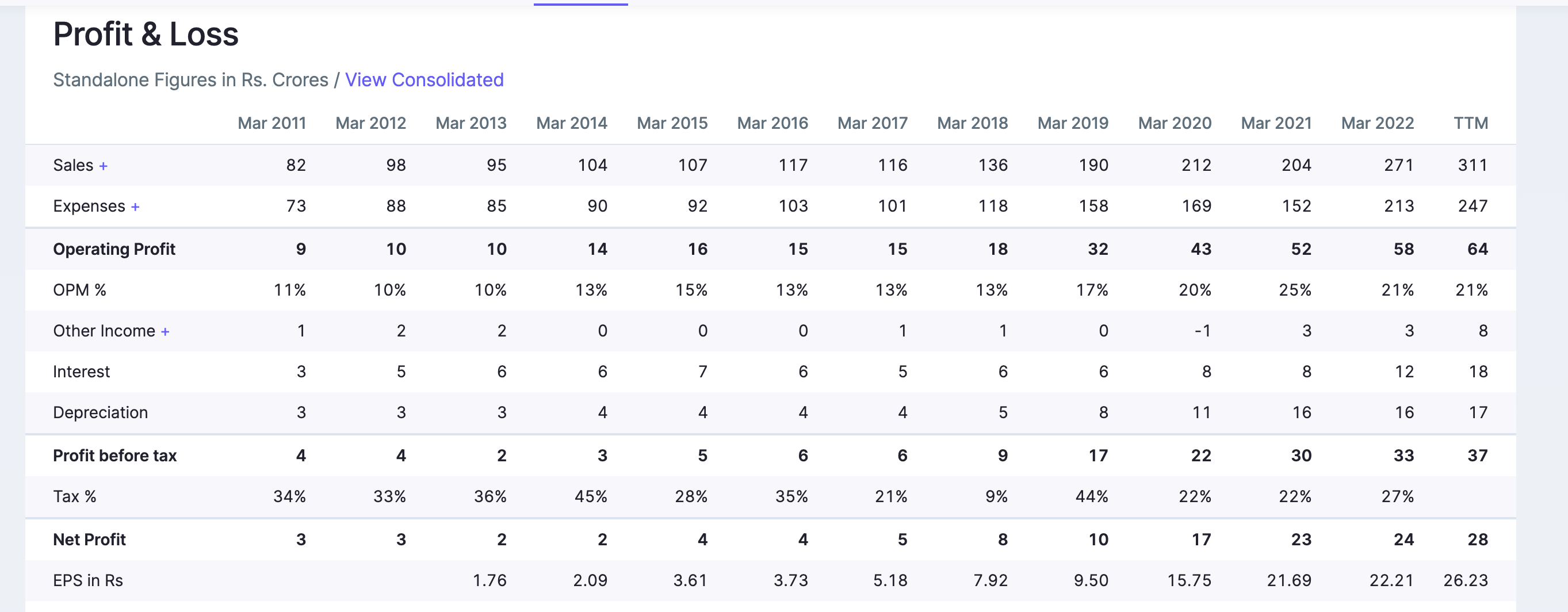

I had invested in RACL in April of 2020 at an average price of 60. It ended up becoming my first ten bagger in a year. I sold out when the price crossed 700 and I realized that the promoters would have no choice but to pile on debt to grow further. However as I’ve tracked the company from the sidelines it has become markedly less attractive from an accounting perspective than it was in 2019.

Few red flags:

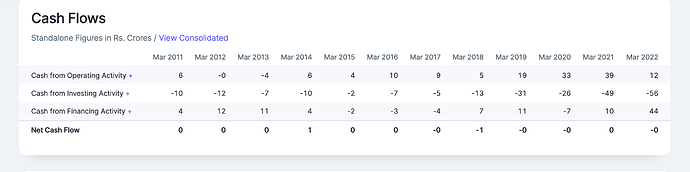

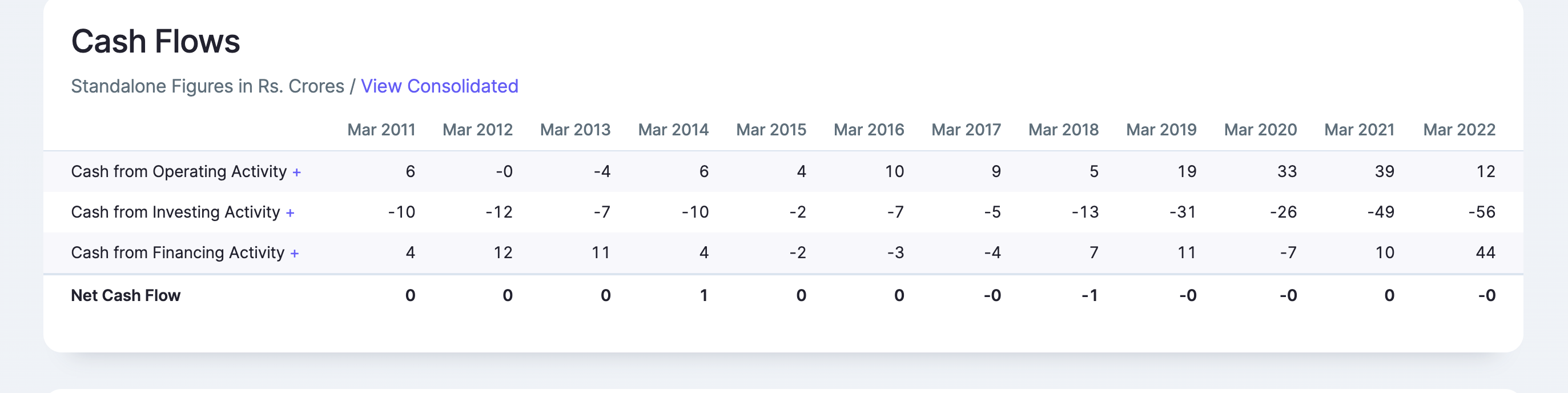

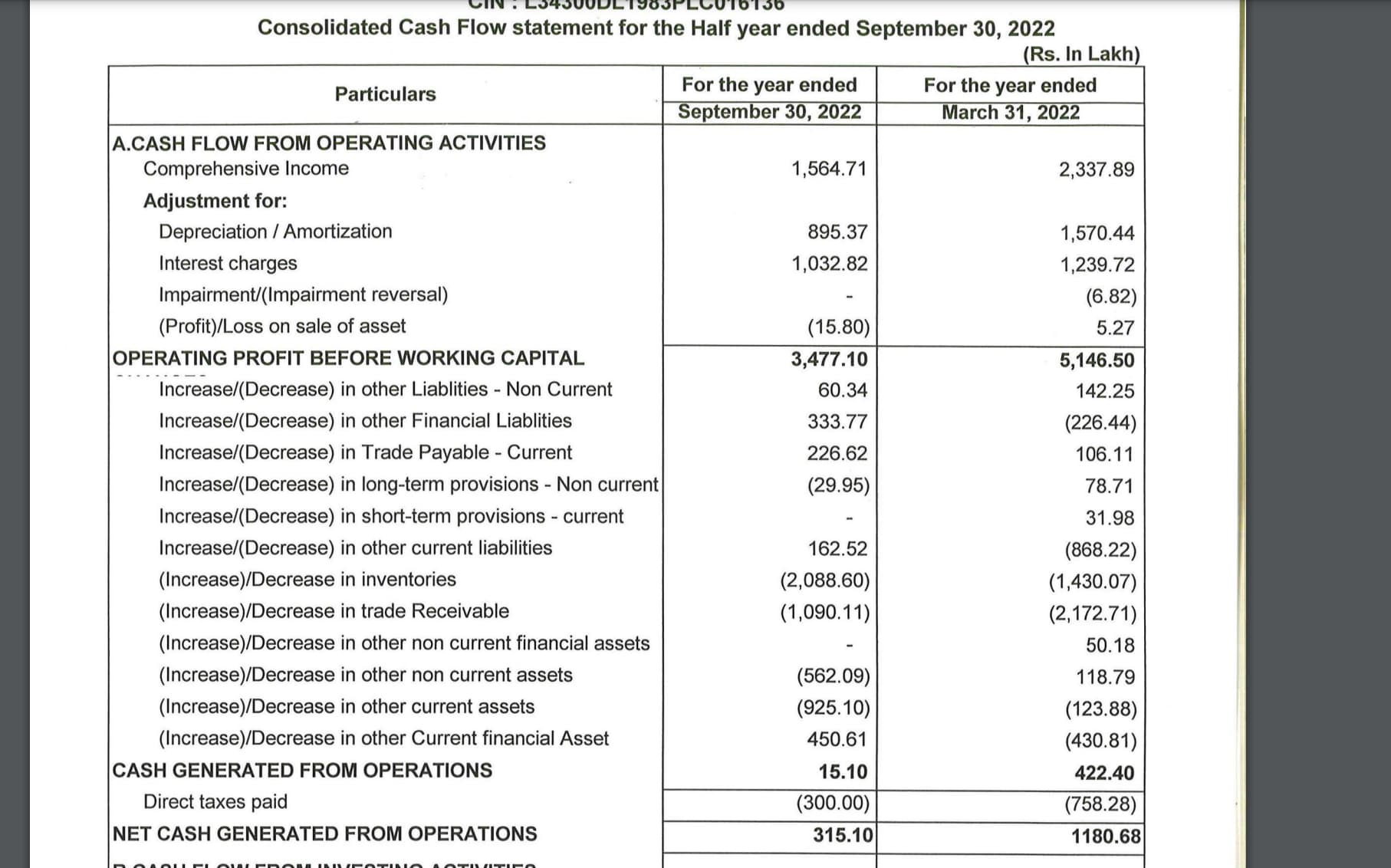

- Cash generation was never an issue for RACL until FY21. Profits were consistently being converted to cash.

That dropped off a cliff in FY22 and has been even worse in H1FY23. Its so bad now that they are unable to fund even interest payments from operating cash flows – they have need to draw down additional borrowing for that.

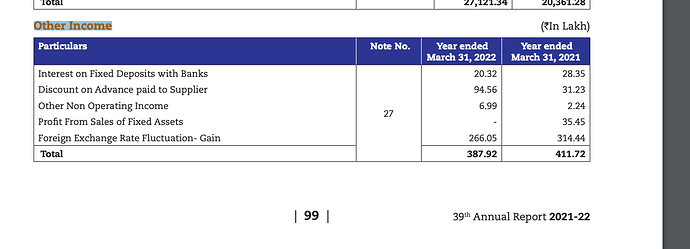

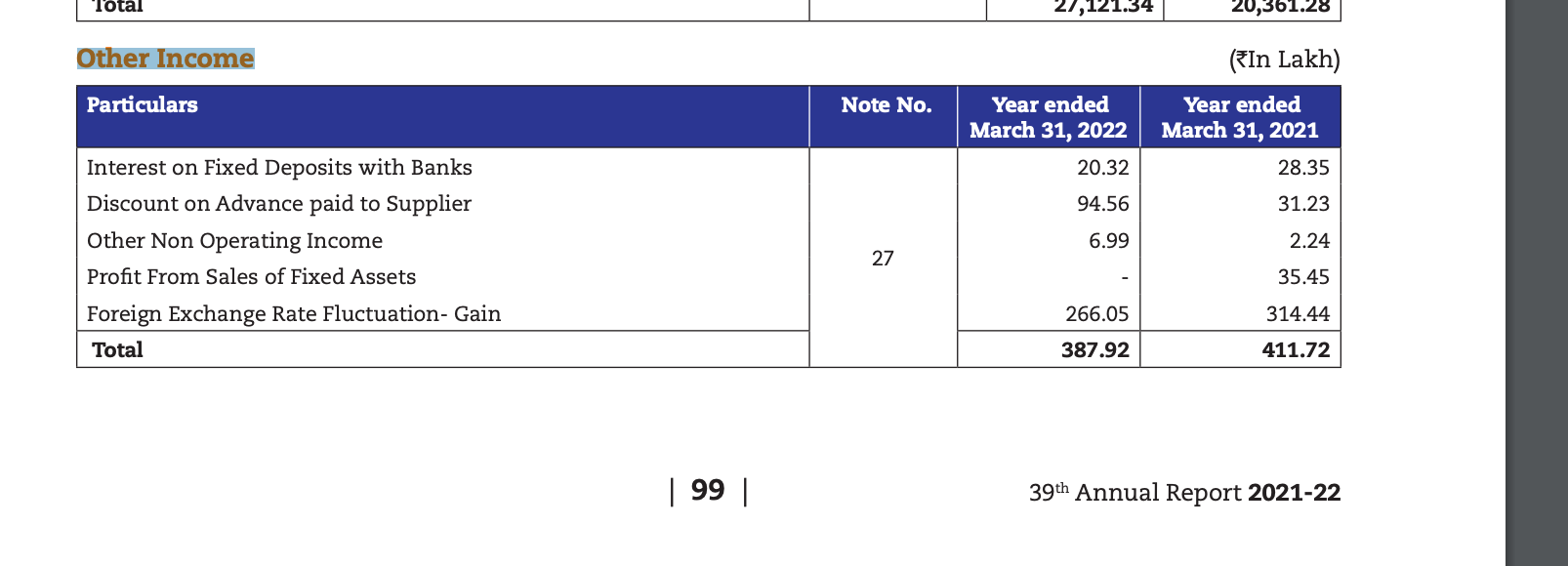

- Other income shot up from nothing in FY20 to INR 8cr in the trailing 12 months which is > 20% of PBT. This income is largely gains on holding foreign exchange.

RACL seems to have become an astute forex trader. Made increasing gains in last 3 years consistently while EURINR has fluctuated wildly.

-

Depreciation policy is odd. Depreciation wildly fluctuates on a quarterly basis with depreciation in the March quarter being nearly 2x of other quarters.

-

Naturally with such cash flow deterioration and aggressive capex, debt has exploded to INR 200 cr. This debt is not cheap (last q interest cost was 5 cr which would imply annualized interest cost of 10%) and is likely to rise when long term borrowings need to be rolled over.

The only two parameters that RACL has improved on in the last 18 months are accounting profits and investor communication.

| Subscribe To Our Free Newsletter |