Debt has always been a concern for RACL Geartech considering their high receivable and inventory days. But I think Mr. Singh has explained why the business fundamentals require such high inventory and receivable days amply in the calls. Also if you take a look at debtor days and inventory days below, there is no material change from 2018 to 2022. For TTM, inventory days are 175 and receivable days are 103. Inventories are actually much lower at the moment than the historical trend.

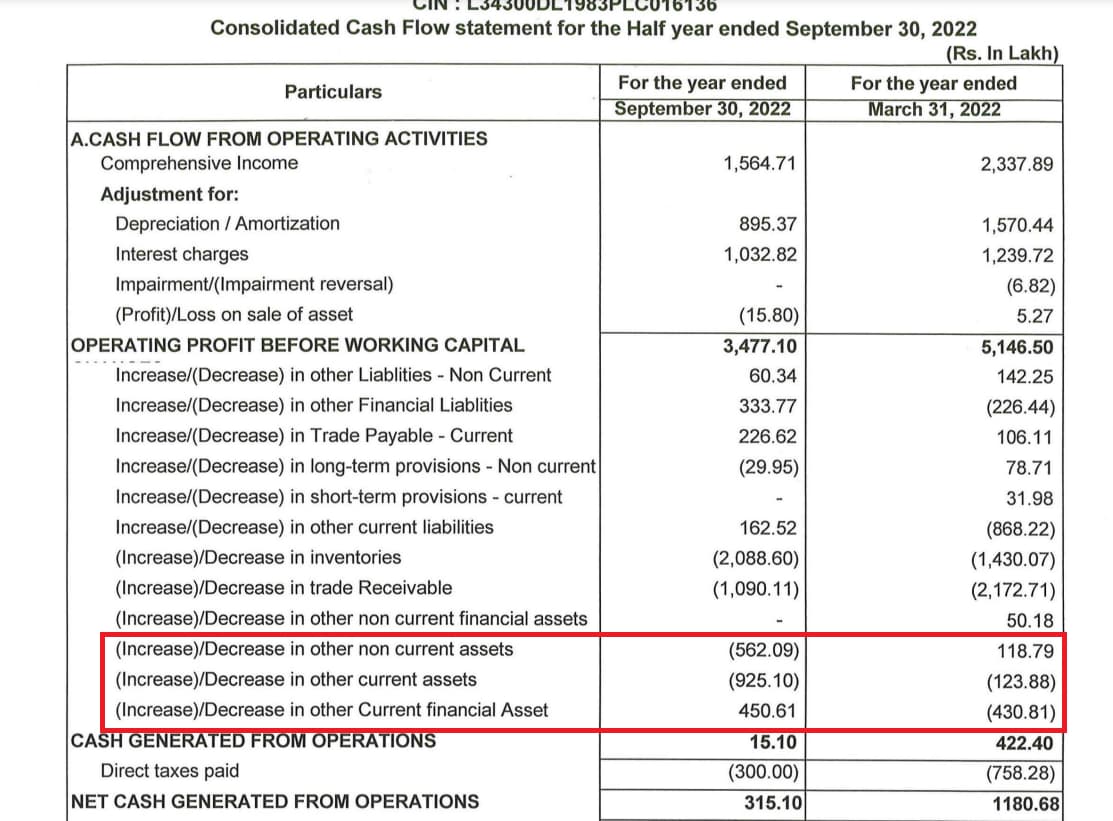

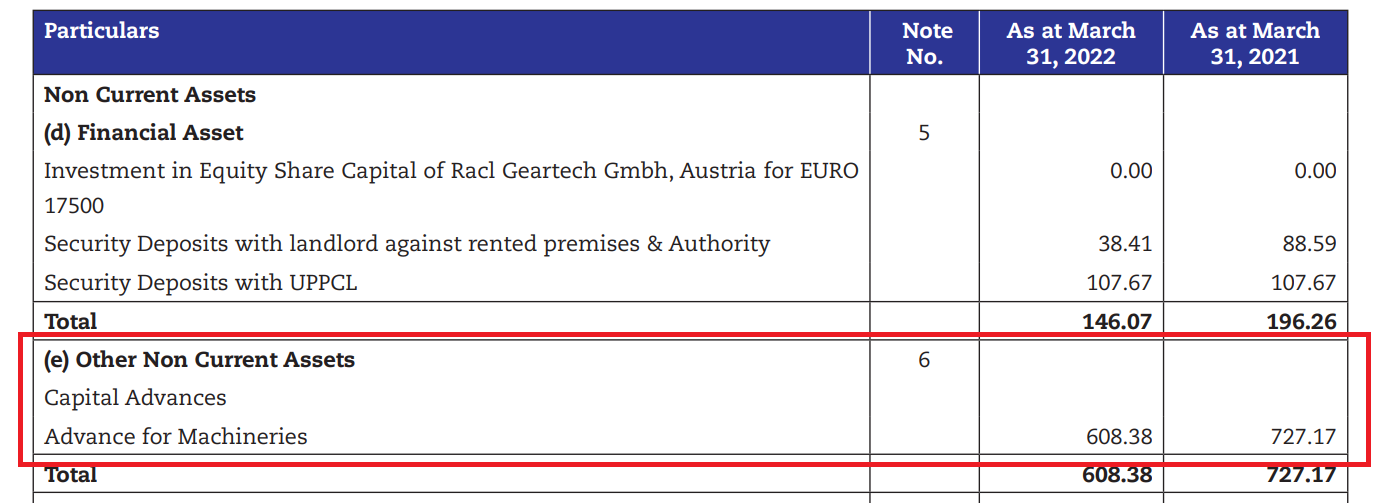

The major hit in operating cash flows in H1FY23 has come from Other current assets and other non current assets

If you check what these items are from ARFY22, you will realize these pertain to advances for machineries, prepaid expenses and advances to suppliers. So these mostly relate to advance cash outflows meant for putting up the new capacities required. Therefore, I wouldn’t be too concerned about quality of cash flows at this point. I expect cash flows to revert to the mean when the new capacities stabilize.

On the whole though, the high debt burden is probably the only thing that rankles a little for investors. I am hoping they will be able to retire more debt once their domestic business share picks up. The domestic business would have a much shorter cash conversion cycle and would boost their OCF.

I also did not understand Mr. Singh’s comment on the call regarding 4% net/net interest rates as I mentioned in my notes above. Interest rates are clearly @ around 10% as evidenced by ~20Cr interest costs on ~200Cr loans. If anybody understood what he meant by that, please let us know.

| Subscribe To Our Free Newsletter |