HEG does have a Graphite story brewing up and from my point of view it is very interesting.

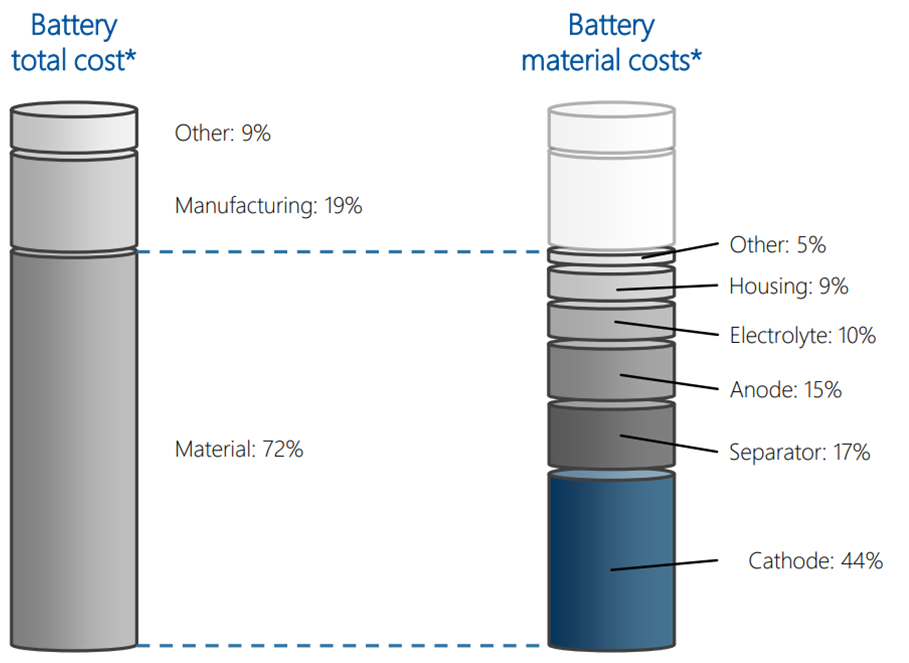

Lets look at the anode part of an EV. We can see that the anode is 15% of the overall cost of the battery. The anode is made up of powder graphite with various binder in it. The particle size of the carbon needs to be small and the purity of the powder should be high.

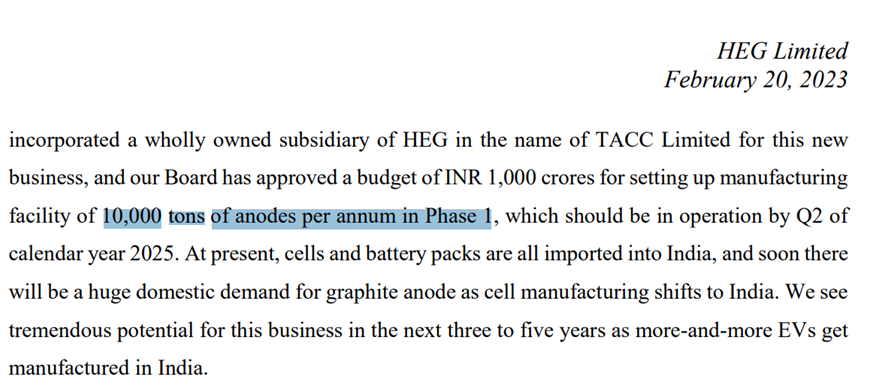

HEG has a new subsidiary TACC which will produce the graphite for anode. They will invest 1000 cr in CAPEX. The yearly output of the plant will be 10000 tons. The plant will be in operational from Q2CY25. The revenue will be 1000 cr and the margins will be around 30% [Interview of Mr. Riju Jhunjhunwala]

Why is this important ?

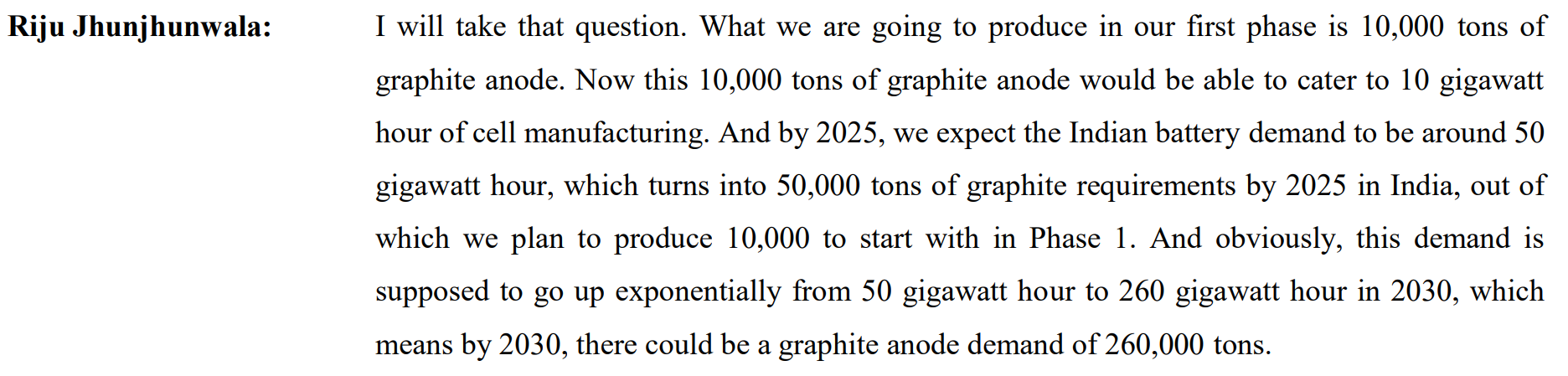

India has a PLI scheme to set up a 50 GWh cell manufacturing plant. As per Mr. Riju, to produce 10 GWh of cell, the graphite required in the anode would be 10000 tons. By 2030, the total requirement will be 260 GWh. This in my opinion is huge opportunity and currently all the graphite is being imported.

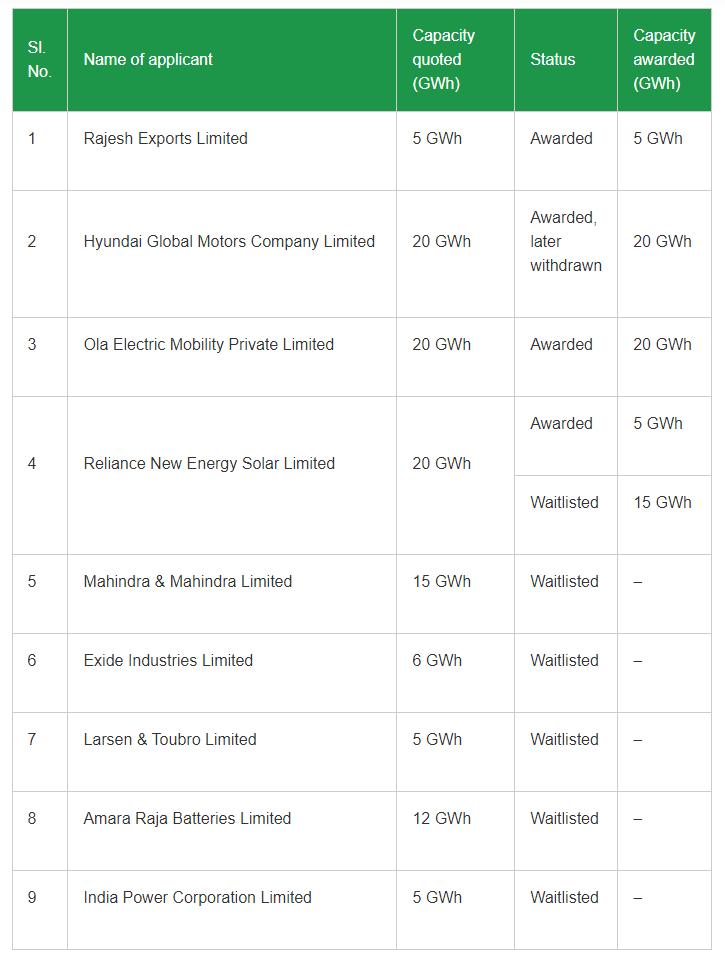

The following players have been awarded by the PLI scheme to set up Lithium ion cell production.

Valuation ?

The market still views HEG as a deep cyclical company. In case the Anode story plays out the cyclicality will be reduced and the company can get re-rated to 4-6 times P/S.

Disc: Biased. Invested (0.5% PF) willing to scale up as numbers come.

| Subscribe To Our Free Newsletter |