Thanks Girish for your comments. Thanks to all who continue to like my posts.

Girish on IRIS, COVID and reporting oversight bodies delayed certain regulatory implementation. I think biggest opportunity for them is ESG reporting in US which encompasses 1000s of companies, which has been delayed for a year or two. Another thing is that it was difficult for me to understand how good their products are. They rely on partners to get their product integrated, direct sales seems to be limited. So I am not sure if there is any product pull.

However, there is no denial that the size of opportunity is good. Also they mention that they don’t have marketing muscle. One of the founder, Mr. Bala, will sell 2lakh shares (over the next 1 year), he holds 11 lakh shares. Very rare to see such disclosures and also in so much advance, kudos on transparency. Mr. Swaminathan, CEO, also seems to be a very good person, I think he did not take salary for many many years.

I think what can elevate their business to next level is, assisting the companies in preparing reports (data entry in India) and complement them with its own products (basically a BPO set up complementing its products). However, given the sensitivity of compliance I am not sure how feasible is this.

Disclaimer: Please note that these are my personal views and should not be construed as buy or sell recommendation. I am not a SEBI registered analyst.

Now my rationale on ICICI Lombard General Insurance (ICGI) (8% of portfolio, 5% profit)

Background: My first buy was in July 2020 at 1307 rs, my last transaction (buy) was in March 2023 at 1160 rs. My average cost is 1293 rs.

During COVID I was keeping eye on the companies which do not lose sale despite lock-downs and such severe humanity crisis. I found ICGI’s revenues were broadly stable or marginally growing, so I entered the stock in July 2020. I also added it aggressively from mid-2022 as I expected it to benefit from higher interest rates and auto recovery.

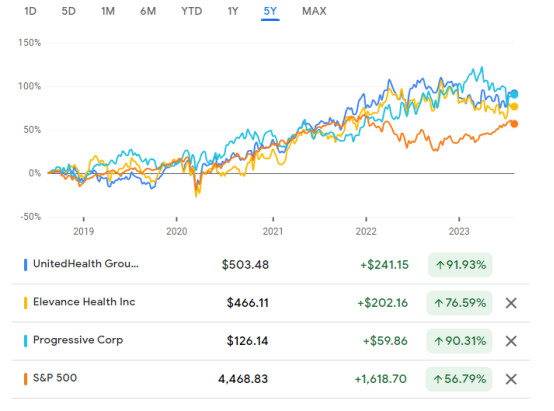

I looked at general insurance companies in the US. I noted that the market cap of large companies in US is anywhere between USD50-470 billion (ICGI is ~8 billion). Total return (including dividends) of these companies is 20% or above for last 10 years vs. S&P 500 ~10%. You can check total returns here https://www.financecharts.com/stocks/PGR/growth/total-return . Also below graph shows that these companies have handsomely beaten S&P 500 over the last 5 years.

Source: google finance.

I feel some of the large Indian GI companies can do in line or better than US companies on a long-term basis. India is very under-penetrated on health insurance while motor insurance will continue to grow with increased number of vehicles.

I believe we have not even scratched surface on fire/construction/marine/cargo insurance. Ask yourself is your home insured? If not that shows under-penetration or lack of awareness.

Company is focussed on profitable growth. They exited crop insurance in 2019 when everyone was very hot on it (ICICI-Lombard exits crop insurance business – Times of India). Management is active as they acquired Bharti Axa operations couple of years back. They are targeting to improve combined ratio to 102% over the next two year which shall improve profitability somewhat.

So far company has been a drag on my portfolio but I expect ICGI and Bajaj Finserv to do well when market breadth gets narrow (a period like 2018). Its like having Rahul Dravid on Australian pitch. Financial services is an area where bigger keeps getting bigger.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock without any prior intimation.

| Subscribe To Our Free Newsletter |