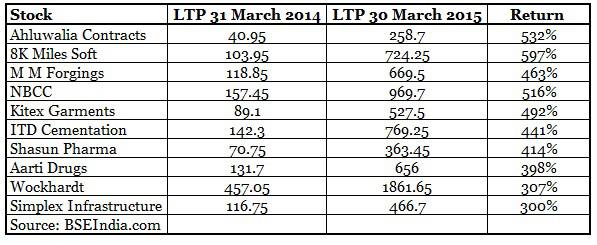

midacap-1 Post navigation Previous Previous post: These Top Ten Mid & Small Cap Stocks Have Given 300%+ Gains In FY15. Do You Have In Portfolio? Leave a Reply Cancel replyYour email address will not be published. Required fields are marked *Comment * Name * Email * Website Current ye@r * Leave this field empty