@Amit2saxena

thanks for your message. In my opinion, the SEZ dedicated building are not attracting new tenants as they are not getting tax incentives. So only limited ITES related export service providers would be looking at that office area. As a result, the occupancy in SEZ for Embassy as well as Brookfield was lower than average occupancy.

While based on my understanding from con call, I understand that in Bangaluru office, Embassy was able to get approval for buildings denotification. However, now floorwise denotification from SEZ would provide better planning of SEZ area (consolidating SEZ clients in specific area) which would release new area for general purpose which would improve occupancy in medium term.

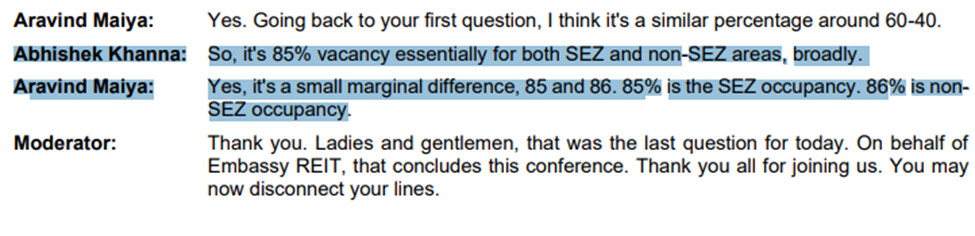

The problem is existing tenant would be seeing tax incentive being not avaialble and may not be keen to renew the lease. At the same, since the area is notified as SEZ (which mean can not be used for domestic market services and shall be exclusively for the exports), demand from new tenants (with no new tax incentives) is very low. Hence, occupancy in SEZ office was higher than non SEZ area. As per Q1FY24 con call, find enclosed management comment on same.

Dislcosure: Embassy REIT is the second largest holding in my Debt/Hybrid portfolio. I have traded in Embassy REIT during last week to benefit from major price decline in 6 December 2023. My view may be positively biased due to my investment. My understanding on REIT instrument structure and market may be wrong. I am not reommending any investion actions to reader, I am not SEBI registered investment advisor.

| Subscribe To Our Free Newsletter |