MONEY BOX

ABOUT

Moneyboxx Finance Limited, having its registered office at New Delhi. The Company is registered with the RBI as a NBFC. The company operates in the unsecured business loan segment, and had assets under management (AUM) of INR530cr (as on 31st dec2023), With 97 branches with 1165 employees, spread across 8 states (RJ, MP, HR,UP,GUJ.BR .CG & PUN) at Dec 2024, located in Tier-2 and below towns, the company caters to micro entrepreneurs operating in essential segments (livestock, kirana, retail traders, micro-manufacturers). The unsecured book (81% of AUM) have an avg ticket size of INR1,40,000 with a tenor of 1 to 3 yrs and the secured book (19% of AUM) have an avg ticket size of INR3,50,000 with a tenor of 4 to 7 yrs

MANAGEMENT

Founder – Mayur Modi, Co Founder – Deepak aggerwal

Linkden profile – https://www.linkedin.com/in/deepak-aggarwal-0511043/ (Deepak)

MAYUR MODI – MONEYBOXX FINANCE LIMITED | LinkedIn (Mayur)

CHIEF RISK OFFICER

Linkden profile – https://www.linkedin.com/in/vikas-b-7ab78b7/

CREDIT UNDERWRITING

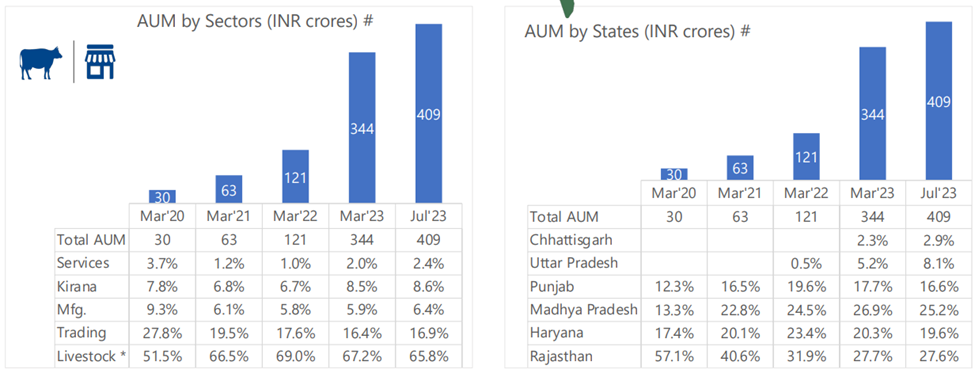

They lend to the essential segment with avg ticket size of 1.25 to 1.5 lakh. Their segment wise AUM in different geography is as follows

1.During FY20 to FY22 which was supposed to be the worst period because of covid and on top of this the Lumpy Skin disease (A lumpy viral skin disease which effects the cattle) they still managed to have a 2-3% credit cost at 30% yield. On a static pool FY20 delinquency was 3% and 2.4% in 2021.

2.They have a proprietary system in which they enter 200-250 points and create the entire balance sheet, P&L statement, whole income statement and cash flow analysis of the borrower. They do this even for a ticket size of 70000.

3.They only lend to customers with self-occupied residential property, they don’t lend to migrants, so this helps them know their relatives, neighbours also this tell they are living in the country since birth (permanent establishment)

4.They don’t lend to single income, 99% of their customers have agriculture as a second income, they look for at least double to triple source of income. In livestock it has to be minimum 5+ cattle with the borrower.

If you think of this point, cattle business can be done from your home, so this is generally done by the women and this is like a second or their income to the family.

5 They have a central credit team in gurgaon where all the loan approval takes place, even a 70k loan, so each branch does not have the authority to approve a loan

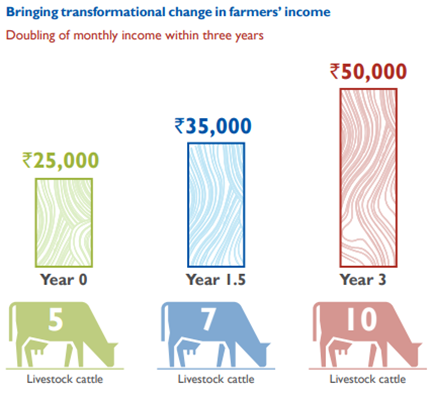

6.They always try to get the women as a borrower and create a joint liability when lending, 55% of their borrowers are women and 34% are new to credit. They help their borrowers double their income in 3yrs.

7.They loan officer who does the sales also has the responsibility to collect, this help him know the exact status of the borrower, this does not happen with most of the lenders where the sales and collection team is different. The company’s business model relies 100% on in-house sourcing and collection and hence requires on ground effort.

8.For Cattle borrowers they have hired vet doctor at their branch and provide free services to monitor the health of cattle. They help in cattle management, feed stock, vaccination drives. Having Vets help money box borrowers tackle the lumpy virus problem. 259k ++ free cattle diagnosis done.

9 They help their borrowers plant fruit bearing trees through CSR activities for big corporations, this helps in increasing the second income of farmers and builds a relationship. 12000++ Fruit bearing trees planted

10 Any branch whose 30 day DPD crosses 2.5% of either branch AUM or loan officer AUM (who manages the entire portfolio from sales to collection) then that branch incentives until all the collection is done is stopped

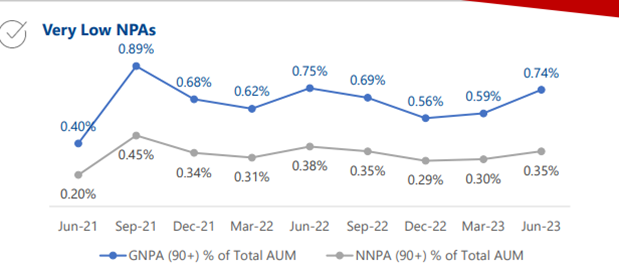

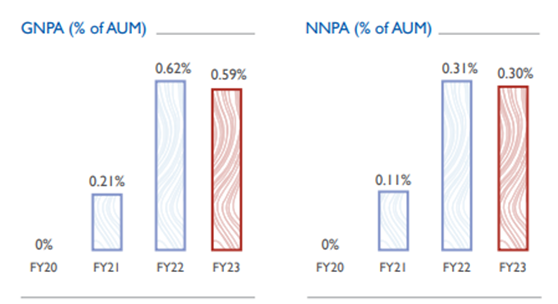

Current GNPA is 1.51% and NNPA is 0.94% this has deteriorated but the management has guided for 2% credit cost so not a surprise with the kind of growth they are doing and this is still best in class in the industry. Need to look watch these numbers closely

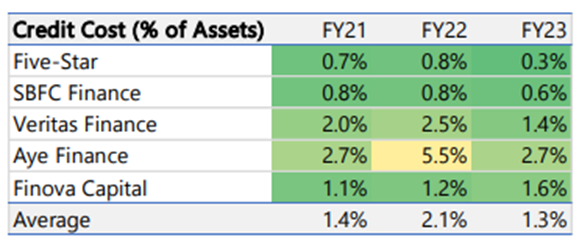

Credit cost of competitor’s

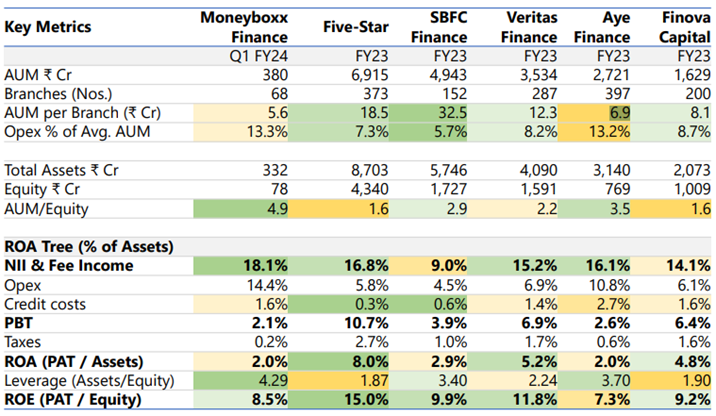

Aye is the closest comparable with MB having the closest gearing to MB and unsecured being the significant portion of total AUM .Moreover Aye also deals in the livestock segment , we can clearly see the difference in underwriting when compared to Aye. The secured guys like Five star have the problem of having almost 5% to 10% of the 30 day DPD bucket whereas MB almost has a NIL here as well.

Lets understand Average cash flow of a livestock borrower

- Their Average Ticket size is 1.5lakh, on an average their borrowers have 8 cattle so yearly income from cattle is 4.2lakh and 99% of them have agri income on top of this. Now they end up paying 15% or so (as interest, plz note every month principal is being paid back) in the entire 2yrs tenure they end up paying 1.8l to 2l approx. So from livestock every year I have 95k (interest + principal) of outflow and 4.2l of inflow.

Please note – these are rough calculations to give a border perspective based on average numbers given by the company, I might make no sense here and might be wrong as well

LIABILITY SIDE

Debt side

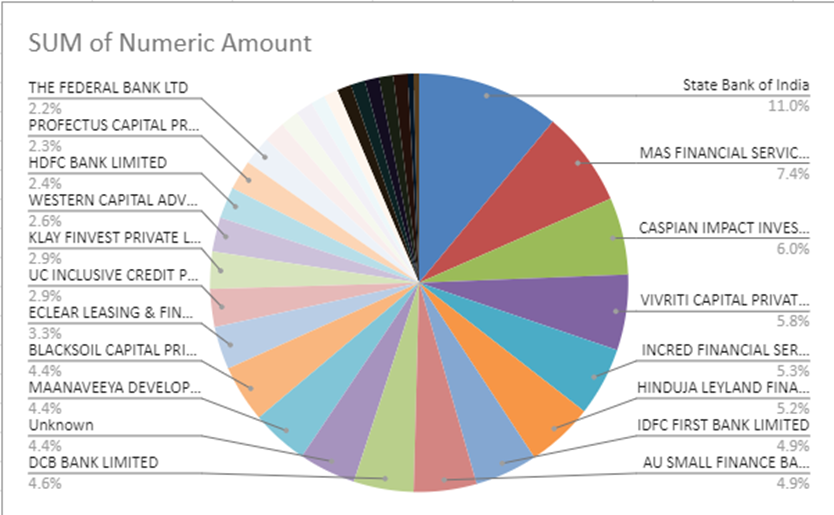

1 They have a total of 31 lenders which includes 10 leading banks

2 Their lenders are willing to lend them even at 7 to 10x gearing. So at any point they can lend up to 10x of their equity

3 They already have commitments of up to 40cr per month or 500cr per annum lending tie up…

4 DCB was their lender at 60cr AUM, IDFC bank at 100 cr AUM, SBI at 150cr AUM and Tata Capital at 170cr AUM

5 If we notice all the players in this field are unlisted and backed by VC, for them getting money from the equity side is way easier than debt, getting money from marquee lenders on the debt side is a testimony of the quality of business because debt guys have limited upside. The reason they get this support is because they operate at a yield spread of 16% (highest in their space) & a credit cost of 2%, they have clearly found a whitespace in lending.

MONEYBOXX DEBT SIDE

We can clearly see Money box has very diversified and such large lenders at a very small size(430cr AUM). This shows their credibility of their business model, credit cost/underwriting, yield spread etc etc

.

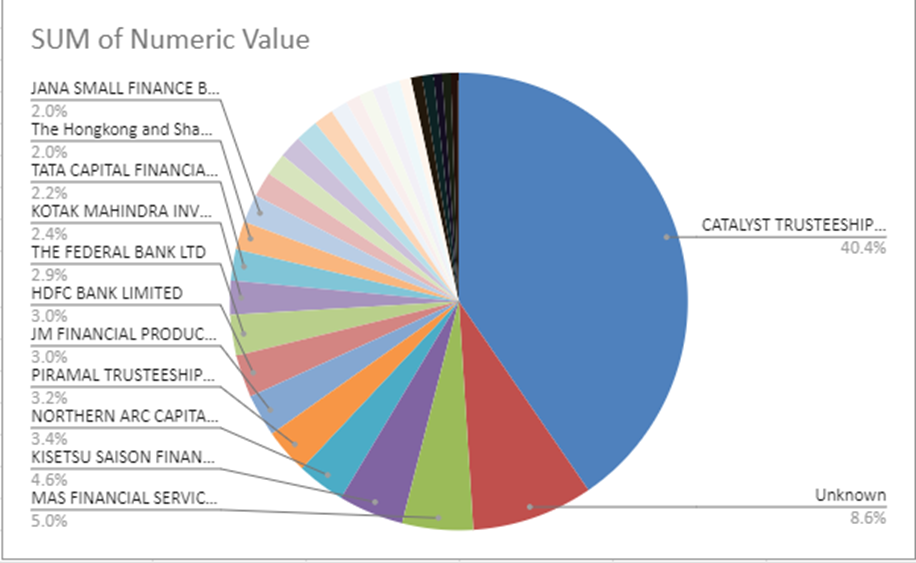

AYE FINANCE DEBT SIDE

AYE finance lenders at almost 3000cr AUM size, we can clearly see MB being almost 6-7 times smaller than AYE has a better set of diversified lenders and they as a % of entire debt are also high. On the other hand these VC backed guys get money from Trusteeships, CAT 1 & 2 easily despite having an inferior business than MB

Equity Side

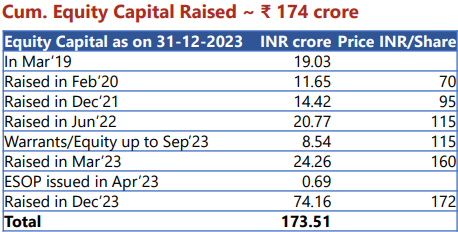

They have raised a total of 93cr out of which 43cr was raised in FY23. They have a target to raise over 100 cr in FY24.

1 Moneyboxx has to approach to HNI, individual investors to raise money for equity whereas All their peers are non-listed companies having investments form CAT 1 and CAT 2, this helped them raise equity very easily, whereas moneybox started as a listed entity because of which they don’t get funding for CAT 1 & 2 and CAT 3 either come in to the picture at 800cr AUM or a 30$ to 40$ million kind of investment.

2 Any delay in money raising for FY24 will not slow their growth because they just need another 25cr total 115cr of equity to reach a size of 800cr or 900cr of AUM and once they raise the money and reach their FY24 targets (800cr AUM, 25%secured etc) subsequent fund raising would become easier. They are confident of raising 100 cr+ by FY24 end.

3 Because of underperformance of UGRO for such a long time investors are sceptical about giving money in listed space but moneybox is not in a hurry they want to raise money at their own terms (5x PB) and they never want to dilute previous investors at a lower price, post this fund raising their new grow journey should start.

Total equity raised by competitor

GROWTH

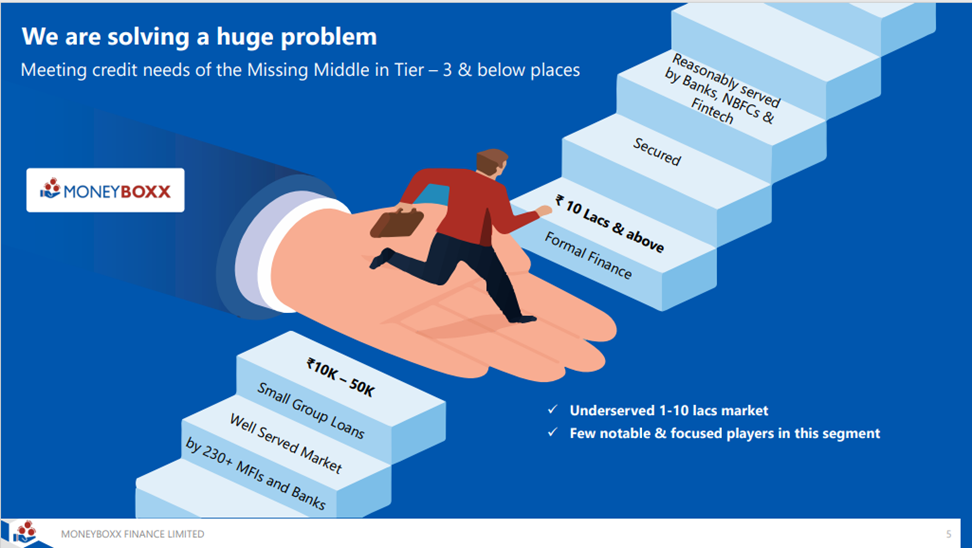

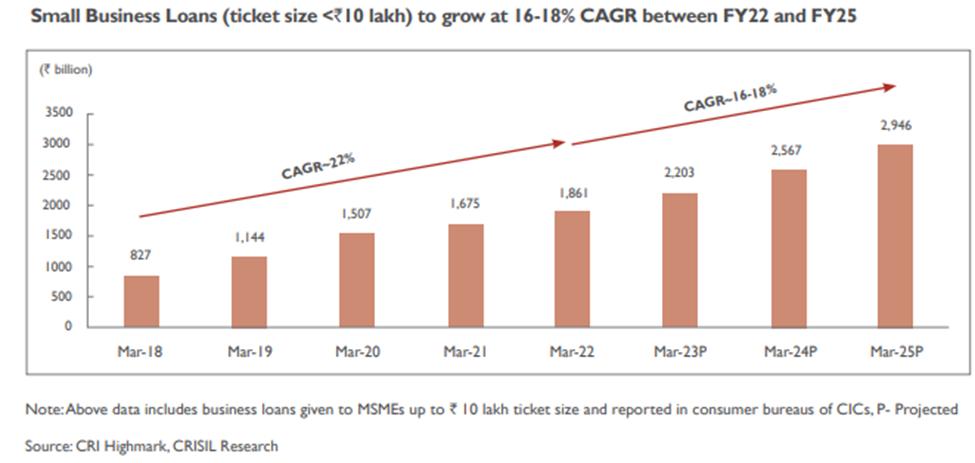

MFI borrowers with average loans under ₹50,000 are adequately served by over 230 lenders. However, these small amounts are insufficient for acquiring income-generating assets or working capital to significantly boost their income. Secured loans exceeding ₹10 lakh are actively pursued by Banks and NBFCs. The unsecured/secured business loans ranging from ₹1 to ₹10 lakh, faces severe underservice due to challenges in income assessment without ITR/GST/Banking/books of accounts, limited credit history, and imperfect collateral. Fintech lenders struggle to serve this segment due to a lack of sufficient data and a minimal digital footprint. Addressing this issue necessitates a physical presence for understanding borrowers, their cash flows, and effective underwriting and collection efficiency. This segment presents a substantial market opportunity. Source- AR

Crisil says 22L cr market is relatively unserved in the Tier 3 & below segment. Digital lenders not able to enter that space

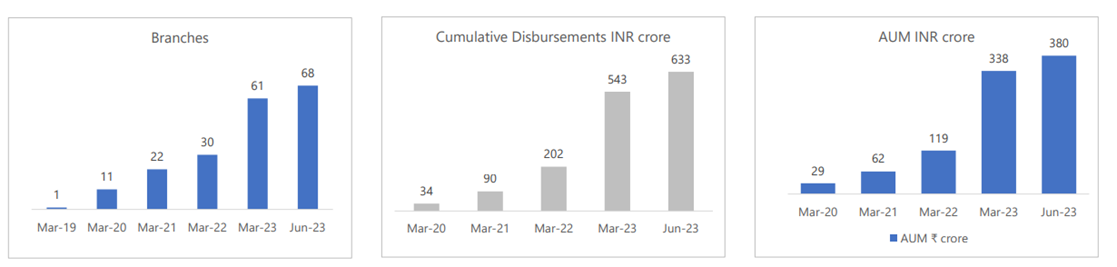

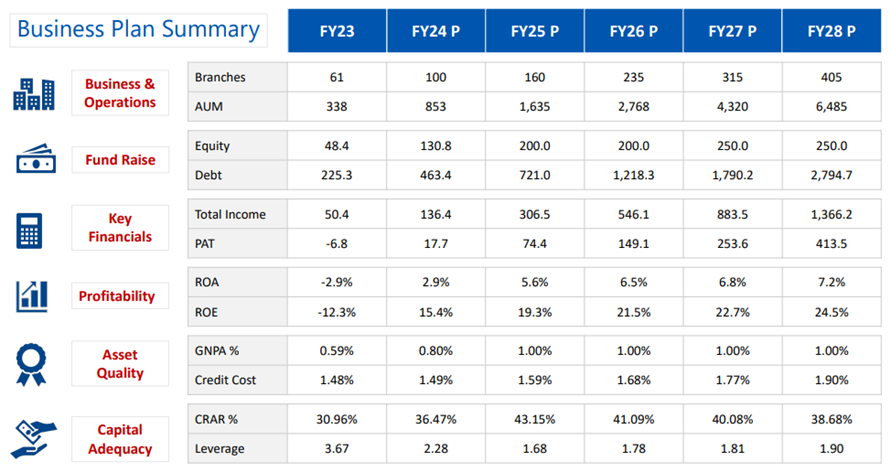

Growth which MB has achieved till now

Future plans

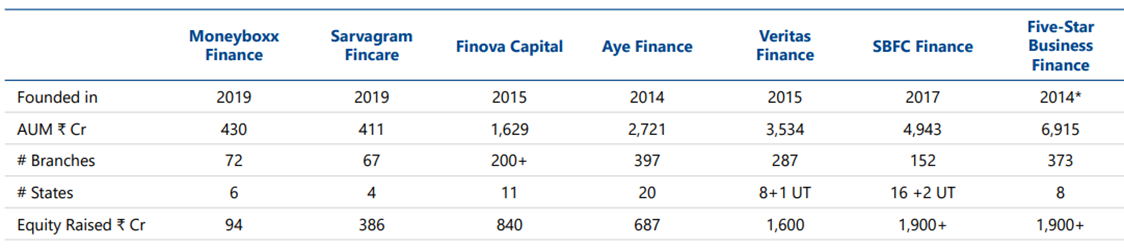

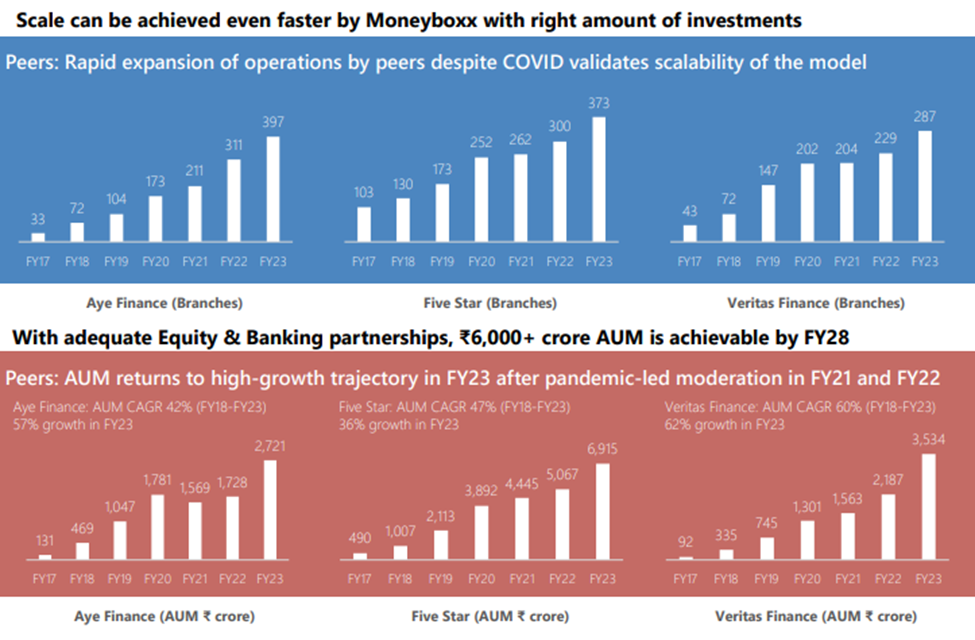

Very scalable business model, growth of some of the peers is as follows

:

The key to a good sustainable growth is good underwriting and strong liability franchise, we have already seen the credit underwriting and debt side. This FY24 equity raise and they achieving the FY24 targets would build a confidence in investors at different levels which would help them in future equity dilution.

Employee growth over the years

As on Jan 2024 – 1165

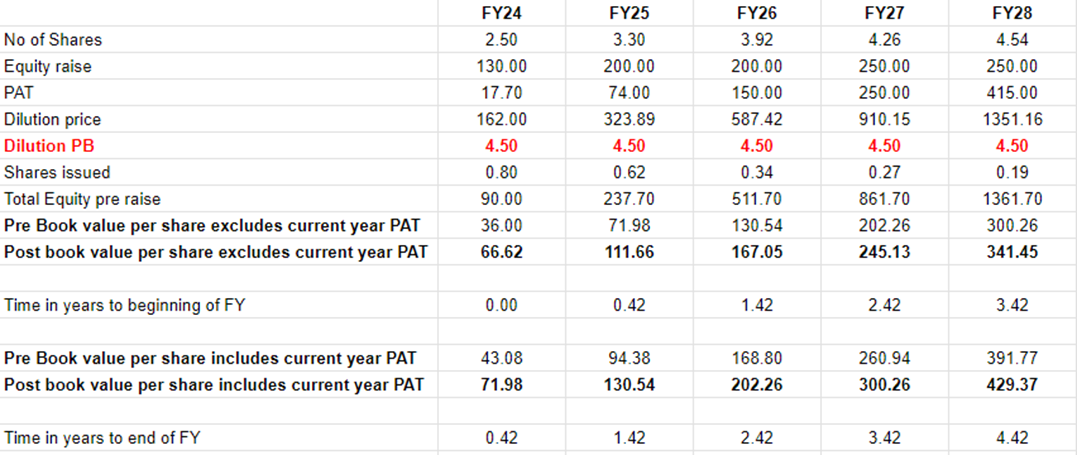

Pre and Post book value per share year wise if executed as guided

Share price CAGR of few competitors

Profitability ROA/ROE

-

Money box has one of the best yield spreads in the industry. They lend at 30% yield and borrow at 14%, with scale and having a PSL portfolio the cost of borrowing is expected to come down to 9%-10% in future. Secured loan is 19% of current AUM and they plan to take it to 25%-30% by FY24 and 50% in future. With decrease in borrowing cost and more of secured business (this reduces yield) they might still maintain the spread and the credit cost reduces further.

-

Their mature branches are doing a 12% PBT margin, taking 4x leverage on 100cr AUM and 9cr as PAT, they equity comes out to be 25cr this results in a 35% ROE (we know what king of ROE they can do if stopped growing), they are guiding for 5%-6% ROA and 25% ROE in 4-5yrs.

3 Aye is doing 60cr PAT on 3000-3500 cr AUM as on Q2FY24 MB with higher gearing, yield spread and lower cost and identical opex should easily their PAT guidance of 150cr at 2700cr AUM & 250cr at 4300 cr

Competitor ROE

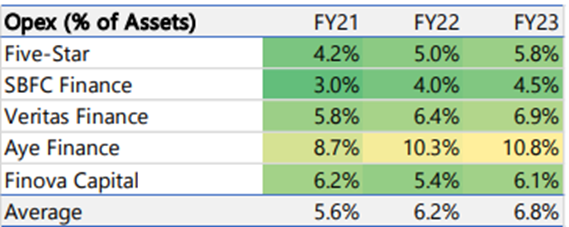

Opex

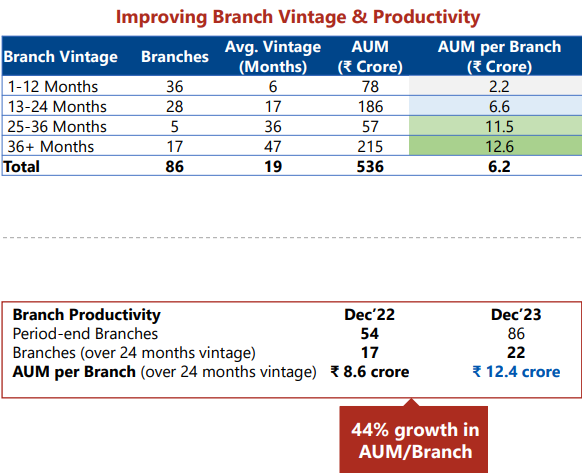

1 It is generally taking 4 to 5 months for a new branch to be profitable; their opex has declined from 25% in 21 to 13% in Q1FY24 and 12% guidance for Q2 FY24. Opex of competitors is below

2 They can scale to 20cr per branch for their older branch with scale, Five star was doing 3.12cr per branch at 64 branches in FY16 (MB has 97 branches) and in FY23 with 373 branches they have almost 18.5cr AUM per branch. MB FY28 Guidance roughly comes out to be 16cr per branch. MB incrementally doing 10cr AUM per branch on more than 12 months vintage. Aye in FY23 doing 7cr per branch.

Disc – Some of the details might not be upto date like the debt side I compared MB and Aye, it was just to convey my point. The company might do another preferential of 150cr (source-todays call at arihanth) post this raise their PB should be around 3 times, in case anybody is interested to take part in preferential you can DM me. Please note I am invested from 172 levels and I might be biased, take you decision after your DD. I have tried to present all the facts above in the best possible way.

| Subscribe To Our Free Newsletter |