JTL Industries

Growth Ahead

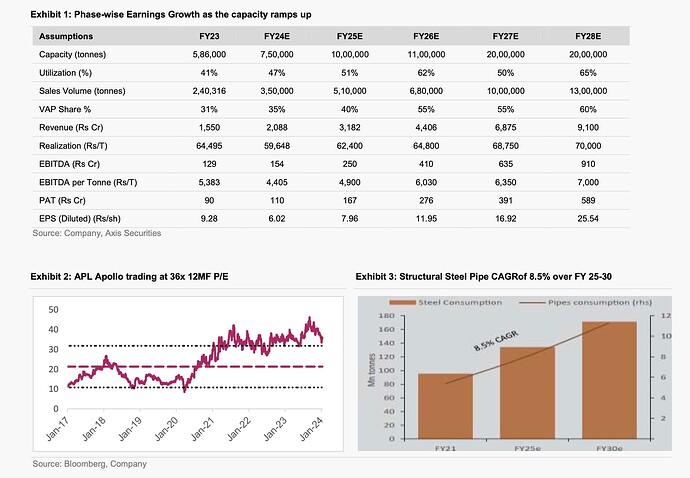

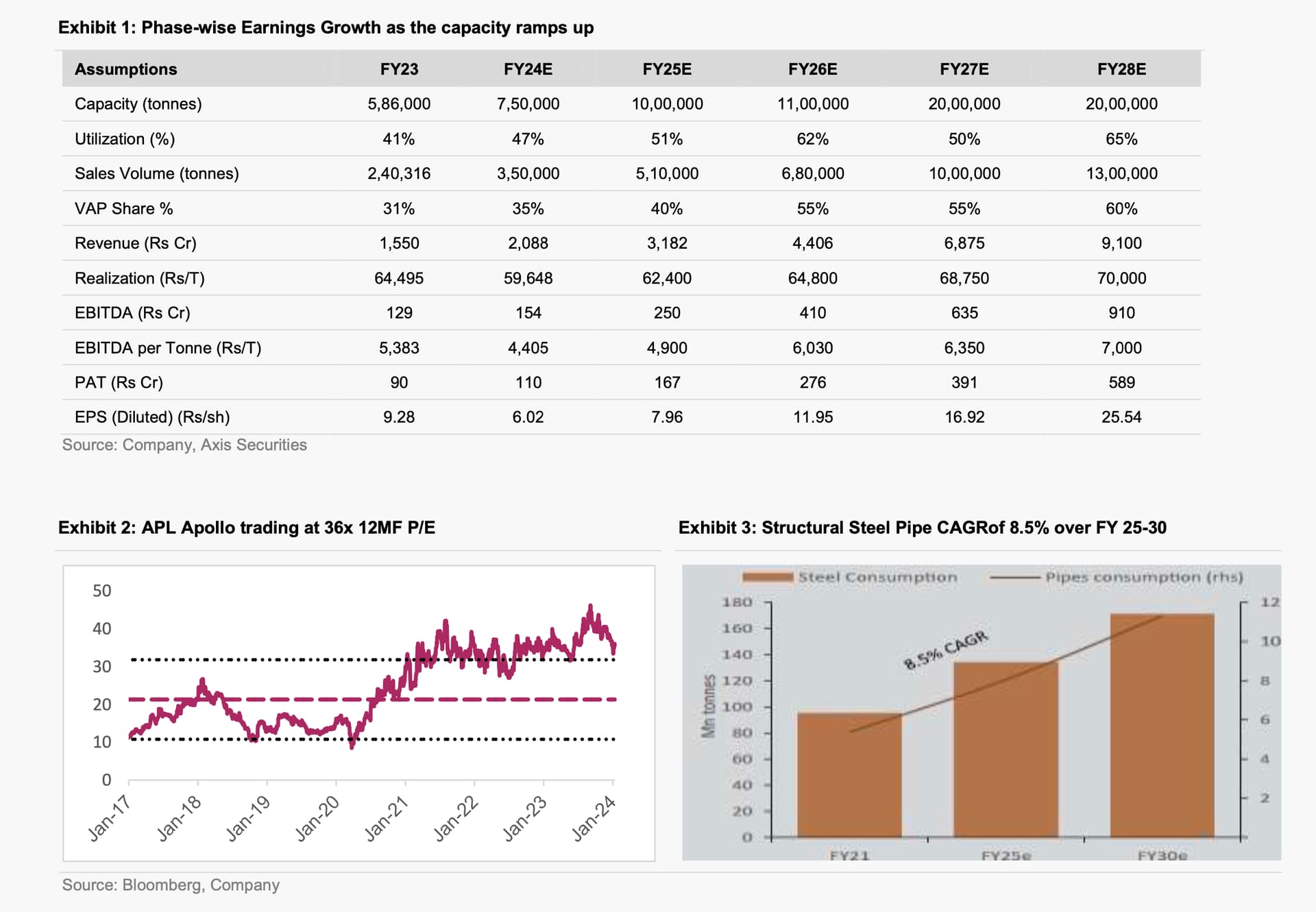

- Company’s announcement in Dec’23 to raise Rs 1,310 Cr to enhance the capacity to 2 MTPA by the end of FY27

- Capacity will reach 2MT by the end of FY27 and full utilization (max ~65% industry standard) on the 2MT capacity will be achieved in FY28

- JTL will enhance its SKUs from 1,000 to 4,000 by FY28 with a focus on VAP (Value-added products). This will translate to ~60% VAP share by FY28 as against 31% as of 9MFY24.

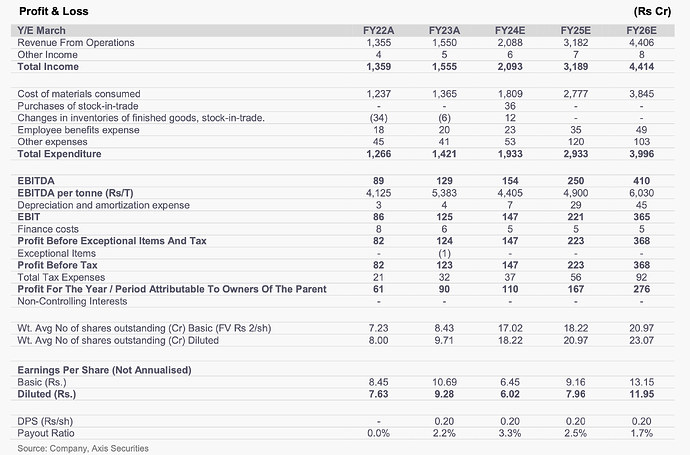

- The newer VAP products will have EBITDA/t of Rs 9,000- 11,000/t, against the general products at Rs 2,000-2,500/t, which will drive the blended EBITDA/t to ~Rs 7,500/t by FY28 (Rs 5,383/t in FY23).

- The expansion plan from 0.56 MTPA to 1 MTPA is on track and will be completed by FY25.

- For the next 1 MT incremental expansion, JTL will focus on enhancing its product profile by adding more DFT lines, introducing color-coated products, and pre-galvanised sheets

Company Outlook & Guidance

- Sector Outlook: Positive

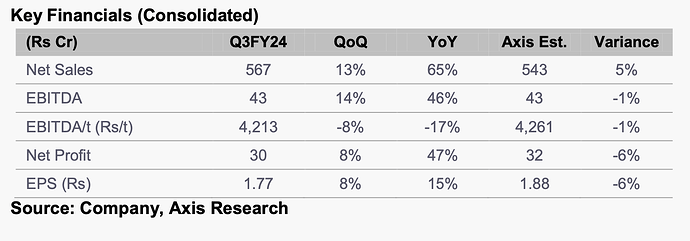

- Post strong Q3FY24 sales volumes, FY24 sales volume to reach ~3.5 Lc tonnes, up 45% YoY, ahead of earlier growth guidance of 30% YoY.

- In Q4FY23, the VAP share could bounce back to 40% (~35% for FY24) from 20% in Q3FY24, as the maintenance of the galvanizing pot is over. 0.56 MT to 1 MT expansion is on track and will be complete before FY25.

- DFT facilities of 2 Lc tonnes out of the total incremental capacity of 4 Lc tonnes will start from Q1FY25.

Concall Highlights Q3FY24

- The company plans to invest Rs 1,200 Cr in its subsidiary company JTL Tubes Limited to set up a Mega Project in the state of Maharashtra at Mangaon. The Capex will be partly incurred from the company’s internal accruals and partly from the proposed issue proceeds (preferential/ QIP).

- In Q3FY24 exports volume stood at 3.6kt, down 19% YoY and 17% QoQ, as the company focused on the domestic market led by strong domestic demand

- JTL currently has 800 dealers pan India out of a total dealer network of 1,000-1,100 dealers, thereby having 80% of dealers catered by it. As more VAP and SKUs share rise in future, more dealers will get on board with the company.

- It currently holds a ~9% market share in the industry and after the onset of the entire 2 MT capacity, its market share will double to 20% by FY28. The market share has moved from 3% in 2019 to 9% in 2023.

- ERW pipes industry is expected to grow at a faster pace than the steel industry at 12-13% in FY24 vs. 10% growth expected in the steel industry.

- Post FY24, the ERW pipes industry is expected to grow by 8-9% for the next couple of years as it replaces traditional long products that were previously used in construction.

Key Risk

- Delay in project execution for the 2 MTPA expansion at the Mangaon Maharashtra plant

- Volatility in the steel prices will drive destocking at the dealer’s end, impacting EBITDA/t.

- Lower-than-estimated demand scenario to hamper the off-take of volumes, impacting our sales volume growth forecasts

Phase Wise Growth at JTL Ahead

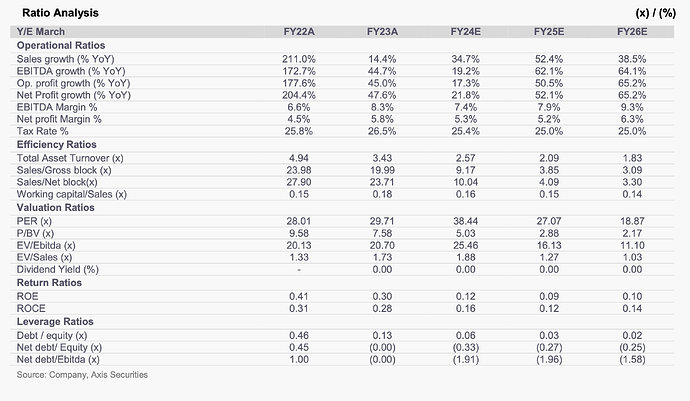

- APL Apollo Tubes, which is the sector leader, is currently trading at 36x consensus 12MF P/E, a premium to its long-term average of 21x given the pace of infrastructure growth in the country.

Disclaimer: Not buy or sell recommendations, only for educational purpose

Invested ~ 8% of total capital @ 190

| Subscribe To Our Free Newsletter |