Rohit Pawar alleges that his rival Ram Shinde has hired a consultant to appeal to youth. Union minister Kirti Vardhan Singh helps free an elephant named Shankar in Delhi Zoo. Bihar Congress invited Haryana leader Bhupinder Hooda as a chief guest for the birth anniversary celebration of state’s first CM Krishna Singh.

Electronics Mart India Limited- EMIL (20-10-2024)

My views on the stock Electronics Mart India (Bajaj Electronics):

-

Electronics Mart India (EMI), a Hyderabad based company. Started in 1980 by Pavan Kumar Bajaj who has no connection with the Bajaj Group’s Rahul Bajaj family.

-

The owner of Bajaj Electronics stores in Telangana and Andhra Pradesh and Electronics Mart stores in Delhi/ NCR region.

-

The largest Electronics retailer in South India and the 4th largest in India, following Reliance Digital, Croma and Vijay Sales.

-

The company launched IPO in 2022 at a price of 60 and now trading at 215. The stock has been in consolidation phase from the last 1 year with a range between 180-240.

-

Market leader in AP & Telangana, and expanding into other areas post IPO.

-

Has a consistent track record of growth, profits and is aiming to add around 25+ stores each year going forward venturing into other states and tier 2 & 3 cities.

-

Their strategy is to enter a market, penetrate deeply and become a market leader which is a strong moat over its competitors. (Similar to DMart’s cluster based expansion approach)

-

My preferred store to shop for any large electronic appliances, bought 2 TVs and 3 ACs and impressed with their customer loyalty.

-

They will match the price to the best price available from the Online stores Amazon/ Flipkart.

-

Have seen 2 new stores opened in my area recently.

-

There doesn’t seem to be any red flags as far as I know.

-

Currently available at fair valuations and is in a consolidation phase since last 1 year.

-

This could be a potential consistent compounding stock for the long term investors.

Disclosure: accumulating in small quantities with a long term view.

CNG price may go up by Rs 4-6 on input supply cut (20-10-2024)

The government has slashed by up to 20 per cent the supplies of cheaper domestically produced natural gas to city retailers — a move that may result in Rs 4-6 per kg hike in the price of CNG sold to automobiles, unless excise duty on the fuel is cut, sources said. Natural gas pumped from below the ground and from under the seabed from sites ranging from the Arabian Sea to Bay of Bengal within India is the raw material that is turned into CNG for sale to automobiles and piped cooking gas to households.

Avenue Supermart: a compounding machine? (20-10-2024)

I think the risks have been mostly factored in the recent price correction. I don’t see any red flags for long term, if the company survives the quick commerce competition it is bound to give decent returns for long term investors.

HLE Glascoat – (Valuation gap with GMM Pfaudler)? (20-10-2024)

What is the actual issue with HLE Glasscoat?

Industry-specific issues (weak demand in chemicals and pharmaceuticals), rising input costs, and possibly a correction after high valuations?

Avenue Supermart: a compounding machine? (20-10-2024)

A great list of all the positive for the company but do you also have a list of risks that the company faces

Amit Singh Learning page (20-10-2024)

Waaree Energies

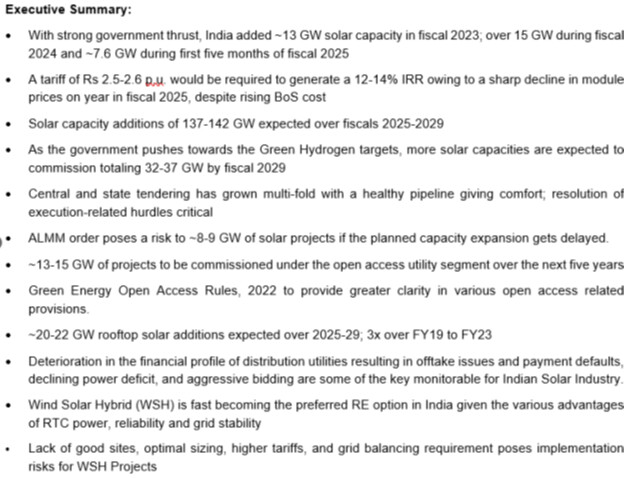

INDIAN SOLAR POWER MARKET

Review of solar energy capacity additions in India

Review of solar energy capacity additions in India

a) About 5,000 trillion kWh per year of energy is incident over the land area.

b) Most parts receiving 4kWh to 7 kWh per square meter per day.

c) The National Institute of Energy estimated the country’s solar potential at 748 GW, assuming solar PV modules cover 3% of the geographical surface.

d) India has 300 days of sunshine each year, with daily peak electricity use being in the evenings and a seasonal peak in the summer.

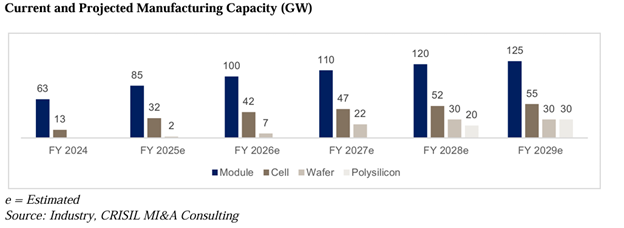

e) Currently, 80% to 85% of the solar modules need be imported as domestic capacity is inadequate to meet demand. India does not have a manufacturing base for polysilicon ingots and wafer; hence, players import these components, incurring high cost.

Waaree business position:

A manufacturer of solar PV modules in India.

- Aggregate installed capacity of 12 GW and utilized capacity of 43.37%, as of and for the year ended March 31, 2024

- Aggregate installed capacity of 12 GW and utilized capacity of 45.01%, as of and for the three months ended June 30, 2024 (on an un-annualized basis).

Solar energy products consisting of the following PV modules:

(i) Multi-crystalline modules

(ii) Monocrystalline modules

(iii) Top-Con modules, comprising flexible modules, which includes bifacial modules (Mono PERC) (framed and unframed)

(iv) Building integrated photo voltaic (BIPV) modules

Operate one factory each, located at Surat, Tumb, Nandigram and Chikhli in Gujarat, India and the IndoSolar Facility, in Noida, Uttar Pradesh.

Total spread over area is 143.01 acres for having 12 GW capacity.

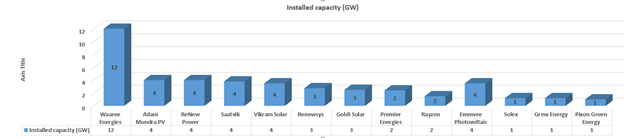

Key domestic solar module manufacturers with capacity

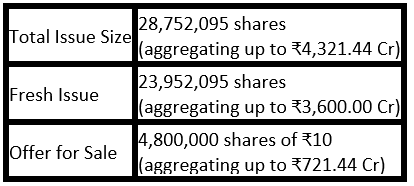

IPO offer size:

|a)|Rs. 27,75 Cr will be used to part finance the cost of establishing the 6GW of Ingot Wafer, Solar Cell and Solar PV Module manufacturing facility in Odisha, India.|

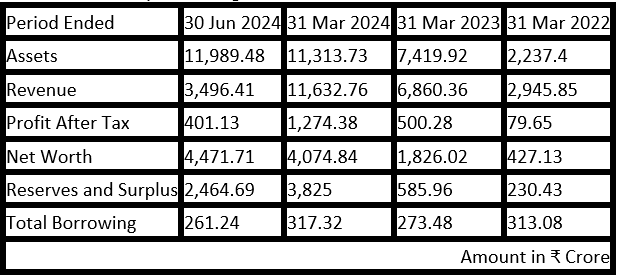

|b)|Waaree Energies Limited’s revenue increased by 70% and profit after tax (PAT) rose by 155% between the financial year ending with March 31, 2024 and March 31, 2023.

|c)|There are no outstanding litigations involving our Group Companies, which may have a material impact on our Company, in accordance with the Materiality Policy.

|d)|Rs. 2033.5 Cr is the estimated amount of contracts remaining to be executed on capital account (net of advance) of the group.|

|e)|Combined Installed capacity is 12 GW but Effective installed capacity is only 3.1 GW and out of this the utilization is only 45% at 1.4 GW production. |

|f)|Cost of Material consumed is in range of 95% to 80% of total expense in Q1 FY25 this is at 60%|

Internal Risk Factors

- Business is dependent on certain key customers and the loss of any of these customers or loss of revenue from sales to any key customers could have a material adverse effect on our business, financial condition, results of operations and cash flows.

- Customer agreements include terms relating to liquidated damages and we have paid liquidated damages and other related claims in Fiscal 2023 and Fiscal 2024 and the three months ended June 30, 2023 and June 30, 2024. In the event waaree is unable to reduce such liquidated damages and other related claims their business, financial condition, results of operations and cash flows may be adversely impacted.

- Export sales make operations subject to risks and uncertainties of various international markets, in particular the United States. Further, revenue from operations is significantly dependent on export sales and there is no assurance that they may be able to continue our export sales going forward.

- Chikhli has 9.66 GW of Mfg base alone.

- Decline in the price of solar PV module prices may have an adverse impact on our business, results of operations and cash flows.

- Transportation freight, duty & handling charges is 3.32% of Revenue from Operations in Q1 FY25.

- The Exports sales in Q1 FY25 has reduced by 45%.

- Other risks in RHP

Number of employees in Company:

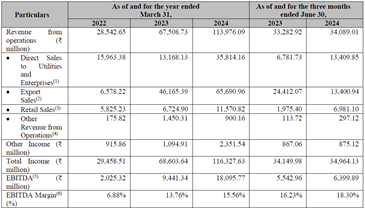

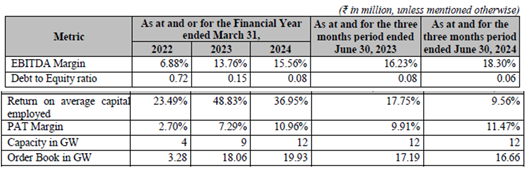

Key performance indicators (“KPIs”) for Waaree Energies:

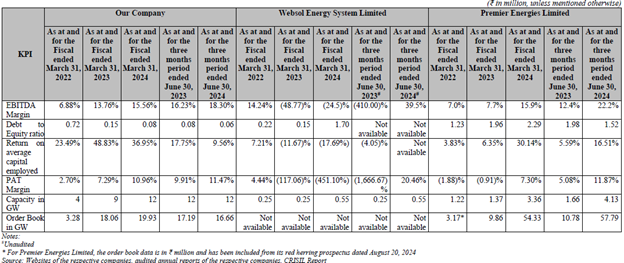

Comparison of KPIs with other listed industry peers:

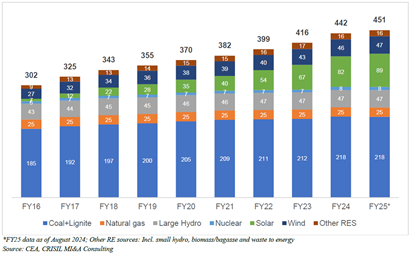

Fuel-wise installed capacity in past 10 years (GW)

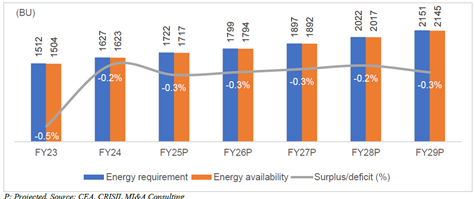

Energy demand outlook (Fiscals 2023-2029)

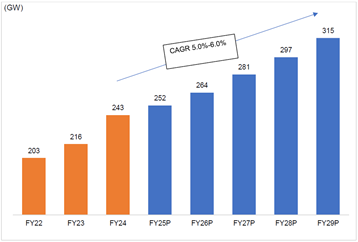

Peak demand outlook (Fiscals 2021 to 2029)

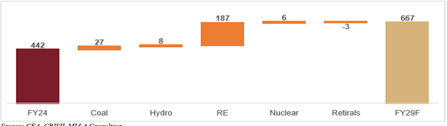

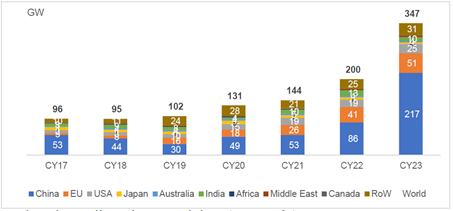

All India installed capacity addition by Fiscal 2029 (in GW)

Annual solar capacity additions in major economies

IRA to boost demand for solar value chain in US

The US Inflation Reduction Act has allocated approximately US$ 400 billion for clean energy. It is expected that it will lead to critical implications for climate change, trade, security, and foreign policy. The tax credits provide financial incentives to both domestic solar demand and supply.

For solar modules the credits are expected to include:

Solar Cells – 4 cents per WDC capacity

Solar wafers – $12 per square meter

Solar grade polysilicon – $3 per kilogram

Polymeric backsheet- 40 cents per square meter

Solar modules – 7 cents per WDC capacity

China Plus One strategy

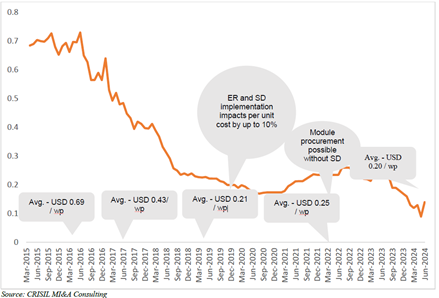

Decline in the prices of Modules

|a)|Module prices started to fall in 2023 owing to the ramp-up in the production of upstream components.

|b)|Prices of modules fell to $0.15-0.20 per watt-peak in April-November 2023 from $0.23 per watt-peak in January 2023. |

|c)|This has eased some pressure on capital costs in Fiscal 2024. Global solar module prices have reached a historic low, standing at just $0.09 per watt-peak in June 2024, which is expected to stimulate growth in solar power capacity. |

|d)|Prices are expected to remain stable over the medium term due to supply glut and relatively weak demand internationally. |

|e)|In line with this trend domestic prices too fell to $0.14 per watt peak maintaining a steady premium over landed cost of imported modules. |

|f)|MNRE has reinstated the applicability of Approved List of Module Manufacturers (“ALMM”). |

|g)|ALMM enlisted manufacturers can supply cells and modules to government and government-assisted projects. Projects under open access and rooftop solar by private parties are also brought into the ambit of ALMM. |

|h)|All the fall in prices across the value chain is expected to be arrested in Fiscal 2025.|

Review of project economics and leveled tariffs for solar PV power plants in India

|a)|5 Acre of land is required to install 1 MW of solar park.

|b)|Equipment cost of ₹ 38 million to ₹ 42 million per MW (including DC side overloading at 40%) for a project based on domestic make modules. – Note: the labour cost and other accessories are extra.|

|c)|If the tariff of solar power is Rs. 2.6 P.U then the IRR on investment is 12-14%.|

Waaree Energies business Forecasting

| All Data in Rs Cr otherwise stated | FY25 | FY26 | FY27 | FY28 | FY29 |

|---|---|---|---|---|---|

| Solar Module in MW (business growth at 20% Y0Y) | 5600 | 6720 | 8064 | 9676.8 | 11612.16 |

| Revenue (@ Rs. 2.435 Cr per MW) | 13636 | 16363.2 | 19635.84 | 23563 | 28275.6 |

| PAT @10% | 1364 | 1636 | 1964 | 2356 | 2828 |

| No of Shares post listing | 28.73 | 28.73 | 28.73 | 28.73 | 28.73 |

| EPS in Rs | 47 | 57 | 68 | 82 | 98 |

| PE @ 50 | 2373 | 2848 | 3417 | 4101 | 4921 |

IPO offer price of Rs. 1503 per share is value for money.

Disc: Invested

Union Minister Kishan Reddy accuses Telangana CM Revanth Reddy of ‘anti-Hindu attitude’ (20-10-2024)

Union Minister G Kishan Reddy accused Chief Minister A Revanth Reddy of an anti-Hindu attitude after police lathicharged peaceful protesters against idol desecration in Secunderabad. Those arrested allegedly desecrated a temple idol, triggering protests by Hindu groups. Police claim protesters turned aggressive and had to be controlled.

Avenue Supermart: a compounding machine? (20-10-2024)

My views on DMart:

-

Avenue Supermarts (DMart) came out with an IPO in 2017 with a price band of 299 and got listed around 616, giving IPO investors more than 100% returns. Since then the stock rallied to an all time high of 5485 and currently trading at 3986 with a 27% discount from its recent high.

-

DMart operates in a high growth retail sector and hence commands a high PE close to 100. The stock had a median PE of 125 since its listing and the lowest PE was around 90.

-

Currently it is trading at a PE of 96, indicating a limited downside and a huge margin of safety. This is a consistent compounding high quality stock, which provides a strong value buying opportunity during significant corrections.

-

The promoters hold 75% of the shares, while FIIs own 10% and DIIs own 7%, CEO owns 2% and the rest 6% is owned by retail investors. There is low free float available in the market hence the stock price is not prone to much volatility unless there are big transactions from FIIs or DIIs.

-

The promoters have not diluted the stock since IPO, not taking any Dividends and investing the entire profits for growth and expansion which shows their strong conviction and commitment to the company.

-

The company has consistently been adding new stores in the last 10 years and been growing revenues at a rate of more than 25% CAGR since inception.

-

DMart currently operates around 377 stores across India and is aiming to add 40-50 stores per year. With strong presence in Maharashtra (112), Gujarat (61), Telangana (42), AP (37), Karnataka (34), TN (23), MP (22), RJ (17) Punjab (13), NCR (9) & others.

-

Remember that Walmart operates 10,500 stores across the world while it operates 4,600 stores in the US with a population of 330 Million, imagine the growth potential DMart has by operating on the similar business model.

-

The company’s unique selling point (USP) is its huge land bank in major metros and tier 2 cities, it owns and operates the stores which saves a lot of lease rental expenses. Also focusing on improving its e-commerce app DMart Ready.

-

It follows a cluster-based expansion approach for penetrating areas where they are already present, before expanding to newer regions, this provides a huge competitive edge. (EMI – Bajaj Electronics allows follows the same approach)

-

The stock has recently corrected by 27% within a month, since the growth has slowed down in the recent quarter and the company acknowledged that its large stores in the tier-1 cities are facing competition from the quick commerce companies.

-

Quick commerce companies are currently trying to match the prices comparable to the retail stores along with free deliveries in 10-15 minutes. For this they need to burn huge VC money for rapid top line growth and exploit manpower.

-

I believe this is an unsustainable business model, once the VC money inflow stops they have to hike prices to become profitable to survive. Once the prices are no longer matching the retail stores their business declines and may get acquired or go bankrupt.

-

Groceries are essential commodities which have very thin profit margins, unlike food delivery business where the margins are high. Zomato and Swiggy have already burnt their hands in the food delivery business and learnt that’s not sustainable and hence pivoted to quick commerce.

-

With rising food inflation the majority of the population looks to buy groceries on a monthly basis where the provided discounts are high. Only the affluent population looks for convenience over the price which is around 1-2% of the overall population.

-

While quick commerce businesses may continue to exist parallelly but beyond a certain point, their growth would be limited. While the retail stores expansion continues beyond tier-1 to tier 2 & 3 cities.

-

The stock has been consolidating in the price range of 3300-4500 since the last 3 years. Once these fears are taken off it may break this price range and start a new rally, I don’t know when that will happen but when it happens it may provide a 2-3X return from the current levels with low risk/reward ratio.

-

Remember Warren Buffett’s saying – to be greedy when others are fearful. That truly applies to D-Mart at current competition fears and hype created by the Zomato stock rally and Swiggy upcoming IPO.

Happy investing in Dmart ![]()

Disclosure: accumulating DMart in small quantities with a long term view.

BSE, NSE to conduct one-hour Diwali ‘Muhurat Trading’ on Nov 1 (20-10-2024)

The symbolic trading session will be held between 6 pm and 7 pm