From the recent conference calls that I have attended of companies which make Ethanol and/or ENA from grains, I understand that those Managements think that it is highly likely that FCI rice will soon be available. Obviously, none of them stated it as a done deal as no one what’s to second guess Govt policy actions, especially after seeing so many twists and turns, but all of them suggested the same thing. FCI Godowns are full till the brim and there’s hardly any space left for the upcoming harvest. That makes them and me hopeful. If this happens, it most likely will cool down Maize prices as many Ethanol producers would move to Rice, thus reducing demand pressure on Maize.

Disc: Invested. Till announcement comes it’s just a conjecture.

Posts tagged Value Pickr

BCL Industries – Ethanol Pick (Capacity 3.5x in Next 2 Yrs) (15-08-2024)

Ranvir’s Portfolio (15-08-2024)

Sir thank you so much for your detailed reply.Sir i am from a maths background,i learnt economics and investing all by myself through reading various books on investing, accounting, following some good youtubers like- SOIC, Smartsync etc.,reading businesses, PPT and concalls of various sectors etc.Sir i also want to expand my knowledge to other sectors,i read concall and businesses in sector like- Infra, Pharma, Chemicals etc but haven’t got the conviction yet to bet reasonable amount.my question is how you learnt and understand these sectors, if you suggest any resources or anything.At last thank you again sir for expanding my knowledge through your concall summaries.

Recently qualified NISM Research Analyst exam through self study.

Focus Lighting & Fixtures Limited (SME) (15-08-2024)

There is some negative sentiment around the company and its management, particularly concerning their technological claims and receivable days. However, I find that the numbers align with management’s commentary. While there is definitely room for improvement—such as distinguishing inquiries from orders and addressing receivable days more effectively—the situation doesn’t appear alarming.

The company works with channel partners that drive sales, which naturally leads to some challenges in the working cycle. Their business tends to be lumpy, showing significant growth during periods of large orders as they primarily focus on substantial contracts. They seem to take a long-term view, planning from a 3-5-year time frame rather than focusing solely on quarterly performance.

For Q1 2025, we can expect marginal year-over-year growth. According to management, receivables should improve in September and October, but this will need to be monitored closely.

What I find interesting is that everything was fine until the start of July, with the 145-150 level providing good support. However, the company began trading below those levels, leading to larger selling pressure at the start of August, around the 120-125 mark. The selling then intensified, with even larger volumes in recent days.

I believe that every 30-40%+ correction has some underlying fundamental reasons, but in this case, I’ve revisited my initial thesis and looked for recent developments, yet I don’t see anything too alarming that would explain these price movements. I understand the sentiment is weak and there are questions about execution, but such drastic price changes are beyond my understanding.

The only thesis I can offer is that some people made too much, too quickly on this counter. The company was trading at around 4.50 INR in mid-2021, and by the start of this year, it had touched over 200—a whopping 50x return in three years. After consolidating at around 150, the price dropped again to 125. It seems someone decided to cash out and book profits, leading to panic selling among shareholders with similar holdings. Recent buyers, understandably, didn’t want to hold onto a falling stock, especially with the market in turmoil, and within days, the stock was completely decimated.

Disc: This is all just my opinion and limited understanding. It represents 0.6% of my allocation, so there’s minimal bias as well as research. I just wanted to share something odd that I observed during my bi-monthly portfolio review.

Kovai Medical Center and Hospital – Health and Wealth (15-08-2024)

Thanks for posting, this management thinks long term always, everyone was worried with medical college

INOX Wind (15-08-2024)

Q1FY25 quarter conf call was very interesting for me.

A few key takeaways from the conf call, from my perspective:

-

Infusion of 900 crores by IW Energy Ltd. = parent company. Makes company net cash +ve.

-

(Tender) Tariffs have been healthy and quantitative ranging between:

a. INR 3.4 to INR3.5 per unit for central sector wind solar hybrid project,

b. INR 3.6 to INR3.68 for plain vanilla wind

c. around INR 5 per unit for FDRE -

Lease on a rental basis for Nacelle hub manufacturing in Ahmedabad. Cost = 4 crores per annum. Substantial savings on Capex. No capex and only minimal rental payments.

-

Current year execution target is 800 MW for current year and next year is 1200 MW (might revise upwards too).

-

- No changes for FY25 guidance wise.

-

- FY26 might see margin improvements due to cost optimization, operating leverage, a better product mix & no finance cost.

a. From Q2 onwards, if you see, so we will have interest earnings (on the cash balance which we have in our balance sheet today) also, which will negate the interest expenses. So, we’ll have a negligible interest outgo from Q2 onwards.

b. Tax loss carry forward: So, FY’25 and ’26, we’ll be actually paying no taxes on our profits.

- FY26 might see margin improvements due to cost optimization, operating leverage, a better product mix & no finance cost.

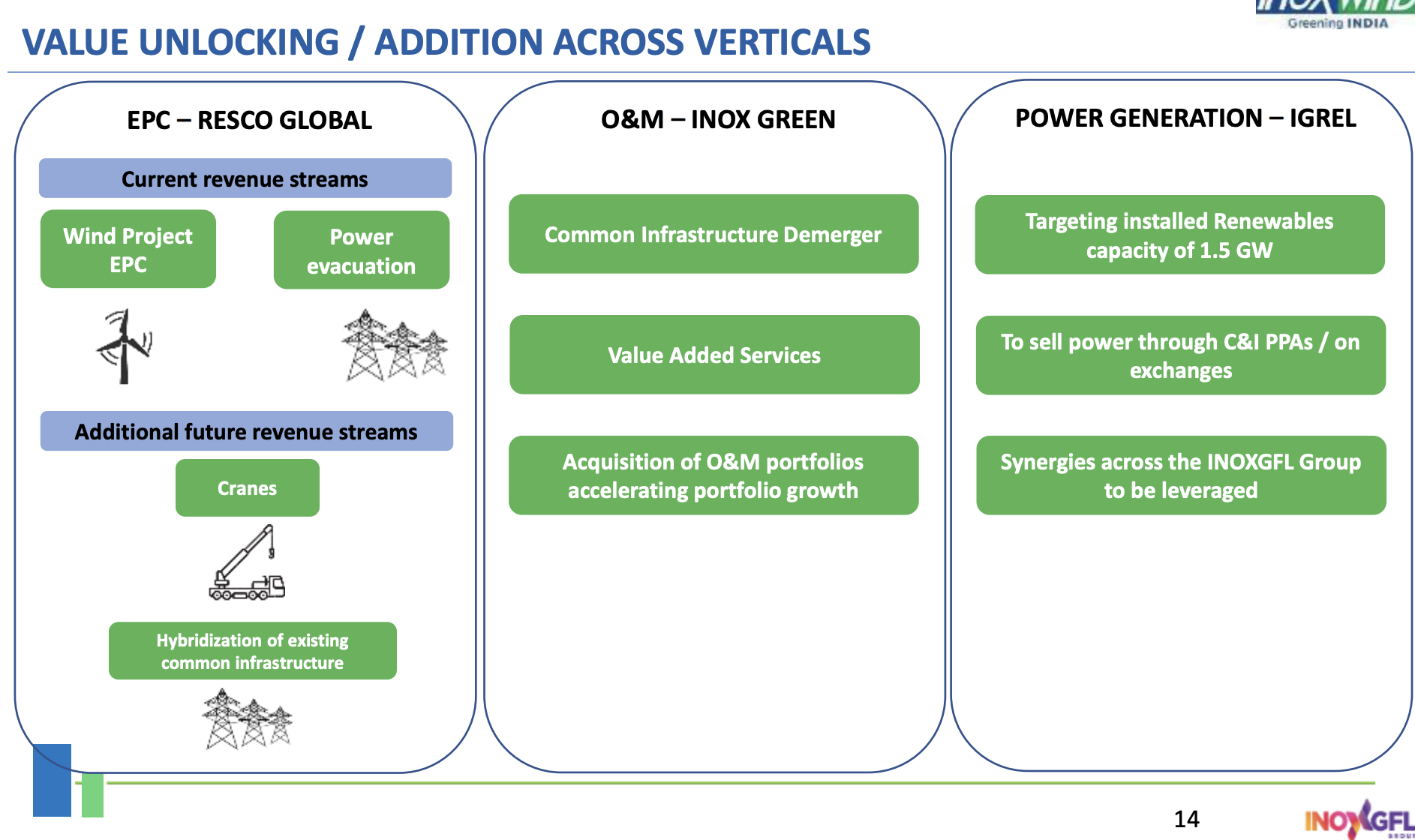

Demerger/ Spinoff:

We are evaluating value unlocking through our EPC arm and also value enhancement through our hybridization of the existing common infrastructure.

Per mgmt, given the multi decadal opportunity ahead:

- at RESCO, it plans to hybridize the common infrastructure like Wind Project EPC, the power evacuation like the substations.

- “backward integrating” – we are getting our own cranes. The returns are phenomenal (30%+)

- (what)we are now doing is given the massive multi-decade opportunity we have ahead of us. We are if I may say so backward integrating into capturing more value within the EPC arm. So we are getting our own cranes. The returns are phenomenal. The payback periods are phenomenal. We are evaluating various other assets to be added within the EPC arm where returns are phenomenal. For example, we buy transformers, our transformers and cable procurement is almost INR400 crores to INR500 crores in a year, given the run rate which we would be on in the coming financial year. We are evaluating whether it makes sense to buy out some of these things to get into it, to manufacture that in-house. Cranes, as I mentioned, is one key area we are anyways moving into internally

- I think we sit on over 5 gigawatts of project site inventory and land bank, which frankly is not given any due importance of value in reality terms, and that’s worth a few couple of INR1000 crores, honestly. So by shunting out the power evacuation from INOX Green, not only do we make the INOX Green balance sheet very light and eliminate the depreciation line, which impacts profitability. But by merging that into the Resco, which is our EPC arm, it leads to automatic listing and creating tremendous incremental value for the larger Inox Wind group. Of course, it’s subject to board approval, but that’s what we are thinking of.

- The company is planning to provide crane services to their existing EPC clients and also rent them to 3rd parties.

Aptus Value Housing : Is valuation justified or just another HFC? (15-08-2024)

Actually Aptus is not great in capital allocation. 1st they raised fresh capital in IPO rather than doing only stake offloading even though their CRAR is crazy high. 2nd, after raising fresh money at high valuation and giving 40% of profit as dividend as if they do not need money.

By giving higher dividend, they themselves are proving capital raise is wrong decision

Aptus Value Housing : Is valuation justified or just another HFC? (15-08-2024)

In my view Avvas Financier’s poor stock performance has been mainly because of high valuations. Until 2 years ago stock used to trade at 6 times book which was clearly excessive given 13-14% ROE of the business. Stock has been in time correction.

Clearly the market is less generous to NBFCs on valuations following RBI’s restrictive policies and higher cost of funds. And none of these small-mid caps NBFCs, Aptus or Avaas, are posting spectacular numbers on your typical parameters such as ROE, NIM, AUM growth etc.

A sane investor will ask as to why they should buy an NBFC at 3-4x book for 14% ROE when they get 16-17% ROE from many dividend paying large private banks current valued at 2 times book.

We’ll have to wait till interest rate cuts and some easing in RBI’s restrictions to see some action in stock prices of these NBFCs.

Voltamp Transformers (15-08-2024)

I compared performance of ABB Power Products (now Hitachi Energy) and Voltamp and the latter has clearly been a better bet.

Since Dec 2020, ABB power products revenue has increased by 70% and earnings only 70%. Despite that stock price has gone up 8x which is not so much due to earning growth but crazy rerating of multiples.

Voltamp has doubled its revenue and earnings 4 times. Stock price has gone up 11x.

On the valuations front, ABB Power is at 250 P/E and 35 times book capping upside. Voltamp on the other hand is trading at 40 P/E and 10 times book and below average industry valuations still gives it some upside despite significant run up.

HUDCO Urban Development – Will it develop the investor too? (15-08-2024)

report HUDCO enclosed

Nirmal_Bang_HUDCO_Q1_FY25_Result_Update.pdf (726.6 KB)

Krystal Integrated Services Ltd – Share Analysis – Facilities Management Services Industry (15-08-2024)

Sorry for the split up. As the Forum post are limited to 40000 character unfortunately i have more than that which not allowed me to post.

Some Q & A, Concall

Training Academy

We have a Krystal Integrated Training Academy which is there one at Vashi. We are going to replicate that in the geographies where we are aspiring to have business.

we signed up an agreement with ITI at Tukkuguda MIDC Industrial Technical Institute and it is a brilliant partnership that we have done there wherein we will train the ITI students in batches at our Tukkuguda office in improving soft skills, interview skills and so on and so forth, CPR, firefighting and all that.

Tax Benefits

The tax rate what you are referring is due to our 80JJAA benefits. So that is the reason why you see our tax components are fluctuating year-on-year.

Receivable Days

Again, receivable days, generally also if you have both government and corporate they are about 70 to 75 days.

Contract Years

This is typically 3+1-year contract, 3-year plus 1 year renewable and after the renewal period then there is a rebidding for that.Some Guidance

- we are going to continue our growth by 25% to 30% year after year . So in that context, if you see the 70% contribution , so that government side will keep on having that contribution. In terms of which are exactly because this is a cyclical process which exactly are contracts which are getting over because they will not get over exactly at the financial year end .

Types of Customers

One is retail, one is key accounts and one is mega accounts .

- Anything which is 10 lakh and less billing for months is retail.

- 10 lakh to 50 lakh three account per month billing

- 50 lakhs and above is major accounts per month billing.

Conclusion

Why would i like to buy this ?

- My Opinion

- Industry is in growth stage – Man power is required everywhere as India is growth stage – Airports, IT Companies and so on.

- Company is in growth stage – Geographic’s expansion, catering growth.

- Very strong presence in One area – Mumbai – Need to track whether they are able to do in Other area too.

Why wouldn’t i like to buy this ?

- My Opinion

- Competitive Industry

- Very low to No Pricing power

- RPT – Related party transactions

- Revenue concentration – Business wise and Geography wise

- Working capital intensity.

My point is not to fill up the page but to provide something which will be useful for us. Please like it and comment for further improvement.