Investment Thesis_BLS international.pdf (734.5 KB)

Posts tagged Value Pickr

BLS International (13-08-2024)

BLS International

Its not a new Movie, it’s a repeat of already played movie

Table of Contents

- What Made Me Look at This Company at First Sight?

- How do I rate this company on different parameters?

- Investment Thesis

- The Story Behind BLS

- Business Model and Innovation

- Market Analysis

- Financial Performance

- Industry Dynamics and Competitive Landscape

- Valuation Analysis

- Risk Assessment

- Appendices

What made me look at this company at first sight?

- Proxy to Travel & Hospitality

- When you want to play proxies, BLS is one of the unique & niche business models that is listed on exchange

- Bridges luxury and essential services i.e. wide array of services to cover the wider spectrum of population

- BLS is probably the only company that provides services to people at the top of the income pyramid and bottom of the income pyramid. This is one of the reasons that subsidiary i.e. BLS E-Services got listed separately on exchange

- One of its Kind Negative Working Capital B2G Business

- Given B2G businesses carry a risk of collections and stretched Working capital, this business has negative working capital.

- Given Indian & Foreign government as its clients but given the nature of services & collection process, this risk is mitigated. There are hardly any receivables on balance sheet

- BLS E-services carries B2G risk but that is getting mitigated as they are charging service fees from end customer now

- Operating Leverage in full swing

- The company has been consistently increasing its EBITDA margins from 15% in 2023 to 27% in Q1 FY25.

- Cash Generating machine

-

60% ROCE (excl. cash) business with negligible leverage on balance sheet

- Company doesn’t need cash to expand organically

- Oligopolistic Industry & High Barriers to entry

- VFS Global commands 50-55% of the market share, while BLS and TLSContact each hold approximately 10-15%. This concentration of power can lead to reduced competition and higher barriers for new entrants.

- Market Opportunity and Growth Prospects

- The global Visa Outsourcing Services market was valued at US$ 3.7 billion in 2022 and is anticipated to reach US$ 8.2 billion by 2028, witnessing a CAGR of 14% during the forecast period 2022-2028.

- Tech Driven & Capital Efficient Business Model

- Asset light model with low CAPEX requirement on tech and physical office infra

- Low-Cost Model

- Like IT Services company, BLS also has a similar advantage. All the support services are provided from India which make it a competitive for BLS international

Video Links:

-

**Company Rating**

| Criteria | Description | Rating (Out of 10) | Comments |

|---|---|---|---|

| Business Model | Evaluation of the company’s business model and market positioning | 8-9 | BLS is a uniquely positioned B2G and B2B business with negative working capital |

| Innovation | Assessment of the uniqueness and innovation of the product/service | 7-8 | BLS is following the best practices and working on enhancing the whole Visa Application process and e-governance services |

| Market Potential | Assessment of market size, growth potential, and competitive landscape | 8-9 | BLS has right to win in an oligopolistic and growing market. Digital services also have a decadal headroom ahead |

| Financial Health | Analysis of revenue growth, profitability, and financial stability | 8-9 | Double digit revenue CAGR and operating leverage in full swing, the company can grow bottom line at much faster pace in both verticals |

| Management Team | Experience and track record of the promoters and management team | 8-9 | Promoters have built the company from scratch. No corporate governance issues yet. No significant RPT. Transparency in report is some that company is catching up on |

| Capital Efficiency | Efficient use of capital and funding history | 8-9 | The company raised xx in IPO in 20xx and hasn’t raised any round yet. Company’s propensity to generate cash is very high |

| Valuation | Comparison of current valuation with industry peers and potential growth | 6-7 | It is available at 19-21x FY26E EV/EBITDA at CMP of 580. Its expensive w.r.t peers but deserves a premium |

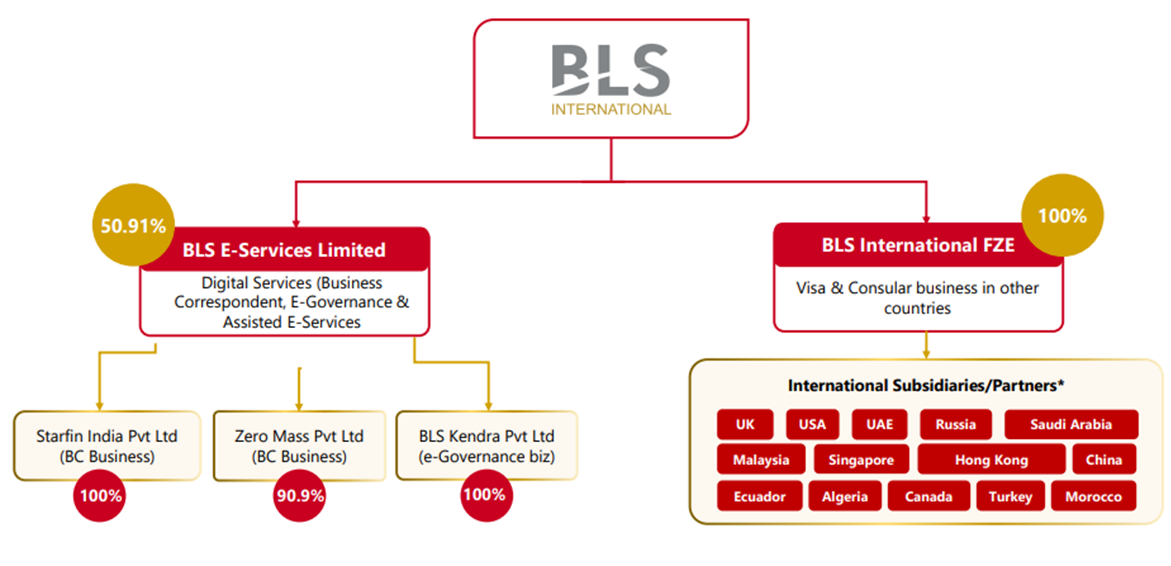

BSL International – 2 distinct companies under 1 Umbrella

Both the companies are very distinct from each other due to the following reasons –

- Are at different stage of lifecycle

- BLS International is much mature than BLS E-services. It is 80% of the consolidated revenue

- Also, management doesn’t want to fund e-services growth from visa business

- Growth prospects and growth levers are different

- BLS international is spread across the globe and has foreign governments as clients. Growth in cross border travel is key lever for growth

- BLS e services is India centric as of now and central/stage govt and banks are customers. More coverage of rural and semi urban areas is the key lever of growth for this segment of business

- Key Inherent Risk are different

Since Inherently, both the businesses are distinct and listed separately (recently), we will discuss the businesses separately

The Story Behind BLS

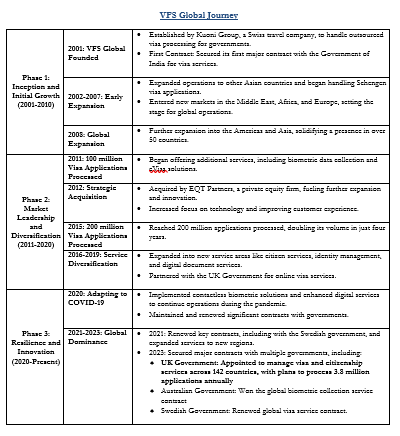

Before we start discussing BLS international, we should look at the journey of VFS global. This will give us an idea of where is BLS placed in the growth cycle.

VFS Global Journey

Key Points to Note –

- VFS was also a 15% EBITDA margin business in Nov 2015 but with economies of scale, its now a 27% EBITDA margin business

- VFS grew acquiring regional players

- Citizen services and other ancillary services is a huge opportunity. E.g., VFS helps with the door-to-door delivery of services in Delhi, sends home birth & death certificates and driving licenses in Mumbai. It also works on establishing the identities of illegal immigrants in South Africa.

- The more data you have for biometric enrollments and other related data, the more you can leverage that data to win more contracts. Note- Data doesn’t belong to VFS

**

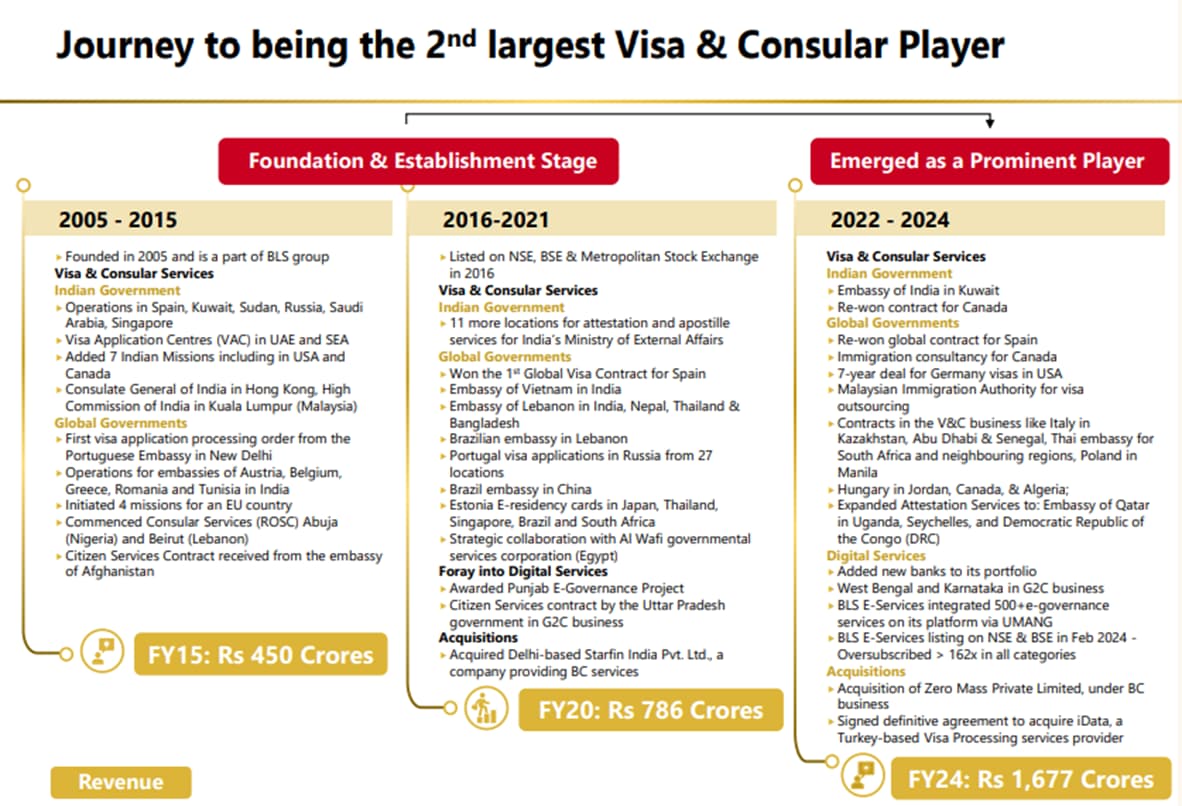

Where is BLS in the journey

**

• BLS seems to be currently in Phase 2 – Market Leadership and Diversification, were

o They are acquiring regional players

o Diversifying into citizen services and other ancillary services

o Changed the business model from partner led office space to own office space

o Improving margins from 15% EBITDA in FY23 to 27% EBITDA in Q1 FY25

o Bidding for new contracts aggressively

Visa & Consular Services

As soon as you start studying this business, you will be able to easily be able to make out few things –

- Industry is Oligopolistic in nature and few companies control the majority of market share

- BLS (being 2nd largest) is 1/3rd the size of VFS global

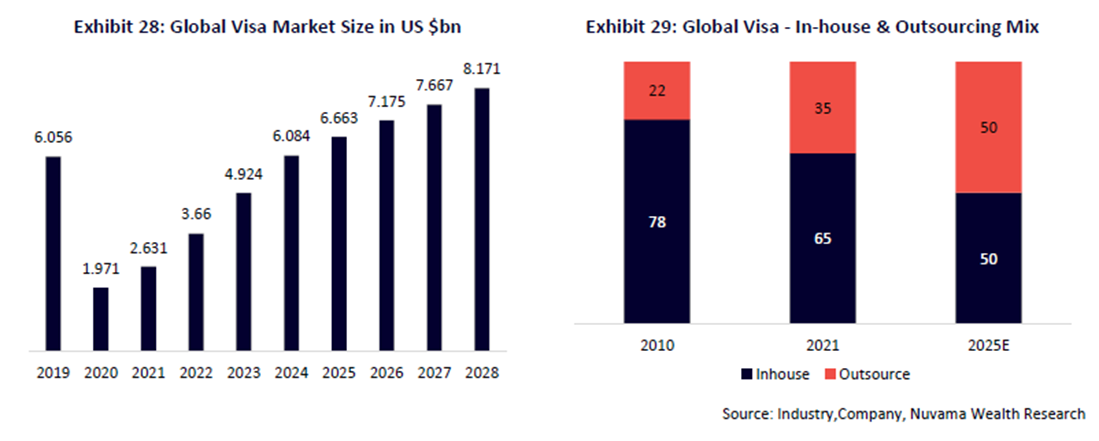

- Global Visa Outsourcing services market size – Market growth of 14% CAGR gives a comfort

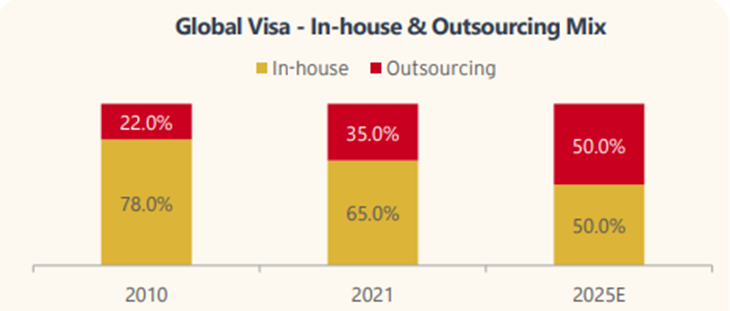

a. This industry, less than two decades old, currently sees only 40% of the total visa market being outsourced, up from 22% in 2010, indicating significant growth potential.

b. The global Visa Outsourcing Services market was valued at US$ 3.7 billion in 2022 and is anticipated to reach US$ 8.2 billion by 2028, witnessing a CAGR of 14% during the forecast period 2022-2028. - Larger players are grabbing market share. There are 2 case studies to prove the same.

a. VFS global – the company has done more than 4-5 acquisitions across the globe in last 5 years to capture the market share

- In March 2017, it took over 100% ownership of its joint venture with TasHeel Group. The JV was the outsourced visa services partner for Saudi Arabia

- VFS acquired Al Etimad, a facility management company that operates 90 visa application centers in 4 countries

- In August 2017, it acquired UK-based visa service provider TT Services

- In 2017, VFS acquired a facility company in the CIS region which operated 550 visa application centers in 8 countries

b. DU Digital Global Ltd – The company has topline of ~INR 29 Cr. The company has just filled a writ petition before the Hon’ble High Court of Delhi. The petition is filed to safeguard against mischievous attempts to scuttle competition and deliberate undercutting and to avail the interim relief.

- The smaller players struggle with profitability at a lower scale. The company has an EBITDA margin of 11%

Investment Thesis

- There are 4 levers of growth for BLS in this business –

a. Consolidation in industry through inorganic route

b. Increase in new outsourcing contracts by new/existing governments

c. Increase the service charge for Visa processing

d. Increase in visa applications processed by BLS

And for now, all the levers are working for BLS international.

o BLS acquired a regional players called iData with the following credentials –

- Turkey based company, founded in 2005

- Provides comprehensive visa processing and consular services to various governments

- Currently servicing Germany, Italy, and Czech Republic consulates in 11 countries

- Operating 37 Visa Application Centres (VACs)

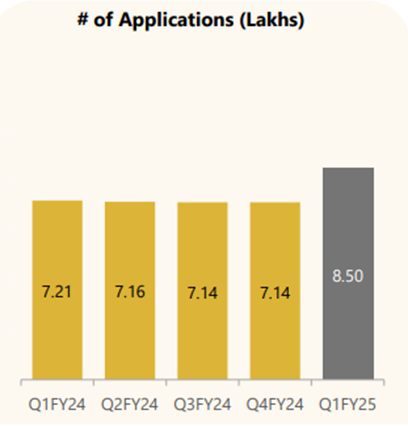

| Particulars | CY2022 | CY2023 |

|---|---|---|

| No. of Applications (in Lakhs) | 5.12 | 7.22 |

| Total Revenue (Rs Crores) | 168 | 246 |

| EBITDA (Rs Crores) | 94 | 144 |

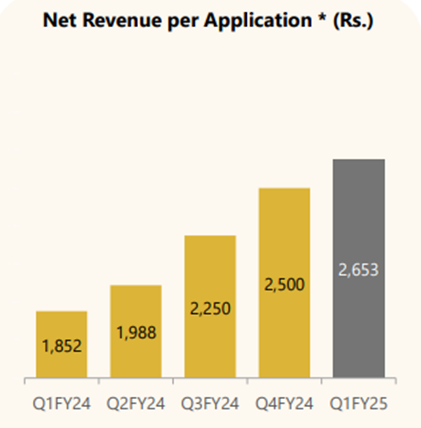

o Due to new contracts won and higher service charges, Number of applications processed and Service charge for processing each application, both the levers are working for BLS International

o Last lever for growth, Growth in Outsourcing of Visa Applicable Worldwide to further fuel up the need for global VISA processors like BLS

Competitive Analysis

Looking at the competition is a major factor in making investment decision in BLS (after iData acquisition)

| Parameter | VFS Global | BLS International (Incl. iData) | TLS Contact | VisaMetric | CSC |

|---|---|---|---|---|---|

| Incorporation | 2001 | 2005 | 2007 | 2005 | |

| Headquarter | Zürich & Dubai | Delhi | Luxembourg | London | |

| Parent | Blackstone | NA | Teleperformance SE | NA | |

| Market Share (outsourced Visa) | ~50% | ~15% | ~20% | ||

| Annual Revenue | $ 700-800 Mn | $ 250 Mn | $ 330 Mn | ~$ 50 Mn | $ 50 Mn |

| EBITDA | $ 180-200 million | $ 60 Mn | $ 85 Mn | ~$ 10 Mn | $ 12 Mn |

| EBITDA % of Revenue | 27% | 21% | 21% | 18% | 24% |

| Annual Visa Applications | ~25 Mn | ~3 Mn | |||

| Visa Applications Processed (Cumulative) | – | 360+ Mn | 6.5 Mn | 7 Mn | 2 Mn |

| Client Govt | 68 | 46 | |||

| Global Presence (countries) | 153 | 66 | 62+ | 16 | 20 |

| Number of Application Centers | 3,500+ | 2,500+ | 1,500+ | 100+ | 150+ |

| Employees | 11,000+ | 60,000+ incl. Associates | 6,000+ | 500+ | 500+ |

| Top Countries | UK, Australia, Sweden, UAE | **Germany Italy Spain****US |

India|France, Switzerland, Italy||US|

|Valuation|$2.5 Bn in 2021|$2 Bn in 2024||||

Management Commentary*

Shikhar Aggarwal; Joint Managing Director

“We have transitioned from a partner-backed model to managing our own operations, a move BLS International Services Limited that underscores our dedication to optimizing performance”

Acquisition

- “A significant milestone in our global strategy was a definitive agreement to acquire a pertinent stake in iDATA, a leading provider of visa & consular services based in Turkey. This strategic move aligns seamlessly with our objective and is expected to enhance our market presence substantially”

- “We’ll continue to focus on our inorganic growth initiatives, wherein we would be targeting synergistic tech-enabled businesses.”

Annexure

**BLS E-Services**

Shikhar Aggarwal; Joint Managing Director

-

“The funds raised (INR 300 Cr through IPO) will fuel the expansion of our digital service arm enabling investments in new technology, service offerings and outright efforts”

-

“Partnerships with public and private sector banks exemplified by initiatives like Har Ghar Suraksha and DBS Dastak underscore our commitment to extending banking services to the underserved population of the country. Our innovative solutions such as the Business Facilitator model and Iris scanner have been instrumental in driving success and delivering value to our partners”

-

“We have recently launched doorstep banking services tailored for the elderly in 25 states and

-

union territories, making banks more accessible and convenient for them. This service aims to

-

address the challenge faced by elderly in accessing traditional banking facilities. Looking ahead,

-

BLS International Services Limited we are focused on organic growth initiatives and strategic acquisitions to expand our market share and strengthen our competitive position.”

Acquisition

“We signed a definitive share purchase agreement to acquire 55% controlling stake in Aadifidelis Loan Solution and its affiliates, which is one of the largest loan distribution processing companies in India with Pan-India presence. Anetwork of 8,600 plus channel partners enabled Aadifidelis to facilitate average monthly loan disbursement of more than INR1,500 crores”

- “On the digital service front, we secured a significant contract from state health agency Ayushman Bharat, Pradhan Mantri Yojana, Uttar Pradesh. This partnership involves handling of Ayushmann cards on behalf of the National Authority IT platform.”

- “Being chosen as being chosen as a Empaneled Service Provider reflects based international reliability in delivering crucially, governance Services.”

- “The company was awarded another significant contract from UIDAI to conduct a comprehensive data quality check for Aadhaar information. The project, spanning over three years, is extendable by another two years”

Key learnings from the Punjab contract

Post the Punjab contract, BLS has decided that it would not pursue any Govt. business where receivables are due from the Govt. The company will participate in contracts only if the revenues are to be collected from Citizens, with a share of revenue going to the Govt.

Post re-contracting of the Punjab contract, the company has entered into two additional contracts with the states of Rajasthan and Uttar Pradesh. In both these contracts, BLS has provided the software necessary to provide services to local entrepreneurs and charges a fee per transaction, making the model even more capital light

Investment Thesis

- There are 4 levers of growth for BLS E-services in this business –

- Consolidation in industry through inorganic route

- Increase in new outsourcing contracts by state/central governments

- Increase the service charge for the services

- Increase in volume of services provided

- Addition of new services to create a complete ecosystem

- Idea to create one stop shop for all services & Eco-system that’s been created, will make this business on the same path to visa services business.

- This business also has potential to generate higher EBITDA margins

- Management has guided for >25% growth in this business for next 4-5 years which is possible by creating one stop shop

- Given the past learnings, Management know how to grow this business vertical

Estimated Financials

| Year to March (INR Cr) | FY23 | FY24 | FY25E | FY26E | |

|---|---|---|---|---|---|

| Income from operations | 1,516 | 1,677 | 2,250 | 2,700 | |

| Cost of services | 1,029 | 965 | 1125 | 1350 | |

| Employee costs | 140 | 208 | 270 | 324 | |

| Other expenses | 125 | 158 | 202.5 | 243 | |

| Total Operating expenses | 1,294 | 1,331 | 1,598 | 1,917 | |

| EBITDA | 222 | 346 | 653 | 783 |

Aster DM healthcare (13-08-2024)

Few of my takeaways from Q1 FY25 of Aster DM Healthcare

𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲:

Aster DM Healthcare’s business outlook appears promising, with the company reporting strong operational and financial performance in the latest quarter. The company’s focus on expanding its hospital network, especially in tier-2 and tier-3 cities, aligns with the growing demand for quality healthcare services in these regions. The management’s emphasis on maintaining sustainable margins and improving operational efficiency suggests a well-planned strategy for long-term growth.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

- Expanding the hospital network through a mix of greenfield and brownfield projects, targeting a total of 1,700 new beds over the next three years.

- Focusing on tier-2 and tier-3 cities, where the company sees significant opportunity for growth and higher margins.

- Optimizing the capital allocation strategy by leveraging existing cash reserves and operating cash flows to fund the planned expansion, without the need for immediate dilution.

- Exploring inorganic growth opportunities, including potential mergers and acquisitions, to further strengthen the company’s presence and capabilities.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

- Increasing insurance penetration and government initiatives, such as Ayushman Bharat, improving accessibility and affordability of healthcare services.

- Growing demand for specialized and quaternary care services, particularly in tier-2 and tier-3 cities.

- Shift towards daycare and outpatient procedures, leading to improved operational efficiency and margins.

- Ongoing consolidation in the healthcare industry, presenting opportunities for strategic acquisitions.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

- Expanding middle-class and growing awareness about preventive healthcare.

- Increasing government focus on improving healthcare infrastructure and accessibility.

- Favorable demographics, with a large young population requiring quality healthcare services.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

- Availability and retention of skilled medical professionals, particularly in tier-2 and tier-3 cities.

- Regulatory changes and pricing pressures that can impact the company’s profitability.

- Competition from other established healthcare providers, both in the metro and non-metro regions.

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Analysts raised concerns regarding the performance of the Andhra Pradesh and Telangana clusters, which have lower margins compared to the company’s other regions. The management acknowledged the challenges and provided a detailed plan to improve the performance of these clusters, including optimizing costs, leveraging government schemes, and building on the company’s existing presence in the region.

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

Aster DM Healthcare operates in a highly competitive healthcare industry, with both regional and national players. However, the company’s strong focus on expanding its presence in tier-2 and tier-3 cities, where competition is relatively lower, as well as its emphasis on specialized and quaternary care services, provide it with a competitive advantage.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

The management has provided a positive outlook, targeting a consolidated EBITDA margin of 20-21% in the medium term and a hospital and clinic segment EBITDA margin of 23-24%. The company’s ability to achieve these targets will be crucial in determining its future performance.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

Aster DM Healthcare’s capital allocation strategy appears prudent, with the company planning to fund its expansion primarily through existing cash reserves and operating cash flows, without the immediate need for dilution. The management’s openness to exploring inorganic growth opportunities, subject to favorable valuations, is a positive sign.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

Key opportunities for Aster DM Healthcare include:

- Expanding its presence in tier-2 and tier-3 cities, where the demand for quality healthcare services is growing.

- Leveraging its expertise in specialized and quaternary care services to drive higher margins.

- Capitalizing on the industry’s consolidation trend through strategic acquisitions.

Potential risks include:

- Regulatory changes and pricing pressures that could impact the company’s profitability.

- Challenges in attracting and retaining skilled medical professionals, particularly in non-metro regions.

- Intensifying competition from both regional and national players.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

The company’s focus on providing quality healthcare services, expanding its presence in underserved regions, and leveraging specialized and quaternary care capabilities suggests a positive customer perception.

Equitas Small Finance Bank: A Profitable lender to small businesses (13-08-2024)

The charts suggests the downside shall continue till 71-72 level since the downward moment has started after breakdown from neck level of the head and shoulder pattern.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (13-08-2024)

Did they give any reason for promoter not being present in the call?

This looks bad. Still, there’s sufficient margin of safety considering the stock price and company’s debt is sustainable and the business is cash accretive so no need to panic just yet.

Did they mention anything about addition of new keys, given the 2,200+ target that they had for FY25? Owner being sick is not a good enough reason, why are they not approaching other owners.

How come they didn’t anticipate drop from election when everyone else was expecting it, are they living with their head in the sand?

Savita Oil Technologies: Undervalued midcap in a competitive space? (13-08-2024)

Sharing the latest investor presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/fe9af0f1-c123-4964-a8a1-216792f89924.pdf

Piccadily Agro Industries Ltd (13-08-2024)

History is irrelevant in this stock given the changing business model. Key question to answer is does USL show a QoQ jump between June & September. Here’s the data:-

| June | September | QoQ | |

|---|---|---|---|

| FY24 | 2,667 | 2,867 | 7.50% |

| FY23 | 2,419 | 2,911 | 20.34% |

| FY22 | 1,722 | 2,508 | 45.64% |

One can ignore FY22 as being marred by Covid wave 2, but FY23 and FY24 numbers are pretty evident.

Also another point on capacity – if one has seen the 40-50 minute video of the tour of piccadily, towards the end you can see that in the new warehouse, whiskey is maturing in new barrels since 2022. So its likely they’ll take some of it out for sale in Q3.

https://www.youtube.com/watch?v=ESC6KU1NaXA – see from 37 min onwards

Madhu in this video says, younger barrles have been purchased “over the last few years”. So whiskey etc / liquid is already maturing in some of these barrels. This is confirmed as you move forward in the video & Madhu shows you barrels that have been stocked since 2022. So its likely some of this extra capacity would be released in the market towards Diwali

If I take a 10% QoQ revenue jump for Piccadily, and around 15% QoQ jump in EBIT, we get 132 crs & 34crs of EBIT for Q2. Q3 and Q4 should be bumper given season + extra capacity + new launches (maybe?)

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (13-08-2024)

Q1FY25 CONCALL NOTES:

- Vishal Kamath (MD) was not available. CFO led the call

- Pune will go under renovation

- Ayodhya and Mumbai are doing exceptionally well

- Other expenses increased from 22 to 30 yoy

- They guided Rs 10 cr only

- CFO said it’s a detailed question and will take later!!

- Int cost will be Rs 5 cr per quarter

- But Maths :

- 115 cr debt @ 10.75% = 3.09 cr per quarter

- Analyst presented this maths, she said yes to this also

- But Maths :

- Will guide next quarter about revenue and ebitda

- “its too premature to comment on this”

- Rs 6 cr lease rental for IRA Mumbai

- 1 cr some fees paid

- 2 cr increase is due to payroll increase due to increase in no. of properties

- New properties :

- Combination of Orchid and IRA

- Chandigarh Property got delayed because the owner was unwell

- They were earlier confident of having Rs 400 cr revenue for fy25 but they didn’t anticipate the decline due to elections

- Analyst explicitly asked them to be conservative with guidance because they miss very often

- The new merger contains a property that is close to sewage treatment plant in Vile Parle

- Analyst said this would add no value to company – so why high valuations of the merged entity?

- Ans : huge land bank – minimum value Rs 300 cr of 1 single land + few more lands

- This was the most messed up call ever.

- People asked about interest cost 7-8 times

- 12 cr renovation cost for Goa

- Another property 12 cr

- Total 24 cr for full yr

- Q1 – they didn’t spend much, only 2 cr

- These go to CWIP

Singer – Possible turnaround a.k.a. Symphony (13-08-2024)

Disappointing set of numbers by Singer India again. But there are clear signs of change happening within the company.

Company has announced ~7x increase in production capacity with only 15lks investment from 90000 machines to 630000 machines!!!

625fc3c7-bf78-4b26-a7f4-ac7f47462de3.pdf (bseindia.com)

As per the filling this is done to increase backward integration and all for Exports.

Singer India Embarks on a Technological Revolution – Indian Retailer

SVP Worldwide To Make India Global Hub For Singer Machines, Plans New Unit (ndtvprofit.com)

“We are looking at Zig-Zag, which is today around 7% of the market. We are expecting this to grow tremendously fast, at a rate of around 50% of growth for…year-on-year for the next three years,” he said, adding, “in the normal sewing machine market, which is rather stagnant and not growing at a high rate, where we are continuously looking at around 10-15% growth for the next three years.”