Appointment of new CEO and COO. Highly experienced, 30+ years, and have previously worked in industry giants.

Posts tagged Value Pickr

Sandur Manganese (05-08-2024)

Sandur Q1 FY25.pdf (1.6 MB)

Q1 Result update

Rajesh’s portfolio (05-08-2024)

Hi @Rajesh_Singh sir! May I learn about your thesis behind Sun Retail Ltd? Because from what I see is, the company is currently loss making and was doing reasonably well until FY 19 but then had been on a constant decline (that too massive decline) and is again gaining momentum (FY 24). Is it a turnaround story or what?

Godrej Properties – Brand, Business model & Scale (05-08-2024)

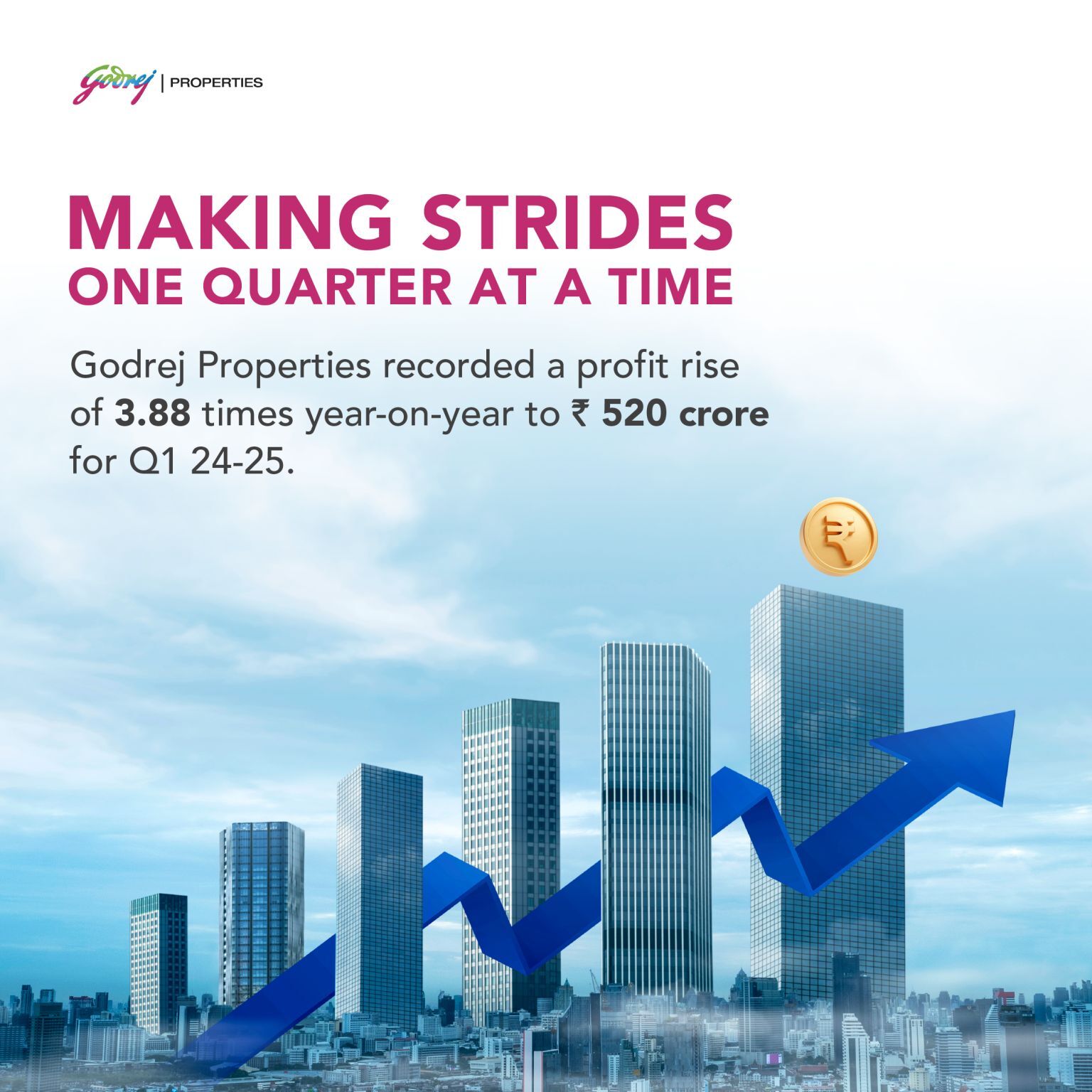

Godrej Properties Q1 FY2025 Analysis: Key takeaways!!

Godrej Properties delivered an exceptionally strong Q1 FY2025, with multi-fold growth across key metrics. The company achieved its highest ever quarterly net profit of INR 520 crores. Booking value grew by 283% year-over-year to INR 8,637 crores, while booking volume reached 8.99 million square feet – the highest among listed developers in India. Management is confident about maintaining this growth momentum through new project launches and strong sustenance sales.

Strategic Initiatives:

- Focus on premium locations and mid-sized projects (10-15 acres) to drive higher returns

- Standardization and centralization of procurement for key materials to achieve economies of scale

- Mix of top contractors for large projects and trusted partners for mid-sized developments to ensure timely execution

- Expansion into plotted developments as a complementary offering, targeting 10-15% of overall sales

- Continued emphasis on business development to replenish rapidly selling inventory and fuel future growth

Trends and Themes:

- Strong demand across key markets, especially for projects by reputed developers

- Price appreciation in most markets, with potential for further increases in some regions like Pune

- Consolidation in the industry favoring organized players with strong brand equity

- Growing importance of end-user driven demand for sustainable sales

Industry Tailwinds:

- Robust economic growth and rapid urbanization driving structural demand for housing

- Low mortgage rates supporting affordability

- Increasing preference for home ownership post-pandemic

- Government focus on housing and infrastructure development

Industry Headwinds:

- Potential cyclical downturn in the medium term (4-5 years)

- Rising input costs impacting margins

- Regulatory challenges and approval delays in some markets

Analyst Concerns and Management Response:

- Execution capabilities given rapid sales growth: Management highlighted investments in engineering capabilities, strong contractor relationships, and a site-head operating model to ensure timely delivery

- Gearing levels: Company comfortable with current gearing (0.71x), expects strong operating cash flows to support growth

- Project delays (e.g. Ashok Vihar): Management acknowledged delays but emphasized enhanced returns due to price appreciation; confident of launch by Q4

Competitive Landscape:

Godrej Properties has emerged as a leader among listed developers, achieving the highest quarterly booking value for two consecutive quarters. The company’s brand strength, execution track record, and financial capabilities are allowing it to gain market share in a consolidating industry.

Guidance and Outlook:

- FY2025 booking value guidance of INR 27,000 crores

- Collections guidance of INR 15,000 crores for FY2025

- Embedded margins slightly higher than FY2024 levels

- Expect strong business development momentum in Q2 FY2025

Capital Allocation Strategy:

- Maintain gearing in the range of 0.5x to 1x

- Focus on high-quality land acquisitions in top 4 markets (Mumbai, NCR, Bangalore, Pune)

- Open to larger land parcels if returns are attractive

- Potential for equity raise if valuation is favorable and growth opportunities exceed internal accruals

Opportunities & Risks:

Opportunities:

- Market share gains in consolidating industry

- Expansion into new micro-markets within existing cities

- Potential for margin expansion through price increases

Risks:

- Cyclical downturn in real estate market

- Execution challenges in rapidly scaling business

- Regulatory hurdles and approval delays

Regulatory Environment:

The company faces some regulatory challenges, such as the ongoing approvals for the Ashok Vihar project and recent issues with the Chandigarh commercial project. Management is confident of resolving these issues but acknowledges the potential for delays.

Customer Sentiment:

Strong customer response to new launches, with projects like Godrej Woodscapes (Bengaluru) and Godrej Jardinia (Noida) achieving record sales. High collection efficiency (94%) indicates positive customer sentiment and financial ability to honor commitments.

Top 3 Takeaways:

- Record-breaking sales performance with INR 8,637 crores booking value in Q1 FY2025, positioning Godrej Properties as a leader among listed developers.

- Strong execution capabilities and strategic focus on premium locations driving growth and profitability.

- Robust business development pipeline to sustain growth momentum, with potential for market share gains in a consolidating industry.

India Pesticides Ltd (05-08-2024)

Brief Summary from IPL Q1’Concall

- Growth in Q1’FY25 is largely driven by volume growth and not the price increase

- During Q1’FY25, formulation growth have been significant while technical growth have been steady

- During this quarter, commissioned the intermediate plant for backward integration for one of herbicide

- Revenue growth of 15-20% expected for FY’25

- Expecting the EBITA margins to reach between 18-20% from Q3’FY25 onwards

- Demand picking up in international markets

- 18-19% revenue from new molecules

- July’24 have been great in terms of business

- From Hamirpur plan, don’t expect revenue during current FY. From FY’26, significant contribution expected from this plant

- 110 Cr. capex required during current year will be funded from internal accruals

- Q1’25 capacity utilization Formulation plant-100%; Technical plan – 66%; The formulation plant capacity will increase in next 1-2 month

- For FY’26, the guidance for revenue growth about 15-20%

- Cash in hands about 140 Cr.

Disc – Invested

Maharashtra seamless-a value plus cyclical play (05-08-2024)

My key take aways from the management conf call:

-

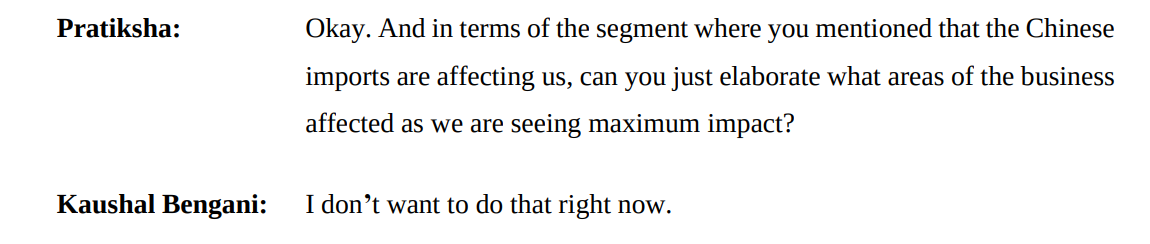

Quarter numbers are lower because of:

a. account of increased competition,

b. lower raw material prices, and

c. some dumping from Chinese manufacturers in certain segments. <did not elaborate which segment specifically it is impacting. This anyways is a time-consuming process, and no quick turnaround is possible. Roughly above 3 were equally weighted impact wise per management.>

d. Preventative maintenance shut down, led to not executing on some high value orders.

Lower RM cost, led to inventory devaluation, which will be nullified once we fulfill the orders that were supposed to be dispatched in the Qtr gone by. -

Telangana Unit:

a. The Telangana finishing line was expected to be completed by March 2025. But, I don’t think that will happen, in all probability it will be deferred by at least 9 months, because we have recently placed order for some equipment, those orders have been finalized, purchase order has been issued. However, the gestation period for that order is 12 months. So, reasonably speaking, the Telangana unit expansion should get completed by December 2025. -

Hot mill upgrade will only happen once the Telangana finishing line is in place because we will have a loss of production whenever we take the hot mill upgrade. So, in order to compensate that loss, we need the Telangana unit to be active in full capacity. The sense which I am getting from your question is, when will volume growth come in? So, I don’t think there will be any volume growth in FY25. And in FY26, volume growth will only happen once the Telangana finishing line has been completed and is open for commercial production.

-

We don’t export to the Middle East, exports have not revived, exports have been slow for more than a year. Market size in US and Canada is very big, but they have not revived for us.

-

EBITDA per tonne fell from Rs.22,000 a tonne to Rs.9,000 per tonne!!

-

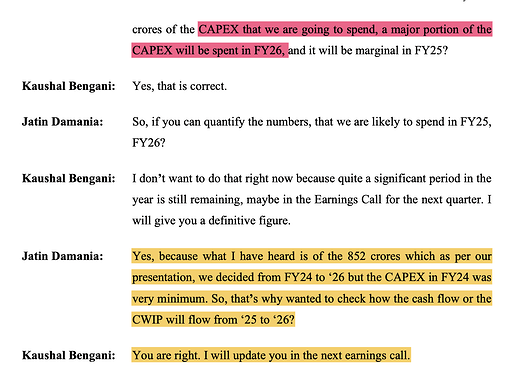

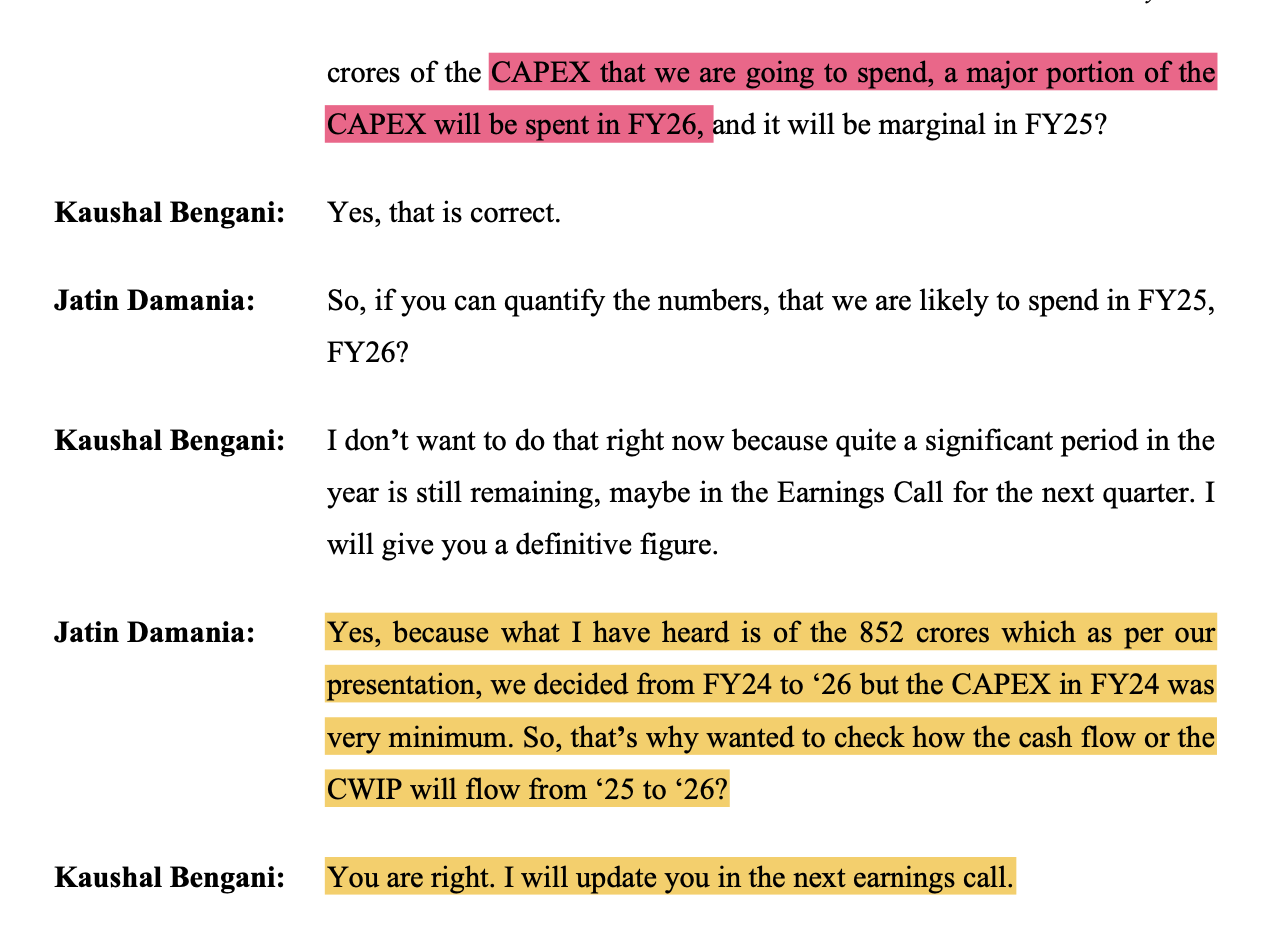

Capex:

The announced ~850 cr would be mostly spent only in FY26.

Although there might be a quick reversal once the high values get shipped and the RM prices adjusted and might show profit and bump in margins, the Capex has been delayed to FY26. So, its wait and watch for me in this counter.

Disc: Not invested.

Tinna rubber – recycling a rubbery growth path (05-08-2024)

Pointers from Tinna Rubber & Infra’s Q1 FY25 concall (Aug 5, 2024)

EPR credits:

-

EPR credits for all of FY24 have been booked in Q1 FY25. They amount to INR 10.53 crs. This aligns with what the company had stated in Q4 FY24, that the EPR credits for FY24 are still to be received by the company

-

Actual revenue of INR 2.5 crores received by the company against booked revenue of INR 10.53 crores. The remaining INR 8 crores have been booked basis the EPR credits available on CPCB portal and has been calculated at Rs. 2000 per unit. This as per the management is a conservative per unit cost as they’ve realized the sale at higher values

-

Going forward the management will add EPR credits to the quarterly revenues as and when they are added to the CPCB portal

-

The output (end usage) of the recycled tyres determines how many EPR credits are realized. It is not calculated based on the tons of end of life tyres crushed

-

Only the surplus of what EPRs they can sell is reported by them as being net importer of waste tyres they need to use some credits to offset the waste tyres being imported for crushing

-

The regulation around EPR policy is fluid as it is still being worked on by the government. There can be further changes to the policy depending on how the regulations shape up

-

As per the management, 500 crores of EPR credits will be needed by tyre companies to offset their requirements (as per the management these are the unofficial hearsay numbers and they should not be quoted on the same as they are only trying to guesstimate the demand for EPR credits)

Growth, margins, capex and other points:

-

Revenue guidance: The below numbers match what the management had indicated during the last con call

- FY25: 500 crs. Management is very confident of achieving the same.

- FY26: 700 crs

- FY27: 900 crs

-

The capex being undertaken is from the view of achieving the guidance provided above. The management had suggested capex of INR 35-40 crs for FY25 on the last call. This is now stated as INR 50 crs for FY25. However, to be fair it remains in the ballpark of what was quoted

-

They may take INR 20 crores of term loans in FY25 to meet current expansion plans. They had indicated in the last con call as well that they are not averse to taking debt if it helps them grow in a responsible way

-

EBITA margins are ~16.5% on a consolidated basis. Expect to maintain a similar profile unless some major unforeseen costs come up (for e.g. increase in freight rates due to the Red Sea issue etc.). The margin profile for their business abroad will be similar to what they make in India (if not better). For e.g. the EBITDA margin in their Oman business is better than their India business

-

Aiming to become a global recycling tyre company. Hence they are pursuing opportunities outside India, like the ones in Saudi Arabia and South Africa

-

The new upcoming plant in Saudi Arabia will cater to all product lines

-

Focus till FY27 will remain towards tyre recycling itself. Not looking to enter into any other recycling categories

-

They are looking at the PPE business where recycled rubber and recycled plastics can be combined for use in various products like – pipes, shoes, plastic pellets etc.

-

India generates around 2 mn tons of end of life tyres per year

-

Varle plant will generate to 80 – 100 crs per year. Expecting ~70% capacity utilization from Q3 FY24. Numbers quoted are in the same ballpark as the last call

A couple of open questions regarding EPR post the Q4 FY24 and Q1 FY25 call,

-

EPR sales in Q4 FY24 was INR 6.6 crores and that was for EPR credits booked in FY23. However, in the Q4 FY24 call they had mentioned that it was not entirely sold. Now EPR value for FY24 is INR 10.53 crores and EPR credits worth ~INR 2.5 crores have been booked in Q1 FY25. So what happened to the EPR credits from FY23 that were not sold? Is it added to FY24?

-

Do the unsold EPR credits of ~INR 8 crores also reflect as receivables on the balance sheet as revenues have been booked but the actual amount has still not been realised?

Disc: Invested as a tactical 3-year bet. #1 stock in my stock pf. Will continue to hold as the management is walking the talk.

Maharashtra seamless-a value plus cyclical play (05-08-2024)

Reasons for decline in numbers as per Management

-

The first reason is the fall in sales realization, which has been on account of increased competition, lower raw material prices, and some dumping from Chinese manufacturers in certain segments.

We are in discussion with relevant authorities to address the issue of Chinese dumping, but that is a long-drawn process. -

Due to the preventive maintenance shutdown of the mill manufacturing high value orders thereby impacting the earnings profile for the quarter. This mill has since resumed production at the start of Q2

FY25 and normalization of dispatches is expected in the second quarter. -

The third reason was the dispatch of high value orders which were in limited quantity. As fewer high value orders were dispatched in Q1, the entire high value inventory which was purchased against

the remaining high value orders had to be marked down when raw material prices fell during the quarter.

Wasn’t there an anti-dumping duty in place till 2026, are Chinese imports still competitive despite that?

Sharda Motors – Emission tailwinds or EV threat to exhaust systems? (05-08-2024)

Can anyone provide insights into the total addressable market for exhaust systems and suspension systems in the Indian automotive sector, specifically distinguishing between passenger vehicles and commercial vehicles? Additionally, if anyone can share a view of how the market evolving over the next few years in terms of growth potential and key driving factors?