Not. it’s financial year 2022-23.

Posts tagged Value Pickr

Journey and Portfolio of a goal-based NEEV investor (02-08-2024)

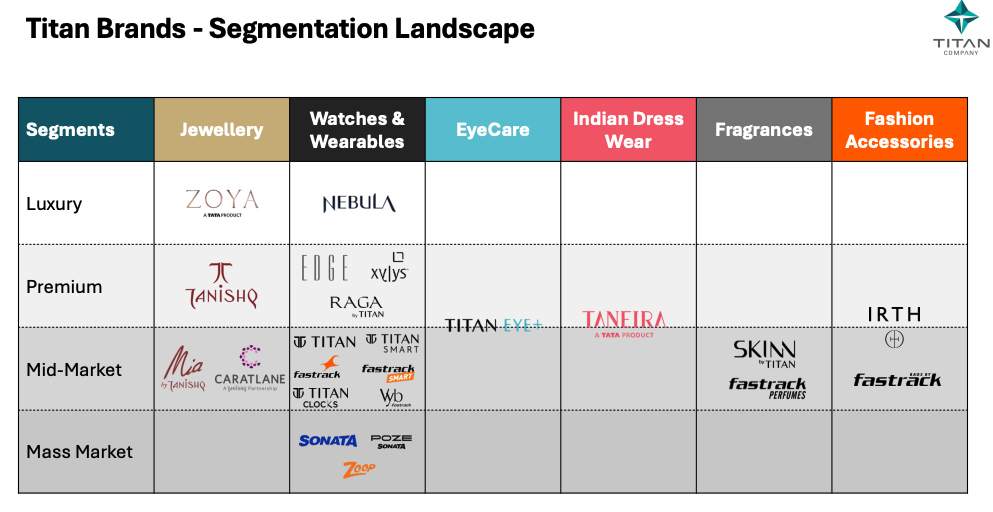

Titan published this data in their recent Q1 FY25 presentation:

Now I tried comparing Titan (a house of brands) with LVMH. Results are interesting:

| Category | Segment | Titan Brands | LVMH Brands |

|---|---|---|---|

| Jewellery | Luxury | Zoya | Bulgari, Chaumet |

| Premium | Tanishq | Fred | |

| Mid-Market | Mia by Tanishq, CaratLane | ||

| Watches & Wearables | Luxury | Nebula | TAG Heuer, Hublot, Zenith |

| Premium | Edge by Titan, Xylys | Dior Watches, Louis Vuitton Watches | |

| Mid-Market | Titan, Raga by Titan, Fastrack | ||

| Mass Market | Sonata | ||

| Eyecare | Premium | Titan Eye+ | |

| Mid-Market | Titan Eye+ | ||

| Indian Dress Wear | Premium | Taneira | |

| Fragrances | Luxury | Dior, Guerlain | |

| Premium | Givenchy, Kenzo, Benefit Cosmetics | ||

| Mid-Market | SKINN, Fastrack Perfumes | ||

| Fashion Accessories | Luxury | Louis Vuitton, Dior, Celine, Loewe, Givenchy | |

| Premium | IRTH | Kenzo, Fendi | |

| Mid-Market | Fastrack | ||

| Wines & Spirits | Luxury | Dom Pérignon, Moët & Chandon, Veuve Clicquot | |

| Premium | Hennessy, Glenmorangie | ||

| Selective Retailing | Luxury | Sephora, Le Bon Marché |

Tl;dr my thesis in investing in Titan is not just a jewellery brand (although 80% of business comes from Jewellery today).

But its final destination is Indian LVMH – started from India, and expanded globally.

IRB INVIT TRUST- new game in the town! (02-08-2024)

Q1’25 results are here.

Came on 26th, post market. At first glance, the fine print in maint provisions seems to be putting the comparison, not like to like.

DPU is the same 2 but the breakup is a tad different.

The next trigger has to be addition of a project and that somehow seems to be elusive. The wait continues.

I also thought that the DPU must inch up a tad, based on concall but that did not happen either and there lies the key difference between IRB and Indigrid

Glenmark Life Sciences (02-08-2024)

Is this speculation from your side, or you have factual information ?

Edelweiss Financial Services (02-08-2024)

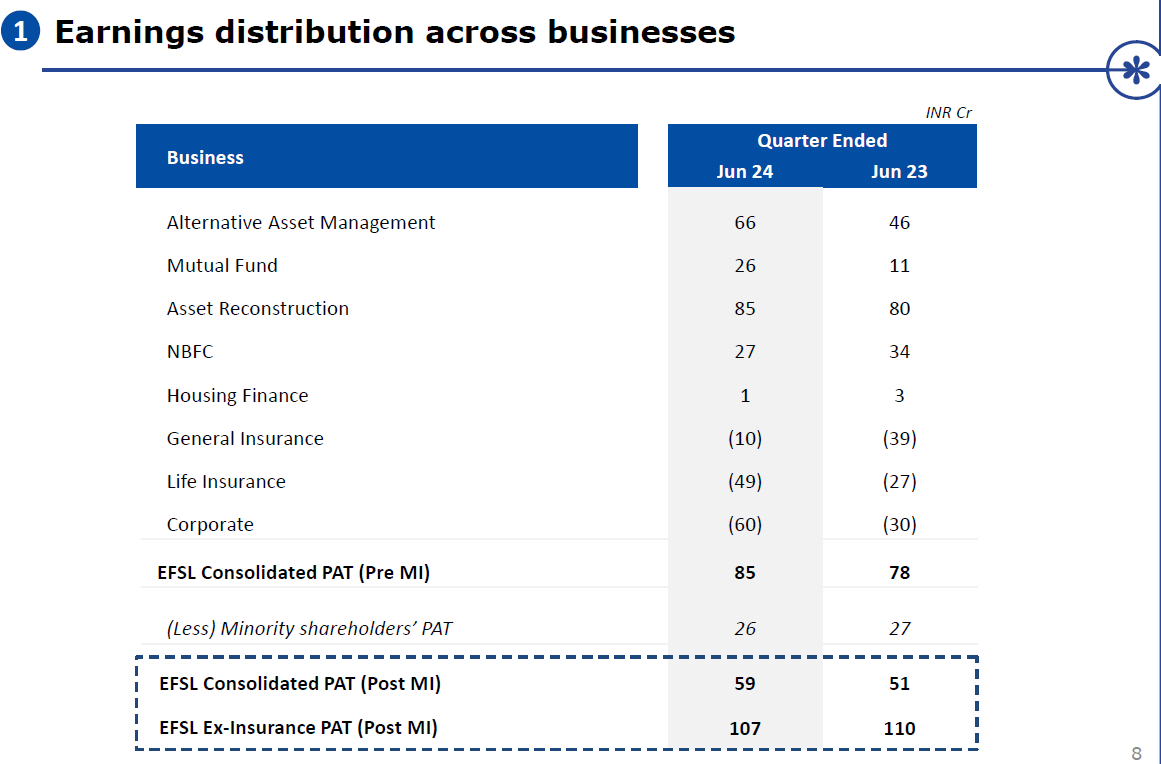

Edel declared Q1 result today.

My 2 cents:

At the current rate, AIF annualised PAT is around 250 cr. However, as the rate is accelerating, it could be 28-300 cr PAT just for AIF.

The mutual fund business is also taking off, with the best PAT ever of 26cr. Their SIP portfolio is growing at a good rate, and they are getting more equity MF. This could be 80/100 PAT for Fy25.

They are setting off AIA spin-off again. I think they should distribute the shareholders the same way they did for Nuvam instead of IPO. In the case of IPO), Edelweiss may get money, but as a shareholder, I want money to be in my hand and not in the hands of management (as they have made a lot of capital misallocation in the past). The Nuvama spin-off was rewarding. I hope AIF/MF follows in line.

AIA profit (AIF +_MF) at annualised rate is 300+ in Fy25. Assuming 20/25 PE, that business is worth around (6,000 to 7,500 cr) at today’s price, which is Edelweiss’s market cap at CMP.

Wholesale reduction of 200cr is on target, less than planned thought. I think this is a sticking point. If wholesale is to be removed from their business, Edelweiss will be quoted at multiple times the current price. But it is not likely to happen. Most of the pending Wholesale must be hard to get rid of , so time is the medicine here. They want to reduce to 1250 cr in June 2026, which is eight quarters away. From 3900 to 1250 (reduction of 2650 cr) in 8 quarters equates to a reduction of 325cr per quarter. They are nowhere near that rate in the last 6 months, so current projects look optimistic at the moment.

General insurance losses are reducing further. Hopefully they keep the momentum. Life insurance is not showing sign if getting better. Hopefully from Fy26 onwards their looses reduce (long if).

Nuvama has declared a dividend of Rs 81 per share, for a total of 289 cr. Edel owns around 14%, which means they will be getting 40cr of dividends in Q2, which will be handy. Additionally, this dividend will be a regular affair going forward.

Note: Long term invested

SJS Enterprises Ltd (02-08-2024)

Onboarded Dixon this quarter. According to the management, this opens large opportunites for expanding into consumer durable segment. Steller quarterly performance. Great growth. Acquisitions on track. Hope it continues.

Disc. Holding. Biased. No recommendation to buy/sell

Glenmark Life Sciences (02-08-2024)

I believe any closure notice revocation can happen after min. 25-30 days. It might take more time than that. Ankleshwar, Being a majority production site , production loss would be substantial. If not more they will lose atleast 25-30% reduction in production in this quarter.

More serious issue in my opinion, is the reason of closure. It seems company mistakenly or intentionally let out effluent in storm water drainage, which showed in the COD parameter. Being not so serious about local authority compliances when your foreign inspection like FDA are overdue is matter of concern. And one very big risk to look out for.

Evaluating to sell/reduce allocation here.

Thanks,

EFC – Entrepreneurial Facilitation Centre (02-08-2024)

Thanks got the clarification. A follow up on the contract tenure. Got this input from the concall transcripts. What are your views on Asset Liability Mismatch. Thanks again

EFC

a) Average client contract tenure: 2-3 years (Managed space)

b) Average landlord contract tenure: 5 to 8 years (Straight lease)

Awfis

a) Average client contract tenure: 33 months

b) Average landlord contract tenure: 5 to 10 years

RBL BANK – Is it a Good Long Term Story? (02-08-2024)

I have been looking at various banks in terms of valuation, growth guidance and asset quality. RBL seems to tick a lot of boxes yet the prices are not being appreciated. It trades at around 1 P/B value while some of the SFBs trade at >2P/B value. Any thoughts?

Edelweiss Financial Services (02-08-2024)

Given market buoyancy and positive feedback received, EAAA may also explore IPO/listing – more update in next quarter ![]()