It may be to monetize the demand for Indian music from NRI’s and others in the international market.

Posts tagged Value Pickr

RSWM LTD (Ascending triangle + Multiyear break out ) (26-11-2024)

anyone tracking stock has reached support level

Infollion Research Services Ltd – Moated Microcap with Differentiated business? (26-11-2024)

It would be bad news if they are considering a QIP

Disc: tracking

Balaji Amines Opportunity (26-11-2024)

Thanks for sharing your views. Went through their conversation again and did some research. There are a couple of reasons, which, I think could be the reason for his anger.

-

Question on Balaji Specialty Chemicals: Balaji specialty chemicals is not a wholly owned subsidiary of Balaji Amines. Balaji amines holds 55% stake and rest is owned by Promoters. The investor criticised the 750Cr investment in Specialty Chemicals saying it generates EBIDTA of 3Cr only. This could have felt like a personal attack on the management.

-

Question on expected margins: Many investors were asking expected revenue and margins on DME and ACN plants. Management kept on saying its too early to say anything. When the investor in question again asked the same question it might have triggered the management a bit more.

Frontier Springs – has departed, whats the next destination? (26-11-2024)

Management guidance is of 240-250cr gross revenue including GST. Net revenue would be lower approx 220-225cr. H2 would be in range of 120-125cr

HDFC Life Insurance Company (26-11-2024)

is there a possibility of HDFC merging health and life under a completely new entity to make it a bigger and wholesome player ?

Jaybee laminations ltd – transforming your portfolio (26-11-2024)

A couple of reports/information sources:

Notes from Nomura report:

-

India’s power transmission sector is poised for significant growth, driven by surging electricity demand and ambitious renewable energy capacity addition targets. CEA expects USD110bn in investments over FY22-32E.

-

In a scenario where countries meet their energy and climate targets, wind and solar power will account for a substantial portion of the increase in global power capacity. Modern, digital grids are crucial for ensuring electricity security throughout this transition. As variable renewables like solar and wind become more prevalent, power systems must be more flexible to accommodate fluctuations in output.

-

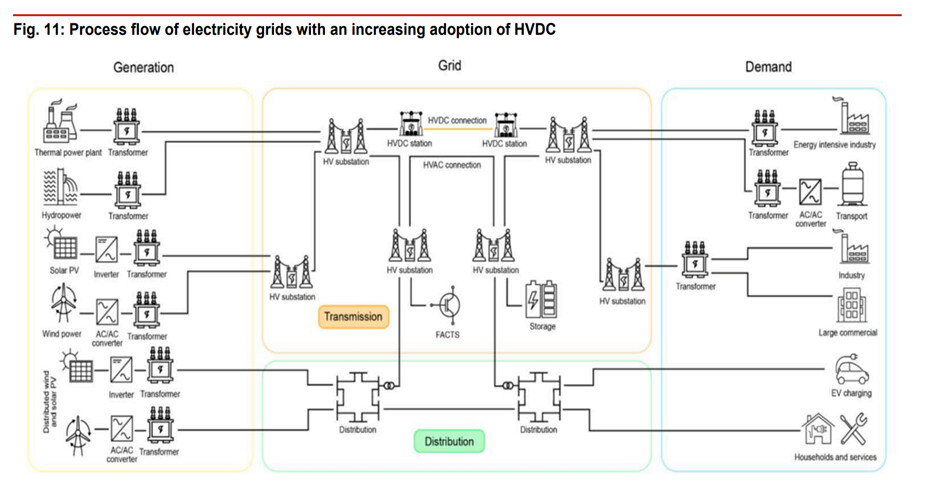

Modern and digital grids are crucial for ensuring reliable electricity supply during the transition to clean energy. As the prevalence of variable renewables like solar and wind increases, power systems must become more adaptable to handle fluctuations in output. We think demand for system flexibility is likely to double between 2022 and 2030F, necessitating innovative operational strategies and integration of distributed resources, such as rooftop solar and diverse flexibility options. Achieving this flexibility requires the implementation of grid-enhancing technologies and the optimization of demand response and energy storage through digitalization. These measures are essential for maintaining electricity security and supporting a successful transition to a cleaner energy future, in our view.

-

A significant challenge in the transition to net-zero emissions is the grid infrastructure. While investment in renewable energy has grown substantially, investment in grid infrastructure has remained relatively stagnant, in our view. Our analysis reveals that slower grid development could lead to reduced renewable energy adoption and increased reliance on fossil fuels. Additionally, inadequate grid development increases the risk of costly power outages and heightens reliance on gas and coal imports.

-

We estimate India’s power demand will record a healthy CAGR of more than 7% over FY24- 27F driven by growing economic activity.

-

Renewables continue to scale up strongly as the share of renewables in India’s energy mix continues to grow, with solar and wind power meeting ~75% of the incremental demand by FY25F, as per our estimates. Renewable energy (RE) accounted for 33.5% of India’s electricity supply in FY24 (as per CEA), which we estimate will rise to 35% in FY25F, driven by a 23% y-y increase in solar power

-

According to the Ministry of Power’s estimates, on the capacity side, India’s installed power capacity is expected to rise at a 10% CAGR over FY24-FY30E to 777.1GW from 450.8GW currently

-

Renewables (ex-hydro) will account 55% of the total capacity and hydro will account for ~7%. Solar capacity is anticipated to record a 22% CAGR to 293GW in FY30E from 89GW at end-FY24 and wind is anticipated to increase at a 13% CAGR to 100GW in FY30E from 47GW currently. The government has set an ambitious target of 500GW of RE capacity by 2030, including 300GW from solar, as part of its commitment to achieving net-zero emissions by 2070. Currently, India’s installed power capacity is 448GW and we expect it to grow to 777GW by FY30F, with 279GW coming from renewables. The country is the third-largest power producer globally, and aims to meet 50% of its electricity needs from renewables by 2030, supported by policies such as the PM Surya Ghar for residential rooftop solar installations, PLI for PV module manufacturing and PM-KUSUM program for solar pumps among others. By 2040F, we believe RE will generate 49% of India’s electricity, driven by advancements in battery efficiency and cost reductions in solar energy. In FY24, India consumed 1,543TWh of electricity, with peak demand hitting a record 243GW, driven by industrial growth and extreme heat waves (as per CEA).

-

India’s data center industry is experiencing unprecedented growth, driven by rapid digitalization, the rise of AI, IoT, and a growing internet user base — currently at 946mn. With a current installed capacity of 960MW, we expect data center capacity to reach 7.5GW in our base case and 9GW in our bull case by FY30F, fueled by the adoption of 5G, AI, and IoT. The surge in digital activities like e-commerce, online education, OTTs generate significant data, requiring robust infrastructure for storage and processing, while AI growth will further drive robust power generation. Government initiatives, such as Digital India, further support data center expansion. Currently, data centers consume 8.4TWh of electricity, representing 0.5% of India’s total power consumption, but we estimate this will rise to 66TWh, accounting for 3% of India’s total electricity demand by FY30F in our base case and 80TWh in our bull case.

-

Increased government focus on transmission: The government’s emphasis on improving transmission infrastructure has intensified, driven by the need for adequate generation capacity and the resolution of fuel supply challenges. Currently, India’s transformation capacity (220kV and above) is at 2.83MVA/MW, compared to the optimal requirement of approximately 7MVA/MW for seamless power evacuation. This underscores the necessity for greater investments in the transmission sector.

-

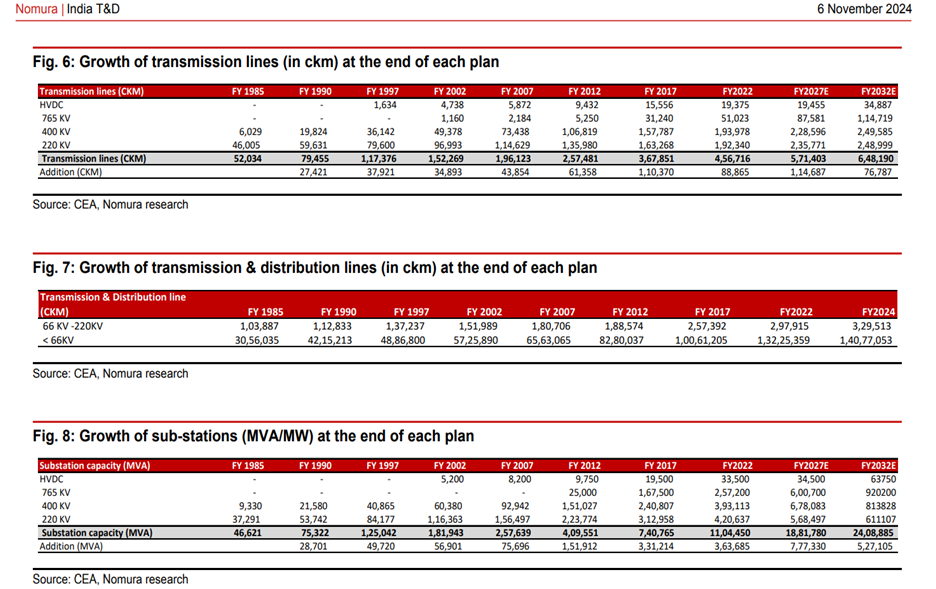

India’s power grid offers multi-year growth opportunities: The National Electricity Plan 2023-32 for Central and State Transmission Systems has been finalised with an investment outlay of INR9.15tn. Under the previous plan of 2017-22, about 17,700ckm (circuit kilometers) of lines and 73GVA of transformation capacity were added annually; 88,865ckm of transmission lines and 349,685MVA of transformation capacity have been added. Under the new plan, transmission network in the country will be expanded from 485,544ckm in 2024 to 648,190ckm in 2032. During the same period, the transformation capacity will increase from 1,251GVA to 2,345GVA. Nine High Voltage Direct Current (HVDC) lines of 33.25GW capacity will be added in addition to 33.5GW presently operating. The interregional transfer capacity will increase from 119GW to 168GW. This plan covers the network of 220kV and above. The estimated costs of the Inter State Transmission System (ISTS) and the intra-state transmission system are INR6.61tn and INR2.55tn respectively (as per CEA).

-

The Minister of Power recently unveiled the National Electricity Plan (NEP) 2023-32, a comprehensive blueprint for the expansion and strengthening of the central and state transmission systems. The NEP allocates a substantial investment of USD110bn (INR9.15tn) to address the escalating demand for electricity, driven by factors such as the rapid integration of RE sources, the development of green hydrogen and pumped storage projects, and the rising peak demand.

-

We expect the NEP to stimulate a significant increase in transmission capex, bolstering the grid’s capacity to accommodate the growing demand for electricity. However, challenges in grid connectivity for new renewable projects in certain regions have been observed, potentially impacting the overall project timeline

-

Between FY24 and FY32, the system-wide transformation capacity should expand by a substantial 1,158GW (an 8.53% compound annual growth rate), and the transmission network will grow by approximately 3.7% (from 485,544ckm to 648,190ckm).

-

As per CEA, an estimated expenditure of INR9.15tn would be required for implementation of additional transmission system of 220kV and above voltage level in the country (transmission lines, substations, and reactive compensation, etc.) during 2022-32.

-

The implementation timeline for these projects is contingent upon the development of associated generation projects. While a 5–8-year timeframe is anticipated, it is subject to adjustments based on evolving energy sector dynamics. Transmission plans will be regularly reviewed and refined to align with the specific schedules of generation projects.

-

Reduced competitive intensity following domestic manufacturing clause implementation: To support the government’s ‘Make in India’ initiative, PGCIL has implemented strict regulations requiring equipment suppliers to establish manufacturing facilities in India. Even prior to this current push, PGCIL had introduced a domestic manufacturing clause for its 765kV transformers, prompting companies such as TBEA Shenyang to set up factories in Baroda. PGCIL has expanded the domestic manufacturing requirement across various equipment types, which may encourage more Chinese and Korean companies to establish operations in India.

-

Benefits of the ‘Make in India’ clause for local players: The ‘Make in India’ clause provides two key advantages for local manufacturers: Elimination of non-serious competitors: It effectively removes non-serious players who were previously importing and dumping equipment from their overseas factories. This change increases market opportunities for established local players, as seen in the 765kV transformer market, where Korean companies have exited after PGCIL enforced the domestic manufacturing requirement. Enhanced pricing for local equipment: By creating a more level playing field against foreign competition (particularly from Chinese and Korean firms), the clause helps improve pricing for domestically produced equipment, benefiting local manufacturers.

-

765kV transformers: Reduced competition due to domestic manufacturing clause: To encourage domestic production of 765kV transformers, PGCIL implemented a requirement that vendors supply transformers from their Indian manufacturing facilities. This move was necessary because transformers have a lifespan of 30-35 years, and there had been a significant increase in imports from Korea and China. According to our analysis based on data from PGCIL, Korean manufacturers held a 22% market share in 765kV transformers, while Chinese firms commanded 44% in FY10. By FY12, the market share of Korean manufacturers plummeted to 2%, leading to their complete exit, as they were unwilling to establish a transformer plant in India. Similarly, Chinese manufacturers Baoding and Xian have also left the market due to their inability to meet qualification standards. As a result, only 4-5 companies are now competing in PGCIL’s 765kV transformer bids: GE T&D, TBEA Shenyang, Hitachi Energy India, Siemens India, and CG Power. With no new entrants expected to set up factories in India, competition will likely remain limited to these established players.

-

Importance of power transformers: Power transformers are essential for the effective functioning of power systems. Approximately half of the weight of a transformer consists of steel, with over 60% being cold rolled grain-oriented electrical steel (CRGO), known for its unique magnetic properties and high permeability. The remaining portion is construction steel. CRGO is crucial not only for transformers but also for power generators and electric vehicle (EV) charging stations. The transformer sector currently represents the largest share of demand for CRGO. Different quality levels of CRGO are available, with higher permeability varieties allowing for smaller transformer designs, reduced insulation oil requirements, and lower electrical losses. Regulatory measures, such as the Energy Efficiency Program in the US and the Ecodesign Directive in the EU, are driving the adoption of higher-quality CRGO. However, European manufacturers have recently raised concerns about potential shortages of this critical material.

-

A significant risk is the potential delay in power transmission and distribution (T&D) spending or prolonged decision-making processes by key government, which can directly impact project inflows and revenue stability. As T&D projects are capital intensive and often depend on government and utility investment cycles, any slowdown or deferment in spending could lead to a backlog of unexecuted orders, straining operational resources and delaying revenue realization.

Jaybee laminations ltd – transforming your portfolio (26-11-2024)

[Short description of investment thesis:

Jaybee Laminations ltd (JBLL) manufactures transformer cores which go into transformers which in turn go into power transmission network. With long term growth tailwind in power transmission network and subsequently in transformers, JBLL is a great long term opportunity to ride this tailwind.]

• ABOUT THE COMPANY:

Jay Bee lamination is a manufacturer of CRGO Silicon Steel Cores for the Power & Distribution Transformer Industry of India. JBLL has over four decades of track record in the CRGO Silicon steel cores business.

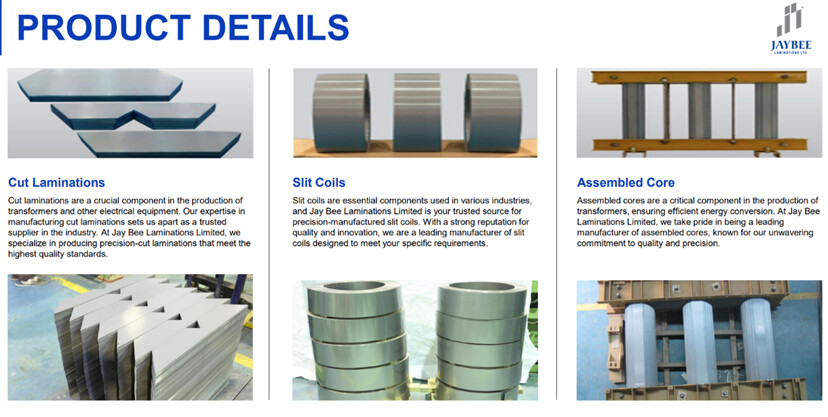

PRODUCTS:

Products manufactured includes Cut Laminations, Slit Coils & Assembled Cores having end use in transformer industry

The lamination industry serves as a critical proxy for the transformers market due to its indispensable role in ensuring the efficiency and performance of transformers. Electrical laminations, particularly CRGO and CRNGO steel laminations, are essential components that minimize core losses and enhance magnetic efficiency

MANUCTURING UNITS:

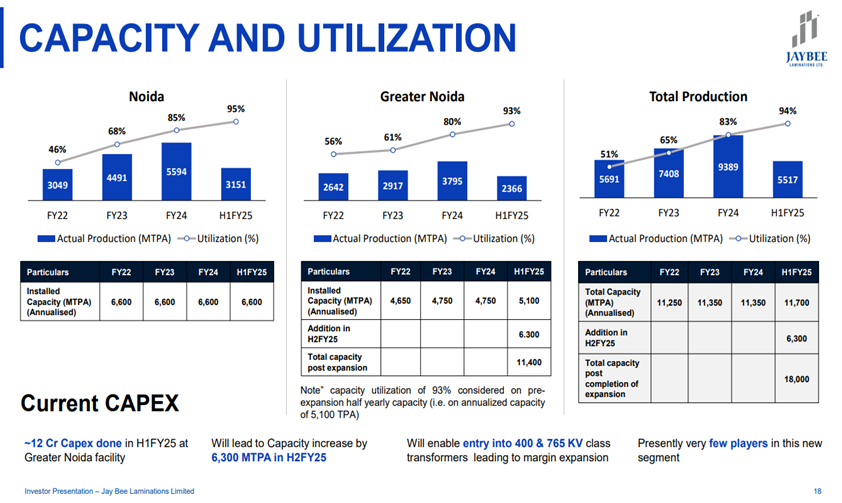

o Currently having manufacturing units located in Noida & Greater Noida in Uttar Pradesh. Current installed capacity of ~11,700 MTPA with Additional capacity of ~6,300 MTPA being added at the existing Greater Noida Plant by H2FY25

Currently operating at 95% capacity (H1FY25)

o Having in-house laboratory for raw material and finished goods sample testing and in-house tooling division for blade sharpening

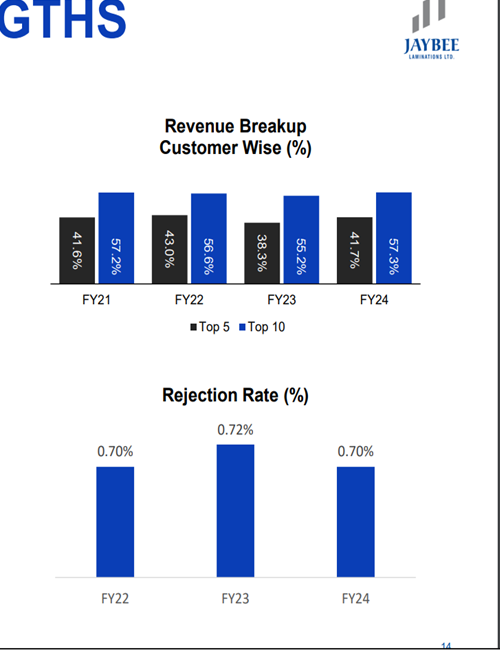

CUSTOMERS:

END INDUSTRY:

Sector Wise Revenue Break-up (%) – FY24 = Transformers – 97.92%

The biggest buyer of transformers in the Indian market is the government. But we are also seeing an increase of transformers demand from the private sector, especially with solar and wind energy is concerned. Because for new generation types, there will be requirement of new transmission and distribution infrastructure that will require new transformers.

Company currently sells transformer to power generation customers and power distribution customers.

(Power transformer players definitely fetch a better margin, because ticket size of each transformer is very high compared to distribution transformers. A standard distribution transformer would be in the price range of ₹50,000 to ₹5 lakhs. While the power transformers can go in crores, they can be as high as ₹5 crores to ₹25 crores per transformer. So, the end customer becomes very, very stringent on the quality standards of the power transformers. Because if a power transformer fails, it blocks the entire grid. The grid goes for a toss, and the lead time to produce another transformer or repairing that transformer is very big. The transportation is very difficult, because each transformer weighs about, it can weigh about 50 tons to 300 tons. So, all those factors considered, the quality standards go up significantly in power transformers. And the entire value chain, the entire supply chain has to be like that. So, the end customer, who does inspection at our premises also for the raw material as well as the final product that we make for the transformer tower)

**INVESTMENT THESIS**

• HIGH END USER INDUSTRY GROWTH:

(JBLL supplies CRGO cores for transformers → transformers are used in transmission of power → Increased Transmission of power depends upon increased power generation and demand)

We estimate India’s power demand will record a healthy CAGR of more than 7% over FY24- 27 driven by growing economic activity.

According to the Ministry of Power’s estimates, on the capacity side, India’s installed power capacity is expected to rise at a 10% CAGR over FY24-FY30E to 777.1GW from 450.8GW currently

India’s power transmission sector is poised for significant growth, driven by surging electricity demand and ambitious renewable energy capacity addition targets. CEA expects USD110bn in investments over FY22-32E.

NATIONAL ELECTRICITY PLAN 2023-32:

The National Electricity Plan 2023-32 for Central and State Transmission Systems has been finalised with an investment outlay of INR9.15tn. Under the new plan, transmission network in the country will be expanded from 485,544ckm in 2024 to 648,190ckm in 2032. During the same period, the transformation capacity will increase from 1,251GVA to 2,345GVA. Nine High Voltage Direct Current (HVDC) lines of 33.25GW capacity will be added in addition to 33.5GW presently operating. The interregional transfer capacity will increase from 119GW to 168GW. This plan covers the network of 220kV and above. The estimated costs of the Inter State Transmission System (ISTS) and the intra-state transmission system are INR6.61tn and INR2.55tn respectively (as per CEA).

Between FY24 and FY32, the system-wide transformation capacity should expand by a substantial 1,158GW (an 8.53% compound annual growth rate), and the transmission network will grow by approximately 3.7% (from 485,544ckm to 648,190ckm).

As per CEA, an estimated expenditure of INR9.15tn would be required for implementation of additional transmission system of 220kV and above voltage level in the country (transmission lines, substations, and reactive compensation, etc.) during 2022-32.

The NEP will stimulate a significant increase in transmission capex, bolstering the grid’s capacity to accommodate the growing demand for electricity. However, challenges in grid connectivity for new renewable projects in certain regions have been observed, potentially impacting the overall project timeline

India Power and Distribution Transformer Market: The market size was valued at around USD 3.97 billion in 2023 and is projected to reach around USD 8.41 billion by 2030. The market is estimated to grow at a CAGR of around 10.84% during the forecast period, i.e., 2024-30.

All transformer companies have robust orderbooks and bidding pipelines. Also, huge re-rating has happened in transformer companies. It might lead to re-rating in JBLL shares

So, there’s no demand concerns for atleast next 6 years. The strong prevailing demand is also confirmed by the fact that JBLL was operating at full capacity and is expected to fully utilized newer capacities

• CAPACITY EXPANSION:

o Capacity Expansion completed at Greater Noida in October, 2024. Capacity increased from 11,700 MTPA to 18000 MTPA with Additional capacity of 6,300 MTPA.

Incremental revenue potential of the newer capacities is about ₹180 crores ((FY24 sales – 303cr)

o New Greenfield facility: Entered into a lease agreement for a property located at Noida, Gautam Buddha Nagar, admeasuring ~3,662.97 sq. mtrs. • This will be used to establish a new manufacturing facility to support future expansion, growth, and new projects • This expansion is necessitated as our existing manufacturing units are expected to reach close to full capacity utilization in FY26 • The new manufacturing facility at Unit-III is projected to commence commercial operations in H2FY2026

o All three units put together, theoretically, we can go up to about 25,000 to 30,000 tons. (From currently 11,700 tons in H1FY25). On full utilizations, the turnover can be around ₹900 crores. (FY24 sales – 303cr)

• ENTRY INTO VALUE ADDED PRODUCTS:

o Targeting new market segments • Aiming to tap new market segments of Power transformers including for 400 kV and 765 kV class. • Given the scarcity of consistent suppliers in these higher voltage class of transformers, this strategic expansion presents a substantial opportunity to escalate production volume.

Currently caters to transformers upto 220 KV with a plan to tap new market segment of Power transformers including for 400 kV and 765 kV class by H2FY25. (The Greater Noida plant we have a new facility, where a new shed which has all the facilities required to process 400 kV and 765 kV class orders)

The demand is increasing in 400 kV and 765 kV class. d the second reason is the capacity utilisation is also very high, and outputs are much better. So it made sense for us to expand in those segments. So we are continuing to expand in those segments, and we will soon target those customers.

o Better margins: 400 kV class and 765 kV class would fetch better gross margins of about 2% to 5%.

o Increase Share of Value-Added Products: With the enhanced capacity, higher value-added products would be added in the product portfolio increasing their share in overall revenue. Revenue mix in total revenues of value-added products over next 2-3 years will be on an average 25% in terms of capacity.

o Power Grid approval upto 220KVA. Approval for 400KV class transformer at Greater Noida in process (“We are in the process of applying to PGCIL for 400 kV class approval. Once we get, 400 kV class approval, we will be able to target those end customers. And once we prove our ability in 400 kV class, then the natural step will be to get approval in 765 kV class. We will be applying soon. We are expecting the approval within this half year.”)

o There are no public listed companies who are operating in 400 and 765 kV class.

o Already executed orders of value-added products: We have already actually executed a 400 kV class order. So about, ₹4 crores to ₹5 crores of sale has already happened in the 400 kV class range. And with those precedents, and examples that were already set, we will go up to PGCIL and get it approved. So that should take about three to four months if everything goes well.

The company has about ₹18 crores of orders for 400 kV class.

• STRONG GROWTH GUIDANCE:

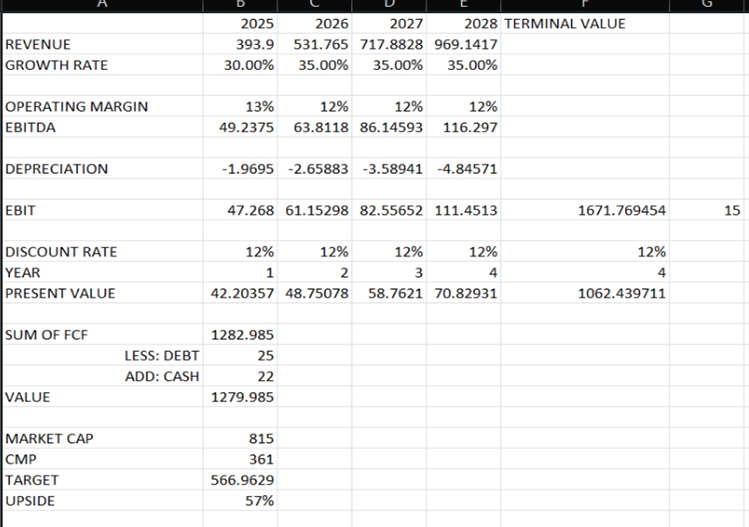

Targeting 30% Volume CAGR for the next 3 years. Looking to achieve 400cr revenues for FY25 and 600cr revenues for FY26 ( (FY24 sales – 303cr)

We are hoping to end the year with the capacity utilisation between 70% to 80% On over 18,000 MT capacity. So, three years down the line, we intend to go to full capacity utilisation in all three units, and probably next plan of expansion will probably start once the Unit III is underway.

We are expecting full capacity utilisation in the first half of the next financial year. It could be early also. It could be, but for sure, within the first half of the next financial year. (Of current 18000 MTPA capacity)

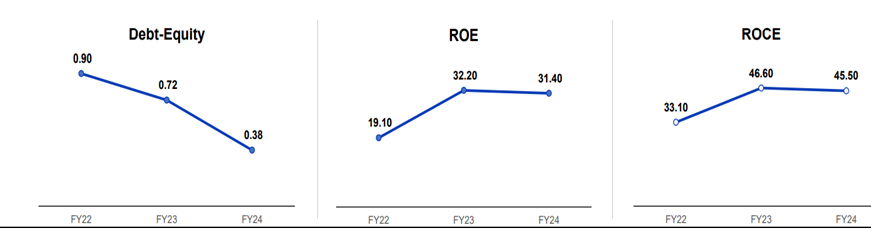

• STABLE FINANCIALS WITH GREAT RETURN RATIOS:

Net debt free as of H1FY25

RISKS

• COMPETITION:

CRGO steel industry is about 3 lakh tons in India on an annual basis. And like in FY ’24, we did about 9,400 tons. So that becomes about 3%, 3.5% of the market share. There are a few players, who are in the range of 25,000 to 30,000 tons, and then there are players in the range of 15,000 to 20,000 tons, then we are at a level of between 10,000 to 12,000 tons.

Vilas Transcore (listed company) Kryfs Power, Amod Stampings, and Vardhman Stampings are amongst the competitors.

(“In 400 kV and 765 kV class, I assume there would be about five to seven players. But it also depends on who has raw material and who is consistently working with these customers. So, I would say about five players. In lower range of 220 and below, in the organized space, again, there could be about including the five that I’ve talked about in 400 and 765. Additionally, there would be about five, seven players. so, these players would be contributing about, I mean, it’s a fairly vague assumption, but I think it would be about 40%, 45

But this market also has an unorganised segment. So, the total number of players on paper would be about more than 100.” )

There aren’t any unorganised players in power transformers.

Competitors are increasing capacity (Vilas Transcore also increasing capacity by 3x), but I think there will be a healthy market for everybody if the entire pie increases.

Lack of competition from overseas: One is that BIS is applicable on the product. So, there is a lethargy amongst the core manufacturers outside India to get BIS approvals. Second, and the bigger reason is that the lead times are very short. So, for example, our order book is generally one to three months. So, within that, lead times and each customer’s order is tailor made. So, we need to stock up inventory first, and then the order comes. So based on that, the lead time is so short that a player from outside India will not be able to serve the market.

(“Two years down the line, in terms of how the industry competitive dynamics may change as far as the demand supply gap is concerned because there are other players also who are increasing their capacity by 2x, 3x. So, two years down the line how do you see the demand supply playing out in terms of either I mean, will there be a mismatch or will there be a glut? What is your sense on that?

Management: I don’t really have a straightforward answer to your question. It all depends on the market dynamics. But looking at the demand side, I don’t see that, there will be much of supply demand mismatch. Or in fact, it could be that supply is still limited, but demand is coming strong.”)

• SLIGHTLY HIGH VALUATIONS (LACK OF MARGIN OF SAFTEY):

Currently trading at 18x FY25 EV/EBIT. Which is much cheaper than many of the transformer players. But still is above the comfort zone of 15x ev/ebit.

(Above estimates are conservative. Management is targeting 600cr by FY26 and 900cr by FY27)

MISCELLEANEOUS

• EBITDA MARGINS DYNAMICS:

Company has fixed EBITDA per ton margin structure regardless of FG-RAW MATERIAL price changes.

(“Our revenue has been close to ₹153 crores, which is almost at the same level as the previous half years. As I said, this was mainly because of the prices coming off, but the volumes have increased. Our EBITDA margin has increased because on a per kg basis, our EBITDA margins do not vary with the raw material or the sale prices. Hence, the margins on a percentage basis are increased to an extent of 52% YoY and 39% at half-yearly basis. Our PAT margins have increased by 49% on both YoY and HoH basis.

If you see that considering that the prices would not have dropped, volumes increased by 20%. And if you consider a 20% increase in the turnover, say, currently our turnover would have been ₹180 crores. So, on that basis, the margins would be around 7.8%. So, we are projecting margins around that level.

We will be somewhere in between 10% and 15%. 15% was achieved because of the low turnover base. Like I said, the turnover was low, but the volumes have increased. So, I mean, if you consider the PAT margin, it was actually 7.8%. If you consider, a similar price range increase of the last year. So considering ₹180 crores, ₹185 crores of turnover, if we consider a 20% jump in from compared to the last half year. The PAT margins are actually not 9.4%. It is lower. And similarly, EBITDA will also be we are hoping to target between 12% to 13%.)

Vulnerability of profitability to volatility in raw material prices and foreign exchange rates: The operating margins of the company remain susceptible to the volatility in price of the raw material. The raw material is generally imported and takes 2-3 months to deliver, and the company maintains moderate inventory and hence any fluctuation in raw material prices may impact the operating margins. Further, since a part of the raw material requirement is met through imports, the company is exposed to the adverse fluctuations in the foreign currency exchange rates.

Going forward, JBLL is expected to sustain PBILDT margins in the range of 10-11% on a growing revenue base in view of growing demand in the industry. – Credit Report

• CRGO STEEL SOURCING: We have tie ups with the most of the CRGO steel producing mills. There are about 10 to 15 CRGO mills in the world who are commercially and largely producing CRGO steel. We have the tie ups with most of the mills, and we directly purchase from the mills as well as we purchase through their stocking centres or through traders within India.

CRGO steel is mostly an imported product. But our imports are less. We almost have a ratio of about 80:20. 80% is domestic, and 20% is import.

With respect to CRGO steel, there has been certain restrictions by the government on the Chinese suppliers. However, like I said earlier, we have sufficient ties with the other CRGO steel producers to ensure that our requirements are fulfilled.

The problem is not that the CRGO is in short supply. It happens because there are multiple grades in CRGO steel. The customer generally has a very shorter forecast of, which grades will be required and with what quantities. And that that becomes a problem for us also sometimes. So, we basically purchase CRGO steel different grades on the basis of our projection, basis of our customer feedback. And because of that, our inventory level has also gone up. So, we are basically covered with a good level of inventory with respect to targeting the new customer base.

• EXPORTS: • Expand sales to International Markets including US and Europe • Increasing sales network overseas including Africa and Asia

Our exports in the last half year were about 11%, and previously, I think it was about 13% to 14%. We will continue to keep this level constant, because export is mostly distribution transformer cores. So, the volumes will be lesser than the power transformer cores that we are targeting in the near future. So even if we are able to keep up the same ratio with the increasing volumes, we will be happy.

• Lab Equipment Installation • Install the lab equipment received from Germany by H2FY25 • Get NABL Accreditation which will lead to reduce dependency on third party testing thereby reducing supply lead time

• Large working capital requirement: JBLL has working capital intensive operations largely on account of moderate debtors and inventory period required for business operations, while the company receives minimal credit from its suppliers and most of the procurement is done on letter of credit basis which led to increase in working capital requirement by the company. The Gross Current Asset though decreased, however still stood high at the level 151 days as on March 31, 2023 against 230 days as on March 31,2022.

Inventories increased from 44cr in Mar 24 to 90cr in Sept 24 (Sign of increased demand along with increased capacity)

• Product focus: We will focus on CRGO steel and amorphous core, because we are experts at core manufacturing. So that will be our first focus. As long as we are able to get growth in the core manufacturing part of transformers, we will not diversify. Once, that market gets saturated in the future for us, then we will think about diversification.

• Debt levels: We intend to keep the debt level at the same, because when we came out with the IPO, our main objective was to fund the working capital requirement that will come with the higher volumes. So, considering that last year, we did about ₹300 crores turnover with the debt that we had. We want to keep it at pretty much the same level with increasing turnover.

• Raw material fluctuations: The raw material prices fell in the last nine or 10 months that had an effect majorly in the last half year. Raw material prices fell primarily, because I mean the reason of raw material prices fluctuation is the global supply and demand of CRGO steel. It also depends on what is the demand structure in the U.S. and European markets. So, because CRGO steel is highly dependent on the power projects that come across from the utilities all over the world. So, if a certain power project comes up in a big way, the demand suddenly increases. And if power projects are not there, then the demand can decrease. So based on that, the fluctuation can be there.

• If I look at the gross profit per ton or EBITDA per ton, they have also increased by 15% to 20% in the first half compared to last year.

There were two reasons. One was, obviously, there was a certain inventory gain, and the second reason, which was more prevalent was the mix that we changed. When I say mix, it is not between segments or product mix. It is mainly about what kind of orders that we take from the customers. So, we sort of had the options to choose specific orders which were suited to our facilities, suited to our capacity because there can be orders in the industry, because the sizes, the dimensions, and the mix of orders can be so varied in our industry. But, if say a certain machine that has a capacity of 100 tons per month, it can go down to 50 tons per month, if we don’t use the right kind of orders on that machine. So capacity utilisation is the key and the orders that had the best margins was the key.

• Detailed concall and presentations right after first ever result declarations.

• Second generation already in management.

• Ashish Khacholia was present in concall

DISCLOSURE: INVESTED (3.5% of portfolio as a starting position. Conviction levels are high)

Midcap Momentum Portfolio (26-11-2024)

@gautamashukla I have two other threads on Microcap Momentum and Smallcap Momentum running in this forum. If you read the initial messages you will get an idea on how the pf is created.

We always start with an equi-weighted portfolio. We allow the winners to run and the ones exiting to leave as soon as possible. The exit rules are clearly defined and it is purely based on ranking.

As regards your specific question of investment, I suggest you consult a Financial advisor who might be able to guide you better.